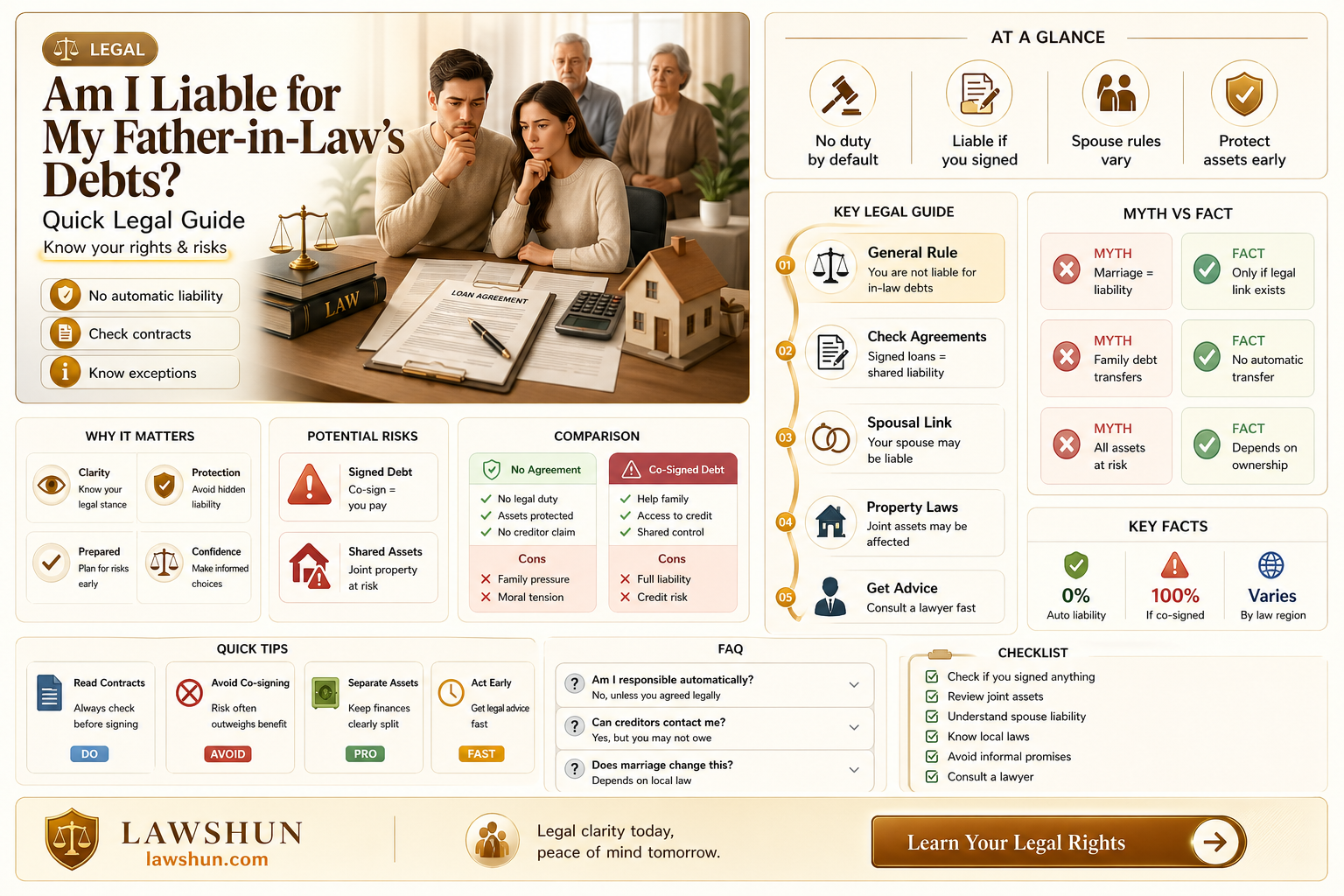

Navigating the complexities of familial financial responsibilities can be particularly challenging when it comes to in-laws, especially if questions arise about whether you are liable for your father-in-law’s debts. Generally, individuals are not legally responsible for the debts of their in-laws unless they have explicitly co-signed a loan, guaranteed the debt, or otherwise legally obligated themselves. However, nuances exist depending on jurisdiction, marital property laws, and specific circumstances, such as joint assets or commingled finances. It’s crucial to understand your legal standing, review any shared financial agreements, and seek professional advice to clarify your obligations and protect your own financial well-being.

