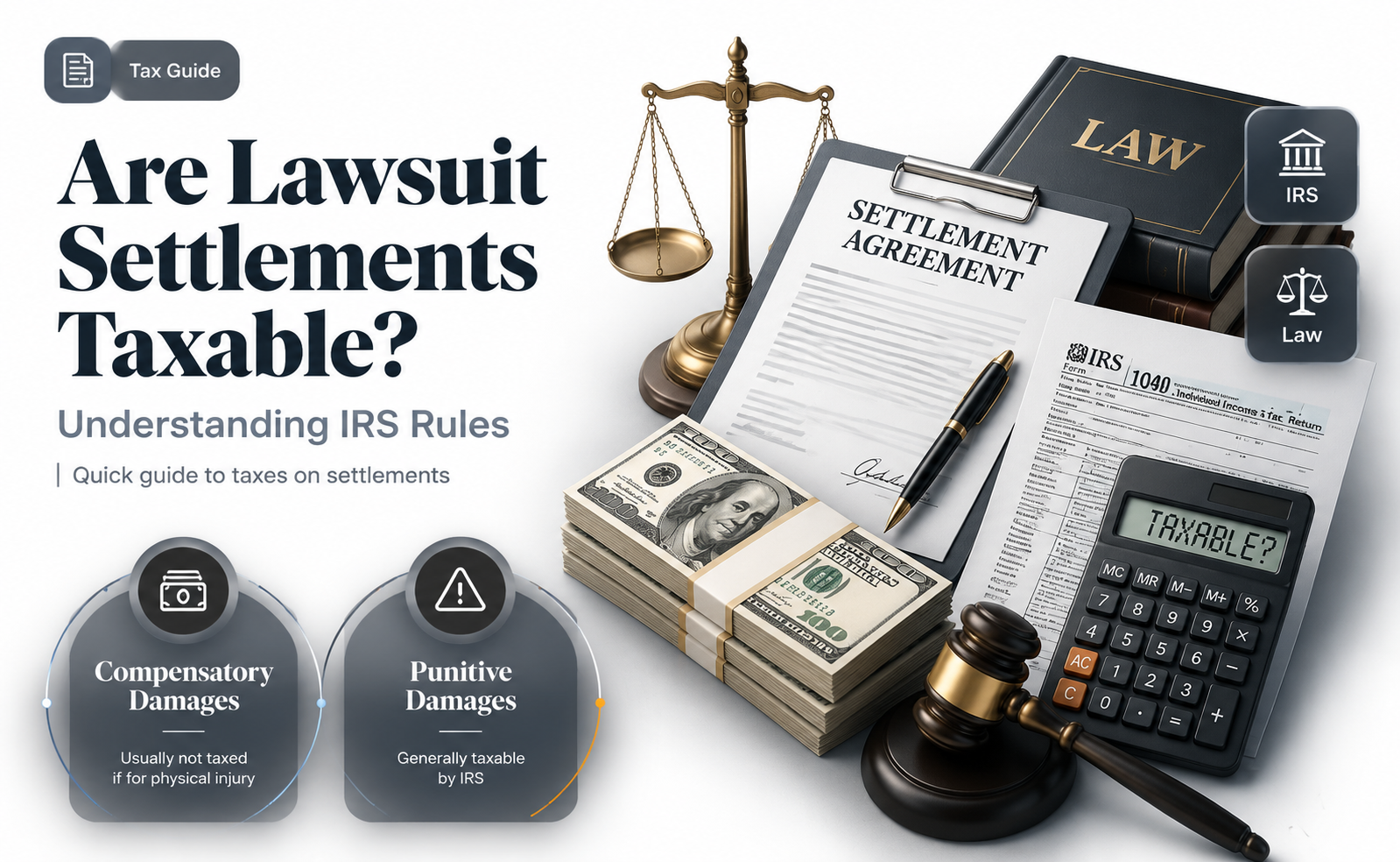

When considering whether lawsuit settlements are taxable, it’s essential to understand that the tax treatment depends on the nature of the settlement. Generally, the IRS treats settlement proceeds as taxable income unless they are specifically excluded by law. For instance, compensation for physical injuries or physical sickness is typically tax-free, while punitive damages, lost wages, and interest on the settlement are usually taxable. Additionally, attorney fees and legal costs may also impact the taxable amount. It’s crucial to consult tax professionals or refer to IRS guidelines to accurately determine the tax implications of a specific settlement, as misreporting can lead to penalties or audits.

