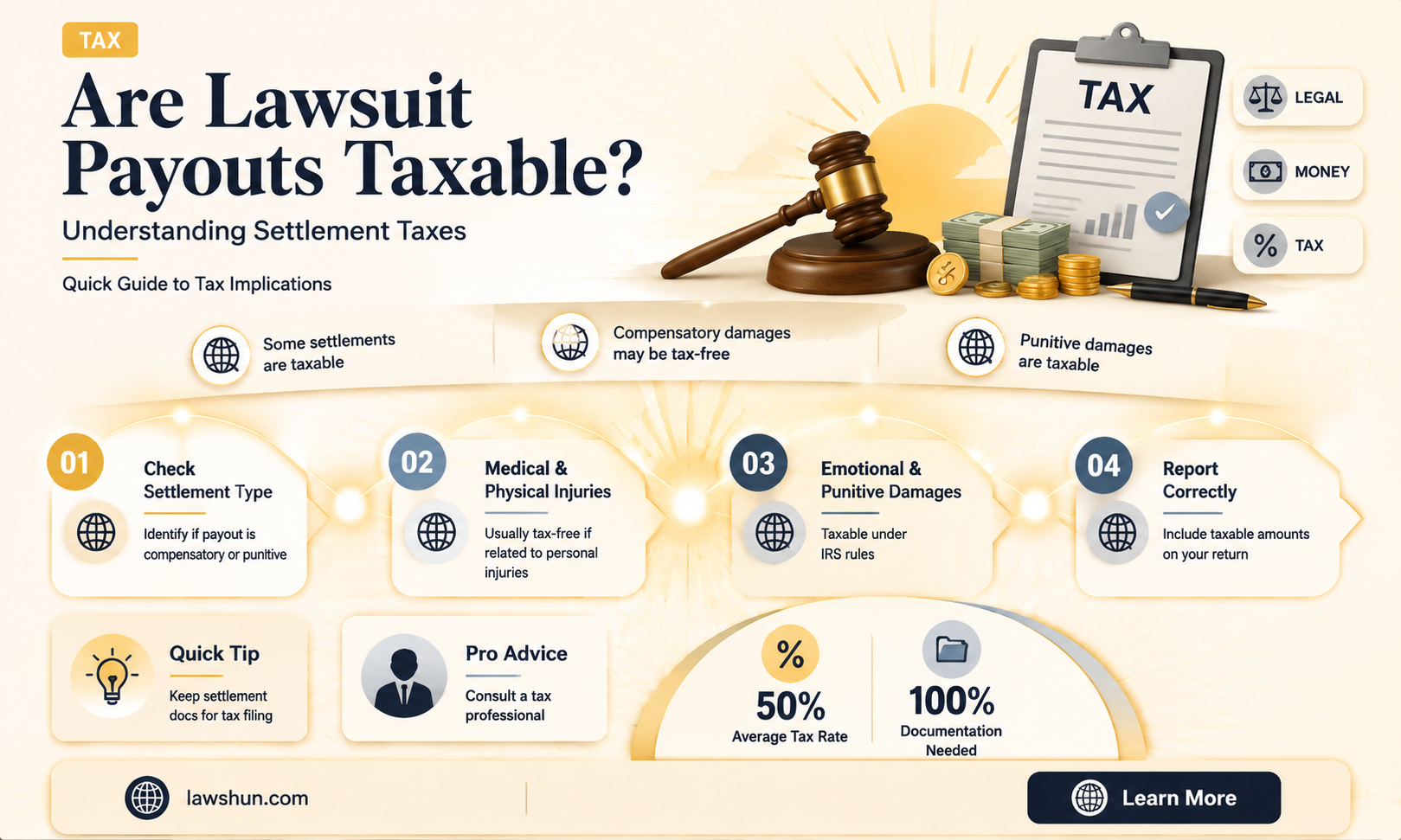

When individuals receive payouts from a lawsuit, a common question arises: are these proceeds taxable? The answer depends on the nature of the settlement or award. Generally, compensation for physical injuries or physical sickness is not taxable under U.S. federal law, as outlined in IRS guidelines. However, if the payout includes punitive damages, lost wages, or interest, these portions may be subject to taxation. Additionally, settlements related to non-physical injuries, such as emotional distress or defamation, are often taxable unless directly tied to medical expenses. It’s crucial to consult tax professionals or review IRS Publication 4345 for specific guidance, as proper reporting and understanding of taxable components can prevent unexpected tax liabilities.

| Characteristics | Values |

|---|---|

| General Rule | Most lawsuit payouts are taxable unless specifically excluded by law. |

| Taxable Payouts | - Lost wages or earnings - Punitive damages - Interest on judgments |

| Non-Taxable Payouts | - Personal physical injury or sickness - Emotional distress tied to physical injury - Wrongful death claims (in some cases) |

| IRS Guidelines | Follows the "origin of the claim" rule to determine taxability. |

| Reporting Requirements | Taxable amounts must be reported on Form 1040 or other applicable forms. |

| State Tax Treatment | Varies by state; some states follow federal rules, others have exceptions. |

| Attorney Fees | If fees are deducted from the award, only the net amount is taxable. |

| Structured Settlements | Tax treatment depends on the nature of the claim (taxable or non-taxable). |

| Exceptions | Discrimination claims under specific laws (e.g., Title VII) may be taxable. |

| Documentation Needed | Settlement agreements and court documents to determine taxability. |

| Recent Updates (as of latest data) | No significant changes in federal tax laws regarding lawsuit payouts. |

Explore related products

What You'll Learn

![]()

Taxability of Compensatory Damages

Compensatory damages, designed to restore a plaintiff to their pre-injury financial state, often raise questions about tax implications. The Internal Revenue Service (IRS) generally treats these payouts as tax-free if they compensate for physical injuries or physical sickness. This rule stems from the principle that such damages replace lost income or cover medical expenses, which are typically non-taxable. However, the taxability shifts when the damages compensate for non-physical injuries, such as emotional distress or reputational harm, unless the distress arises from a physical injury. For instance, a plaintiff awarded $50,000 for medical bills and $30,000 for pain and suffering would only need to report the latter if it wasn’t tied to a physical ailment.

