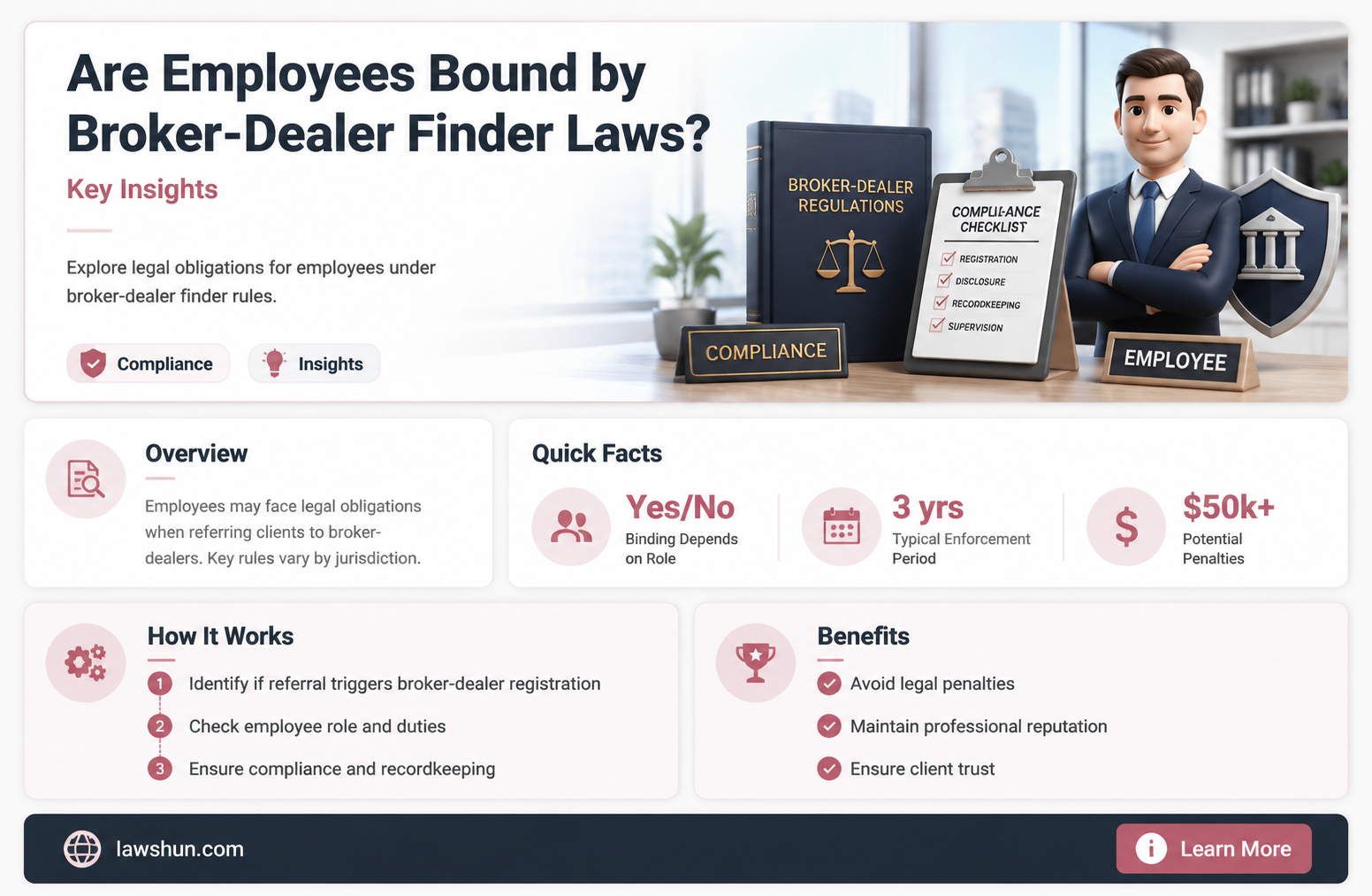

The question of whether employees are subject to broker-dealer finder laws is a critical one, particularly in industries where financial transactions and intermediary roles are common. Broker-dealer finder laws, which regulate individuals or entities that facilitate securities transactions or connect buyers and sellers, often come with strict registration and compliance requirements. Employees who engage in activities that could be construed as finding or soliciting investments may inadvertently fall under these regulations, even if they are not formally designated as brokers or dealers. This raises important considerations for both employers and employees, as non-compliance can result in significant legal and financial penalties. Understanding the scope of these laws and how they apply to various roles within an organization is essential to ensure adherence to regulatory standards and mitigate potential risks.