Explore related products

What You'll Learn

![]()

Taxability of Physical Injury Settlements

Physical injury settlements often come with a critical yet overlooked question: Are they taxable? The Internal Revenue Service (IRS) provides clear guidance on this matter, rooted in the distinction between compensatory and punitive damages. Generally, settlements for physical injuries or physical sickness are tax-free under Section 104(a)(2) of the Internal Revenue Code. This exemption applies to amounts received to cover medical expenses, lost wages, and pain and suffering directly tied to the physical injury. However, if a portion of the settlement compensates for non-physical injuries, such as emotional distress not stemming from a physical ailment, that portion may be taxable. Understanding this distinction is crucial for accurate tax reporting and financial planning.

Consider a hypothetical scenario: A plaintiff receives a $150,000 settlement after a car accident. Of this, $100,000 covers medical bills and lost wages, while $50,000 is allocated for emotional distress. The $100,000 tied to physical injuries is tax-free, but the $50,000 for emotional distress may be taxable unless it can be directly linked to the physical injury. This example highlights the importance of clear allocation in settlement agreements. Plaintiffs and their attorneys should ensure that settlement documents explicitly separate taxable and non-taxable components to avoid unexpected tax liabilities.

The IRS also scrutinizes settlements involving punitive damages, which are awarded to punish the defendant rather than compensate the plaintiff. Unlike compensatory damages for physical injuries, punitive damages are fully taxable, regardless of the underlying claim. For instance, if a plaintiff receives a $200,000 settlement, with $150,000 for physical injuries and $50,000 in punitive damages, the latter amount must be reported as taxable income. This rule underscores the need for plaintiffs to carefully review their settlement agreements and consult with tax professionals to ensure compliance.

Practical tips can help individuals navigate the tax implications of physical injury settlements. First, maintain detailed records of all medical expenses and lost wages to substantiate the tax-free portion of the settlement. Second, negotiate settlement agreements that clearly delineate between physical injury compensation and other damages. Third, consult a tax advisor to assess the settlement’s taxability and explore strategies for minimizing taxable income, such as structuring payments over multiple years. By taking these steps, plaintiffs can maximize their financial recovery while adhering to tax laws.

In conclusion, while physical injury settlements are generally tax-free, the devil is in the details. Proper allocation of settlement amounts, awareness of IRS rules, and proactive tax planning are essential to avoid pitfalls. By understanding the nuances of taxability, individuals can ensure their settlements provide the intended financial relief without unwelcome tax surprises.

Mastering Hooke's Law: A Step-by-Step Guide to Calculating Force

You may want to see also

Explore related products

![]()

Punitive Damages Taxation Rules

Punitive damages, designed to punish and deter egregious behavior, are a unique component of lawsuit settlements. Unlike compensatory damages, which aim to restore the plaintiff to their pre-injury state, punitive damages serve a broader societal purpose. However, their tax treatment is far from straightforward. The IRS classifies punitive damages as taxable income under Section 104(a)(2) of the Internal Revenue Code, which excludes only damages received on account of personal physical injuries or physical sickness. This means that if your settlement includes punitive damages, you’ll likely owe taxes on that portion, regardless of the underlying claim.

Consider a scenario where a plaintiff wins a $1 million settlement, with $700,000 in compensatory damages for physical injuries and $300,000 in punitive damages. While the compensatory damages may be tax-free, the punitive damages are fully taxable as ordinary income. This distinction can significantly impact the plaintiff’s net recovery, especially in high-stakes cases. For instance, in a 24% federal tax bracket, the plaintiff would owe $72,000 in taxes on the punitive damages alone. State taxes may further reduce the final amount, underscoring the importance of tax planning in these situations.