| Characteristics | Values |

|---|---|

| Legal Responsibility | Generally, you are not responsible for your father-in-law's debts unless you co-signed or guaranteed the debt. |

| Community Property States | In some community property states (e.g., California, Texas), spouses may be liable for debts incurred during marriage, but this typically does not extend to in-laws. |

| Co-Signing or Guaranteeing Debt | If you co-signed or guaranteed your father-in-law's debt, you are legally responsible for it. |

| Joint Accounts or Assets | If you jointly own accounts or assets with your father-in-law, those assets may be at risk to satisfy his debts. |

| Estate Inheritance | If you inherit assets from your father-in-law, creditors may claim those assets to pay off his debts, but you are not personally liable beyond the inherited assets. |

| Medical Debts | In some states, family members may be responsible for medical debts of certain relatives, but this varies widely and typically does not apply to in-laws. |

| Debt Collection Practices | Debt collectors may attempt to pressure you into paying, but you are not legally obligated unless you have a direct legal tie to the debt. |

| Spousal Liability | Your spouse may be responsible for debts incurred during marriage in community property states, but this does not extend to your responsibility for your father-in-law's debts. |

| Bankruptcy Impact | If your father-in-law files for bankruptcy, his debts are typically discharged, and you are not responsible unless you co-signed or guaranteed the debt. |

| State-Specific Laws | Laws regarding debt responsibility vary by state, so consult local laws or an attorney for specific guidance. |

Explore related products

What You'll Learn

- Legal Obligations: Understanding if you're legally bound to your father-in-law's debts

- Marital Assets: How your spouse's assets might be affected by inherited debts

- Estate Laws: Role of inheritance laws in debt responsibility after death

- Joint Accounts: Liability if you share accounts with your father-in-law

- Cosigning Risks: Consequences of cosigning loans or debts with him

![]()

Legal Obligations: Understanding if you're legally bound to your father-in-law's debts

In most jurisdictions, you are not legally responsible for your father-in-law's debts solely because of your marital relationship. The law generally does not impose financial obligations on in-laws unless specific conditions are met. However, exceptions exist, and understanding these nuances is crucial to protecting your financial well-being. For instance, if you co-signed a loan or jointly own property with your father-in-law, you could be held liable for those debts. Similarly, in community property states like California, debts incurred during marriage may be shared between spouses, but this typically does not extend to in-laws unless they are explicitly involved in the financial agreement.

Consider the role of legal agreements in determining liability. If your father-in-law’s debt is tied to a business or estate in which you are a partner or beneficiary, you might be indirectly affected. For example, if he owns a family business and you are a co-owner, creditors could pursue the business’s assets, potentially impacting your financial stake. Additionally, if your father-in-law passes away and his estate is insolvent, any inheritance you receive could be subject to claims by creditors, though this does not make you personally liable for the debt itself. Always review legal documents carefully to ensure you are not inadvertently assuming responsibility.

A common misconception is that marriage automatically transfers debt liability to in-laws. This is false. Your legal obligations are primarily determined by your direct involvement in financial agreements, not familial ties. However, cultural or emotional pressures might lead to voluntary financial support, which is distinct from legal responsibility. For instance, some families may choose to help settle a relative’s debts out of goodwill, but this is a personal decision, not a legal mandate. To avoid confusion, maintain clear boundaries between your finances and those of your in-laws, and consult a legal professional if you’re unsure about potential liabilities.

Practical steps can further safeguard your financial independence. First, keep your assets separate from those of your in-laws unless you explicitly agree to share responsibility. Second, monitor joint accounts or properties to ensure no unauthorized debts are incurred. Third, if your father-in-law requests financial assistance, consider drafting a formal agreement to clarify terms and protect both parties. Finally, stay informed about local laws, as they can vary significantly. For example, in some countries, family members may be held responsible for certain debts under specific circumstances, such as unpaid medical bills or taxes. Proactive measures and legal awareness are key to avoiding unintended financial entanglements.

Mastering Argumentative Law Essays: Essential Tips for Legal Writing Success

You may want to see also

Explore related products

![]()

Marital Assets: How your spouse's assets might be affected by inherited debts

In community property states, inherited debts can unexpectedly entangle marital assets, even if the debt predates the marriage. For instance, if your spouse inherits a debt from their father—say, unpaid medical bills or credit card balances—and the inheritance is commingled with joint assets, creditors may have a claim on those shared resources. This occurs because community property laws treat income and assets acquired during the marriage as jointly owned, regardless of whose name is on the title. To shield your assets, keep inherited funds in a separate account and avoid using them for joint expenses like mortgage payments or vacations.