| Characteristics | Values |

|---|---|

| Applicability | Employees may be subject to broker-dealer finder laws if they act as intermediaries in securities transactions, even if not formally registered as brokers. |

| Registration Requirement | Generally, individuals acting as brokers or finders must register with the SEC and FINRA unless exempt. |

| Exemptions | Employees may be exempt if their activities are limited to intra-company transactions, or if they meet specific criteria under Rule 3a4-1 (e.g., not receiving transaction-based compensation). |

| Compensation Structure | Transaction-based compensation (e.g., commissions) often triggers broker-dealer registration requirements. |

| Scope of Activities | Activities like soliciting investors, negotiating terms, or facilitating securities transactions may subject employees to these laws. |

| Regulatory Bodies | SEC (Securities and Exchange Commission) and FINRA (Financial Industry Regulatory Authority) enforce broker-dealer regulations. |

| Penalties for Non-Compliance | Failure to register can result in fines, legal action, and reputational damage. |

| State Laws | Some states have additional broker-dealer registration requirements that employees must comply with. |

| Recent Updates | As of the latest data, there are no significant changes to federal laws, but enforcement actions have increased in recent years. |

| Best Practices | Companies should ensure employees understand their roles and comply with securities laws, including seeking legal advice when necessary. |

Explore related products

What You'll Learn

![]()

Definition of Broker-Dealer Activities

Broker-dealer activities are strictly regulated under U.S. securities laws, primarily by the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). These activities encompass the buying, selling, and facilitating of securities transactions on behalf of clients or for a firm’s own account. Key functions include acting as a middleman between buyers and sellers, providing investment advice, and underwriting securities offerings. Understanding the scope of these activities is critical, as engaging in them without proper registration can result in severe legal and financial penalties. For employees, the question arises: does their role inadvertently cross into broker-dealer territory, subjecting them to these regulations?

Consider the case of an employee who regularly refers clients to a specific investment firm in exchange for a fee. While this may seem like a finder’s fee arrangement, it could be construed as engaging in broker-dealer activities if the employee is involved in soliciting securities transactions or negotiating terms. The SEC defines a broker as "any person engaged in the business of effecting transactions in securities for the account of others." Even if the employee does not execute trades directly, activities such as recommending specific securities or structuring deals may trigger regulatory scrutiny. Practical tip: employees should review FINRA Rule 2020, which prohibits gifts or gratuities that influence recommendations, to ensure their actions remain compliant.

Analyzing the distinction between finder and broker-dealer roles is essential. A finder typically introduces parties to a transaction but does not participate in the negotiation or execution of the deal. In contrast, a broker-dealer actively facilitates the transaction, often providing advice or handling the mechanics of the trade. For instance, an employee who merely connects a startup with potential investors may not be subject to broker-dealer laws, but if they discuss investment merits or assist in structuring the deal, they may cross the line. Caution: courts and regulators often focus on the substance of the activities rather than the title of the role, so employees must carefully assess their involvement.

To mitigate risks, employees should adopt a proactive approach. First, document all activities related to securities transactions, ensuring clarity on the scope of involvement. Second, consult legal counsel or compliance officers to determine if registration as a broker-dealer is necessary. Third, establish clear boundaries in finder agreements, explicitly stating that the employee will not provide investment advice or negotiate terms. For example, a well-drafted agreement might include language such as, "The finder shall not engage in any activities that constitute the offer or sale of securities or provide investment recommendations." This reduces ambiguity and aligns with regulatory expectations.

In conclusion, the definition of broker-dealer activities is broad and hinges on the nature of the employee’s involvement in securities transactions. While finder roles may seem distinct, the line between the two can blur easily, particularly when employees receive compensation for referrals. By understanding the regulatory framework, adopting cautious practices, and seeking guidance when necessary, employees can navigate this complex landscape without inadvertently violating securities laws. The takeaway is clear: compliance is not just about avoiding penalties—it’s about protecting both the employee and the organization from unnecessary legal exposure.

Understanding Dower Interest Accrual in Ohio: Key Legal Insights

You may want to see also

Explore related products

![]()

Employee Roles and Exemptions

Employees of broker-dealers often find themselves navigating a complex web of regulations, particularly when their roles intersect with finder activities. A critical question arises: Are these employees subject to the same stringent broker-dealer finder laws that govern their employers? The answer hinges on the nature of their duties and the exemptions carved out by regulatory frameworks such as those established by the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). Understanding these distinctions is essential for compliance and risk mitigation.

Consider the role of an employee who identifies potential investment opportunities but does not engage in the actual negotiation or execution of transactions. Such individuals may fall under the "associated person" category, which typically requires registration as a broker-dealer representative. However, certain exemptions exist. For instance, the "issuer exemption" allows employees of a company to engage in finder activities related to their employer’s securities without registering as broker-dealers, provided their efforts are limited to their employer’s offerings. This exemption is particularly relevant for in-house corporate development teams or investor relations staff.