One critical exception to this rule involves wrongful death claims. Under Section 104(c), damages received in a wrongful death action are not taxable, even if they include punitive damages. This exception is narrowly applied and depends on state law governing wrongful death statutes. For example, if a state allows punitive damages in wrongful death cases and explicitly excludes them from taxation, the IRS will follow suit. However, this exception is rare, and most punitive damages remain taxable.

To navigate these rules effectively, plaintiffs should consult a tax professional early in the settlement process. Strategies such as allocating settlement amounts to non-taxable categories (e.g., medical expenses or lost wages) can minimize tax liability. Additionally, structuring settlements over multiple years may reduce the tax burden by keeping the plaintiff in a lower tax bracket. For instance, receiving $100,000 annually over three years instead of a lump sum of $300,000 could result in lower overall taxes, depending on the taxpayer’s income level.

In conclusion, punitive damages taxation rules are complex and require careful consideration. While they are generally taxable, exceptions and planning strategies exist to mitigate their financial impact. Understanding these rules is essential for plaintiffs to maximize their net recovery and avoid unexpected tax liabilities. By working with legal and tax professionals, individuals can navigate this challenging landscape with greater confidence and clarity.

Filing a Lawsuit: Step-by-Step Guide to Navigating the Legal Process

You may want to see also

Explore related products

![]()

Emotional Distress Payouts & Taxes

Emotional distress payouts from lawsuits often leave recipients wondering about their tax implications. The IRS generally treats these settlements as taxable income unless they meet specific criteria. For instance, if the payout compensates for physical injuries or physical sickness, it’s typically tax-free under Section 104(a)(2) of the Internal Revenue Code. However, emotional distress awards not tied to physical harm are usually taxable as ordinary income. This distinction is crucial, as it directly impacts the amount you’ll owe come tax season.

Consider a scenario where a plaintiff wins a lawsuit for workplace harassment, receiving $50,000 for emotional distress. If the harassment didn’t result in a physical injury or sickness, the entire amount is taxable. Conversely, if the emotional distress stemmed from a physical assault, the payout could be tax-exempt. The key lies in the origin of the claim: physical harm or not. Courts and the IRS scrutinize the nature of the damages, so precise documentation linking emotional distress to physical injury is essential for tax-free treatment.

Navigating these rules requires careful strategy. If you’re pursuing a lawsuit, consult a tax professional early to structure the settlement agreement effectively. For example, allocating funds specifically to physical injuries or medical expenses can shield portions of the payout from taxation. Additionally, keep detailed records of medical treatments or diagnoses related to the emotional distress, as these can strengthen your case for tax exemption. Ignoring these steps could result in unexpected tax liabilities, reducing the net value of your settlement.

One practical tip is to negotiate separate line items in the settlement agreement. For instance, if your case involves both emotional distress and physical injury, ensure the agreement clearly distinguishes between the two. This transparency helps the IRS understand the allocation and reduces the risk of audits. Remember, while emotional distress payouts can provide financial relief, failing to account for their tax treatment can turn a windfall into a financial burden. Always prioritize clarity and compliance to maximize your settlement’s after-tax value.

Understanding the Role of a County's Top Law Officer

You may want to see also

Explore related products

![]()

Lost Wages Settlements Tax Treatment

Lost wages settlements often arise from employment disputes, personal injury claims, or wrongful termination cases. The IRS treats these settlements as income if they compensate for lost earnings, making them taxable at ordinary income rates. This means if you receive a settlement for wages you would have earned had the disruption not occurred, you’ll likely owe taxes on that amount. For example, if you settle for $50,000 in lost wages, the entire sum is taxable unless specific exceptions apply. Understanding this rule is critical, as failing to report such income can lead to penalties and audits.

One key exception to taxation involves settlements tied to physical injuries or sickness. Under Section 104(a)(2) of the Internal Revenue Code, compensation for physical injuries or physical sickness is generally tax-free. However, lost wages fall into a gray area. If the lost wages are directly linked to a physical injury or sickness—such as a workplace accident—they may be exempt. For instance, if a construction worker receives a settlement for lost wages due to a back injury sustained on the job, that portion could be non-taxable. But if the lost wages stem from emotional distress or reputational harm, they remain taxable.