Consider the scenario where your spouse inherits a house with an outstanding mortgage from their father. If the estate lacks sufficient funds to cover the debt, the lender may pursue your spouse for repayment. If the house is sold and the proceeds are deposited into a joint account, creditors could argue that the money has become marital property, exposing your shared assets to collection efforts. A proactive step here is to consult an estate attorney to structure the inheritance in a way that isolates the debt, such as placing the asset in a trust or disclaiming the inheritance altogether.

In contrast, equitable distribution states offer more protection for marital assets from inherited debts. These states view assets and debts acquired during the marriage as belonging to the individual who incurred them, unless they’re used for the benefit of both spouses. For example, if your spouse inherits a debt but keeps it separate from joint finances, creditors typically cannot touch your assets. However, if the inherited debt is used to pay for a family expense—like a home renovation—it could blur the lines of ownership, making your assets vulnerable. Always document the source and use of inherited funds to maintain clarity.

Practical tip: If your spouse is expecting an inheritance that includes debt, establish a prenuptial or postnuptial agreement explicitly stating that inherited debts remain separate from marital assets. This legal safeguard can prevent creditors from pursuing shared resources. Additionally, monitor credit reports regularly to ensure no unauthorized accounts or debts are tied to your name or joint accounts. By taking these steps, you can minimize the risk of inherited debts disrupting your financial stability.

Understanding the Law of Conservation of Energy: Significance and Applications

You may want to see also

Explore related products

![]()

Estate Laws: Role of inheritance laws in debt responsibility after death

Inheritance laws play a pivotal role in determining debt responsibility after a loved one’s death, but their application varies widely by jurisdiction. In most cases, heirs are not personally liable for a deceased relative’s debts unless they co-signed a loan or explicitly agreed to assume responsibility. However, creditors can claim repayment from the deceased’s estate before assets are distributed to beneficiaries. This means that if your father-in-law’s estate has insufficient assets to cover his debts, the remaining balance is typically written off—you are not obligated to pay out of pocket. Understanding this distinction is crucial, as it prevents heirs from mistakenly believing they must liquidate personal assets to settle a deceased relative’s financial obligations.

The probate process is the legal mechanism through which a deceased person’s debts are settled, and it operates under strict estate laws. During probate, an executor or administrator inventories the estate’s assets, notifies creditors, and pays valid claims using estate funds. If your father-in-law’s debts exceed his estate’s value, creditors cannot pursue you or other heirs for payment unless you have a legal obligation tied to the debt. For instance, if you jointly owned a credit card or property with your father-in-law, you may be liable for a portion of the debt. Always review joint accounts and legal agreements to assess potential exposure.

A common misconception is that inheriting assets automatically transfers debt responsibility. In reality, inheritance laws protect heirs from inheriting debt unless they take specific actions. For example, if you accept an inheritance and the estate is still in debt, creditors can claim the inherited assets to satisfy the obligation. To avoid this, some jurisdictions allow heirs to disclaim an inheritance, effectively refusing it and preventing creditors from accessing those assets. This strategy can be particularly useful if the estate’s liabilities outweigh its assets, but it must be executed promptly and in accordance with local laws.

Practical steps can further safeguard heirs from unintended debt responsibility. First, consult an estate attorney to review the will, probate process, and potential liabilities. Second, ensure all joint accounts and co-signed loans are identified and addressed early. Third, monitor the probate process to confirm creditors are paid from the estate, not personal funds. Finally, if you’re considering accepting an inheritance, weigh the asset’s value against the estate’s debts to make an informed decision. By leveraging estate laws and taking proactive measures, heirs can navigate debt responsibility after a loved one’s death with clarity and confidence.

E-Cigarettes and the Law: Understanding Regulations and Legal Boundaries

You may want to see also

Explore related products

![]()

Joint Accounts: Liability if you share accounts with your father-in-law

Sharing a joint account with your father-in-law can blur the lines of financial responsibility, often leading to confusion about who is liable for debts incurred. When you open a joint account, both parties typically have equal access and ownership, meaning any debt accumulated on the account becomes a shared obligation. This arrangement is governed by the principle of joint and several liability, where creditors can pursue either party for the full amount owed. For instance, if your father-in-law uses the account to rack up credit card debt or overdraft fees, you could be held responsible for repaying it, even if you didn’t personally benefit from the expenditures.

Consider the practical implications of this setup. Joint accounts are often used for convenience, such as managing household expenses or pooling resources for shared goals. However, without clear boundaries or agreements, one party’s financial missteps can quickly become your problem. For example, if your father-in-law faces a sudden medical emergency and maxes out the joint credit card, the debt collectors won’t differentiate between the two of you—they’ll pursue both parties equally. To mitigate this risk, it’s crucial to establish ground rules, such as setting spending limits or requiring mutual consent for large transactions.