Contrast this with employees who facilitate transactions between third parties, even if indirectly. These individuals may inadvertently trigger broker-dealer registration requirements if their activities involve soliciting buyers or sellers, negotiating terms, or receiving transaction-based compensation. A practical example is a business development manager who connects investors with external investment opportunities in exchange for a fee. In such cases, the lack of an exemption could expose both the employee and their employer to regulatory scrutiny, fines, or legal action.

To navigate these complexities, employees and their employers must adopt a proactive approach. First, clearly define job roles and responsibilities to ensure they align with regulatory exemptions. Second, implement internal compliance programs that include regular training on broker-dealer laws and finder activity restrictions. Third, consult legal counsel when structuring compensation arrangements or expanding into new business areas that may involve finder activities. By doing so, organizations can minimize the risk of non-compliance while leveraging their employees’ expertise effectively.

Ultimately, the interplay between employee roles and regulatory exemptions underscores the need for precision in both job design and compliance strategies. While exemptions provide flexibility, they are not blanket protections. Employees and employers must remain vigilant, ensuring that their activities fall squarely within the boundaries of applicable laws. This nuanced understanding not only safeguards against regulatory penalties but also fosters a culture of ethical and informed business practices.

Is the Patriot Act a Statutory Law? Understanding Its Legal Framework

You may want to see also

Explore related products

![]()

Finder’s Fee Legal Boundaries

Employees often navigate a complex web of regulations when engaging in activities that resemble brokerage services, particularly when finders fees are involved. The legal boundaries surrounding these fees are critical to understand, as they differentiate between permissible compensation and potential violations of securities laws. For instance, the Securities and Exchange Commission (SEC) requires individuals who facilitate securities transactions to register as broker-dealers unless they meet specific exemptions. Employees who receive finders fees for introducing investors or deals must ensure their activities do not cross into unregistered brokerage territory, as this can result in severe penalties, including fines and legal action.

One key distinction lies in the nature of the employee’s role and the extent of their involvement. If an employee merely provides a referral without negotiating terms, structuring deals, or handling funds, they may fall under the "finder" exception. However, this exception is narrow and varies by jurisdiction. For example, in some states, finders must still register if their activities involve public offerings or frequent transactions. Practical tip: Employees should document their actions meticulously, ensuring they do not engage in activities like soliciting investments or advising on securities, which are strictly regulated under broker-dealer laws.

A comparative analysis reveals that international regulations further complicate this landscape. In the European Union, for instance, the Markets in Financial Instruments Directive (MiFID II) imposes stricter requirements on individuals receiving finders fees, often mandating registration even for limited activities. Conversely, some U.S. courts have interpreted the "isolated transaction" exemption more broadly, allowing certain finders to operate without registration. This disparity underscores the importance of consulting local laws and, if necessary, seeking legal counsel to navigate these boundaries effectively.

Persuasively, companies must proactively educate their employees about these legal boundaries to mitigate risk. Implementing clear policies that define permissible referral activities and providing training on securities laws can prevent unintentional violations. For example, a financial services firm might establish a compliance checklist for employees, outlining when and how finders fees can be accepted. Cautionary note: Ignorance of the law is not a defense, and even well-intentioned employees can face consequences if their actions inadvertently violate broker-dealer regulations.

In conclusion, the legal boundaries of finders fees are nuanced and require careful consideration, especially for employees operating in industries adjacent to securities transactions. By understanding the distinctions between permissible referrals and regulated brokerage activities, documenting actions meticulously, and staying informed about jurisdictional differences, individuals and organizations can navigate this complex terrain while minimizing legal exposure.

Is the Patriot Act a Primary Law? Exploring Its Legal Status

You may want to see also

Explore related products

![]()

Regulatory Compliance Requirements

Employees engaged in activities that resemble brokerage or finder services must navigate a complex web of regulatory compliance requirements, even if they are not formally registered as broker-dealers. The Securities Exchange Act of 1934 and regulations from the Securities and Exchange Commission (SEC) impose stringent obligations on individuals who facilitate securities transactions or receive transaction-based compensation. For instance, an employee who introduces investors to investment opportunities in exchange for a fee may inadvertently trigger broker-dealer registration requirements under Section 15(a) of the Act. Failure to comply can result in severe penalties, including fines, disgorgement of profits, and reputational damage.

To avoid regulatory pitfalls, employees must first assess whether their activities meet the definition of a "broker" under SEC guidelines. Key factors include the frequency of transaction involvement, the nature of compensation, and the extent of investment advice provided. For example, a one-time referral for a friend may not qualify, but systematic introductions for commissions likely do. The SEC’s 2019 guidance on digital asset securities further complicates this analysis, as it extends broker-dealer obligations to activities involving blockchain-based transactions. Employees in fintech or emerging markets must exercise particular caution.