To navigate this complexity, careful documentation is essential. When negotiating a settlement, structure the agreement to clearly separate taxable and non-taxable components. For example, allocate specific amounts to physical injuries and lost wages, respectively. If the settlement is lump-sum, consult a tax professional to determine the taxable portion. Additionally, if you deducted medical expenses related to the injury on your taxes, the settlement may need to be reported as income to offset those deductions. This interplay between deductions and settlements underscores the need for meticulous record-keeping.

Practical tips can help minimize tax liabilities. First, consider spreading the settlement over multiple tax years if possible, as this may reduce your tax bracket in any given year. Second, use pretax dollars from a health savings account (HSA) or flexible spending account (FSA) to cover medical expenses, freeing up more of the settlement for non-taxable purposes. Finally, if you’re self-employed, ensure you account for self-employment taxes on the taxable portion of the settlement. Proactive planning and professional advice are invaluable in optimizing the tax treatment of lost wages settlements.

Stickers on Recycling Bins: Legal or Littering? Understanding Local Laws

You may want to see also

Explore related products

![]()

Attorney Fees Impact on Taxability

Attorney fees can significantly alter the taxability of lawsuit settlements, often in ways that surprise both plaintiffs and their legal counsel. Under the Internal Revenue Code (IRC) Section 104(a)(2), certain settlement amounts are tax-exempt if they compensate for personal physical injuries or sickness. However, when attorney fees are deducted from these settlements, the IRS may treat the entire settlement as taxable unless specific conditions are met. For instance, if a $100,000 settlement for physical injuries includes $30,000 in attorney fees paid directly by the plaintiff, the IRS could argue that only $70,000 is tax-exempt, leaving the remaining $30,000 subject to taxation.

To mitigate this risk, plaintiffs and attorneys should structure settlements to allocate fees explicitly. The IRS allows tax-exempt treatment for attorney fees if the settlement agreement clearly designates the portion attributable to physical injuries and ensures fees are paid from non-exempt funds. For example, in a case involving both physical injuries and emotional distress, the agreement should specify that attorney fees are deducted from the taxable portion (emotional distress) rather than the tax-exempt portion (physical injuries). This requires precise drafting and foresight during negotiations.

A cautionary tale emerges from cases like *O’Brien v. Commissioner*, where the Tax Court ruled that attorney fees reduced the tax-exempt portion of a settlement because the agreement lacked clear allocation. Plaintiffs must proactively address this issue, as the IRS scrutinizes ambiguous agreements. If fees are paid directly by the defendant without allocation, the entire settlement may be taxed, regardless of the underlying claim. This underscores the importance of involving tax professionals early in the settlement process.

Practically, plaintiffs should request itemized settlement agreements that separate taxable and non-taxable components. For example, if a settlement includes $80,000 for physical injuries and $20,000 for punitive damages, attorney fees should be deducted from the $20,000 taxable portion. Additionally, plaintiffs can consider contingency fee arrangements where attorneys are paid a percentage of the recovery, ensuring fees are tied to the tax-exempt portion. This approach aligns with IRS guidelines and minimizes tax liability.

In conclusion, attorney fees are a critical factor in determining the taxability of lawsuit settlements. By understanding IRS rules and structuring agreements carefully, plaintiffs can preserve the tax-exempt status of their compensation. Ignoring this detail can lead to unexpected tax bills, making it essential to treat attorney fees as a strategic component of settlement negotiations rather than an afterthought.

Are Law Classes Liberal Arts at Baruch College?

You may want to see also

Frequently asked questions

Not all lawsuit settlements are taxable. Generally, settlements for personal physical injuries or physical sickness are tax-free, while those for lost wages, punitive damages, or non-physical injuries may be taxable.

Check the nature of the settlement. If it compensates for physical injuries or medical expenses, it’s likely tax-free. If it covers lost wages, emotional distress, or punitive damages, it may be taxable. Consult IRS guidelines or a tax professional for clarity.

No, nontaxable settlements (e.g., for physical injuries) do not need to be reported on your tax return. However, if any portion of the settlement is taxable, it must be reported as income.