From a legal standpoint, closing a joint account isn’t always a straightforward solution. If the account already carries debt, closing it won’t erase the liability. Both parties remain responsible for the outstanding balance until it’s fully repaid. Additionally, removing one person’s name from the account typically requires the consent of all account holders and may not retroactively absolve them of prior debts. If you’re considering a joint account with your father-in-law, consult a financial advisor or attorney to understand the long-term implications and explore alternatives, such as separate accounts with designated contributions for shared expenses.

A comparative analysis reveals that joint accounts differ significantly from other financial arrangements, like authorized user status on a credit card. As an authorized user, you can make purchases but aren’t legally obligated to repay the debt unless you’ve signed an agreement stating otherwise. In contrast, joint account holders are equally liable by default. This distinction highlights the importance of choosing the right financial tool for your situation. If your goal is to help your father-in-law manage expenses without assuming full liability, adding him as an authorized user on your account might be a safer option.

Ultimately, sharing a joint account with your father-in-law requires careful consideration and proactive measures to protect your financial well-being. Start by having an open conversation about expectations, risks, and responsibilities. Draft a written agreement outlining how the account will be used and who is responsible for what. Regularly monitor the account activity to catch any discrepancies early. While joint accounts can foster financial cooperation, they demand transparency, trust, and a clear understanding of the legal obligations involved. Without these safeguards, you risk becoming entangled in debts that weren’t yours to begin with.

Ohio Nurse CEU Requirements: Understanding Your Law Credit Needs

You may want to see also

Explore related products

![]()

Cosigning Risks: Consequences of cosigning loans or debts with him

Cosigning a loan or debt with your father-in-law may seem like a gesture of goodwill, but it’s a decision that carries significant financial and legal weight. When you cosign, you’re not just vouching for his ability to repay; you’re legally obligating yourself to cover the debt if he defaults. This means your credit score, assets, and financial stability are on the line. Before agreeing, consider whether you’re prepared to assume full responsibility for the debt, as lenders will hold you accountable regardless of your relationship dynamics.

Analyzing the risks reveals a stark reality: cosigning can jeopardize your financial future. If your father-in-law misses payments, the lender will report the delinquency to your credit report, potentially lowering your score. This can affect your ability to secure loans, rent an apartment, or even land a job, as many employers check credit histories. Additionally, if the debt goes into collections, you could face lawsuits or wage garnishments. The emotional strain of such consequences can also strain family relationships, turning a well-intentioned act into a source of conflict.

A comparative look at alternatives highlights safer options. Instead of cosigning, explore whether your father-in-law can qualify for a secured loan, which uses collateral to reduce risk for the lender. Alternatively, suggest he rebuild his credit through smaller, manageable debts or a credit-builder loan. If financial assistance is necessary, consider gifting a lump sum without tying it to a loan agreement. While this may feel less formal, it protects your finances and avoids the legal pitfalls of cosigning.

Practically speaking, if you’re already cosigned on a debt, take proactive steps to mitigate risk. Monitor the account regularly to ensure payments are made on time. If your father-in-law faces financial hardship, encourage him to contact the lender immediately to discuss options like deferment or a modified payment plan. In extreme cases, you may need to pay the debt yourself to protect your credit, then seek reimbursement through family agreements or legal channels. Remember, once you cosign, reversing the decision is nearly impossible without the debt being fully repaid or refinanced.

The takeaway is clear: cosigning is not a casual favor but a binding commitment. Before agreeing, weigh the potential impact on your finances, credit, and family relationships. If you proceed, do so with a full understanding of the risks and a plan to minimize them. Ultimately, protecting your financial health is paramount, even when faced with the pressure of familial expectations.

Arizona's Abandoned Property Laws: Understanding Your Rights and Responsibilities

You may want to see also

Frequently asked questions

Generally, you are not personally responsible for your father-in-law's debts unless you co-signed for them or live in a community property state where spousal assets may be liable. His estate is typically responsible for settling debts.

No, creditors cannot pursue your personal assets for your father-in-law's debts unless you are a co-signer or guarantor. However, they may seek repayment from his estate or assets.

If your spouse inherits assets, the estate must first settle debts before distributing inheritances. Your spouse is not personally liable unless they co-signed or live in a community property state.

Your father-in-law's bankruptcy does not affect you unless you are financially tied to his debts (e.g., co-signed). Your credit and assets remain separate.