Practical compliance strategies include implementing internal policies that clearly delineate permissible activities and establishing firewalls between employees involved in sales or marketing and those providing investment advice. Firms should also conduct regular training sessions to educate staff on the nuances of broker-dealer regulations, emphasizing real-world scenarios. For instance, a case study of the 2018 SEC enforcement action against an unregistered finder firm could illustrate the consequences of non-compliance. Additionally, leveraging legal counsel to review compensation structures and client agreements can provide a critical layer of protection.

A comparative analysis of state and federal regulations reveals inconsistencies that employees must address. While the SEC governs securities transactions at the federal level, states like California and New York impose their own licensing requirements for broker-dealer activities. Employees operating across jurisdictions must ensure compliance with the most restrictive applicable laws. For example, California’s Corporate Securities Law of 1968 mandates registration for anyone engaged in the sale of securities, even if their role is limited to finding investors. This layered regulatory environment demands meticulous attention to detail.

Ultimately, the takeaway is clear: employees cannot assume they are exempt from broker-dealer regulations simply because they are not formally titled as such. Proactive measures, such as self-audits, legal consultations, and ongoing education, are essential to mitigate risks. By treating compliance as a dynamic, rather than static, obligation, individuals and firms can navigate the regulatory landscape with confidence and avoid the pitfalls that have ensnared others.

Understanding CWS: Its Role and Significance in Legal Proceedings

You may want to see also

Explore related products

![]()

Penalties for Non-Compliance

Non-compliance with broker-dealer finder laws can trigger severe penalties, often escalating beyond financial fines to include reputational damage and operational disruptions. Regulatory bodies like the SEC and FINRA impose sanctions based on the severity and frequency of violations. For instance, unregistered broker-dealer activity can result in civil penalties up to $100,000 per violation for individuals and $500,000 for firms, alongside disgorgement of ill-gotten gains. These penalties are not static; they adjust for inflation and the scale of the misconduct, making them a formidable deterrent.

Beyond monetary fines, non-compliance can lead to criminal charges, particularly if fraud or intentional deception is involved. Employees found guilty of willful violations may face imprisonment, with sentences varying from six months to 20 years, depending on the jurisdiction and nature of the offense. For example, under the Securities Exchange Act, criminal penalties for fraudulent activities can include up to 25 years in prison and millions in fines. Such outcomes underscore the critical need for employees to understand their obligations under these laws.

Reputational harm is another significant penalty, often more damaging than financial sanctions. Firms and individuals implicated in non-compliance may face exclusion from industry networks, loss of client trust, and difficulty attracting future business. Regulatory actions are publicly disclosed, creating a lasting record that can hinder career advancement. For employees, this can mean blacklisting from future roles in the financial sector, effectively ending their careers.

Practical steps to mitigate these risks include implementing robust compliance programs, conducting regular training, and maintaining detailed records of all transactions. Firms should also establish clear policies defining employee roles and responsibilities, ensuring no one inadvertently crosses regulatory boundaries. For example, employees should be explicitly informed whether their duties involve soliciting investments or merely supporting registered brokers. Such clarity can prevent unintentional violations and demonstrate good faith to regulators.

Finally, proactive engagement with legal counsel and compliance experts is essential. These professionals can provide tailored advice, conduct audits, and represent firms in the event of investigations. While the cost of compliance may seem high, it pales in comparison to the penalties for non-compliance. Firms that prioritize adherence to broker-dealer finder laws not only avoid sanctions but also build a reputation for integrity, a priceless asset in the financial industry.

Mastering Citations: A Guide to Citing UCLA Law Review Articles

You may want to see also

Frequently asked questions

Employees are not automatically subject to broker-dealer finder laws solely based on their employment status. However, if they engage in activities that meet the definition of a broker-dealer (e.g., soliciting securities transactions for compensation), they may be subject to registration and compliance requirements under federal or state securities laws.

Employees may act as finders in limited circumstances without registering as broker-dealers, but this depends on the specific activities performed and the jurisdiction. Generally, if the employee receives transaction-based compensation and actively solicits or facilitates securities transactions, registration may be required.

Penalties for violating broker-dealer finder laws can include fines, disgorgement of profits, injunctions, and even criminal charges in severe cases. Additionally, individuals may face reputational damage and restrictions on future involvement in the securities industry.

Employees should consult legal counsel to assess whether their activities require broker-dealer registration. They should also establish clear policies, maintain detailed records, and avoid transaction-based compensation if they are not registered. Staying informed about applicable state and federal securities laws is also crucial.