Understanding the source of the damages is crucial for accurate tax reporting. Punitive damages, intended to punish the defendant rather than compensate the plaintiff, are always taxable, regardless of the underlying claim. In contrast, compensatory damages for lost wages or profits are taxable because they replace income that would have been subject to tax. For example, if a freelancer receives $20,000 for lost business income due to a breach of contract, that amount is taxable as ordinary income. Taxpayers must carefully review the breakdown of their settlement or judgment to determine which portions fall into taxable categories.

Practical tips can help navigate this complexity. First, request a detailed allocation of damages in the settlement agreement or court judgment to clarify taxable and non-taxable components. Second, consult a tax professional to ensure compliance with IRS rules, especially in cases involving mixed claims. Third, retain all medical records and documentation linking emotional distress to physical injuries, as this can exempt related damages from taxation. For instance, a plaintiff suing for workplace discrimination might need to prove physical symptoms like migraines or insomnia to exclude emotional distress damages from taxable income.

Comparatively, other countries treat compensatory damages differently. In the UK, most compensation for personal injuries is tax-free, while in Canada, damages for lost income are taxable but those for pain and suffering are not. U.S. taxpayers should be aware of these distinctions, especially in cross-border litigation. Additionally, state laws may influence how damages are categorized, though federal tax rules ultimately govern their treatment. For example, California’s approach to emotional distress claims might differ from Texas’, but the IRS’s taxability standards remain consistent nationwide.

In conclusion, the taxability of compensatory damages hinges on the nature of the injury and the type of loss being compensated. While damages for physical injuries are typically tax-free, those for non-physical injuries or lost income require careful scrutiny. Proactive steps, such as detailed documentation and professional advice, can prevent unexpected tax liabilities. By understanding these nuances, plaintiffs can better manage their financial recovery and avoid pitfalls in tax reporting.

The Jungle's Impact: 1906 Law Revolutionizing Consumer Protection

You may want to see also

Explore related products

![]()

Punitive Damages and Taxes

Punitive damages, designed to punish and deter egregious behavior, occupy a unique tax position. Unlike compensatory damages, which restore a plaintiff to their pre-harm state and are generally tax-free, punitive damages are considered taxable income by the IRS. This distinction stems from their punitive nature; they exceed mere compensation and are treated as a windfall, subject to federal and often state income tax. For instance, if a plaintiff receives $500,000 in a lawsuit, with $300,000 in compensatory damages and $200,000 in punitive damages, the latter amount would be taxable.

Understanding the tax implications of punitive damages requires careful planning. Plaintiffs should consult a tax professional to strategize how to report and pay taxes on these awards. One practical tip is to set aside a portion of the punitive damages to cover the anticipated tax liability, ensuring compliance and avoiding penalties. Additionally, plaintiffs should be aware of the timing of tax payments; punitive damages are taxed in the year they are received, not when the lawsuit was filed. This can significantly impact tax brackets and overall financial planning.

A comparative analysis reveals that while punitive damages are taxable, certain exceptions exist. For example, punitive damages awarded under federal law for wrongful death or personal physical injuries are exempt from taxation under Section 104(a)(2) of the Internal Revenue Code. However, this exemption does not apply to state law claims, creating a complex landscape for plaintiffs and their attorneys. This disparity underscores the importance of understanding the jurisdictional basis of the lawsuit and its tax consequences.

From a persuasive standpoint, the taxation of punitive damages raises questions about fairness. Critics argue that taxing punitive damages reduces their deterrent effect, as defendants may factor in the plaintiff’s tax liability when assessing potential risks. Proponents, however, contend that treating punitive damages as taxable income aligns with the principle that all income, regardless of its source, should be subject to taxation. This debate highlights the need for legislative clarity to balance deterrence with equitable tax treatment.

In conclusion, punitive damages are a taxable component of lawsuit payouts, requiring careful attention to tax laws and financial planning. Plaintiffs must navigate the nuances of federal and state regulations, consult professionals, and consider exceptions that may apply. By understanding these specifics, individuals can mitigate tax liabilities and ensure compliance, turning a potentially burdensome situation into a manageable financial outcome.

Annual U.S. Legislation: How Many Laws Are Voted In Yearly?

You may want to see also

Explore related products

![]()

Medical Expense Settlements

To ensure compliance, recipients must meticulously document their medical expenses. Keep receipts, invoices, and statements from healthcare providers to substantiate the tax-free portion of the settlement. If you deducted these expenses in prior tax years, the settlement may need to be reported as income to offset the earlier deduction. For example, if you claimed $10,000 in medical deductions last year and receive a $50,000 settlement for those same expenses, $10,000 becomes taxable to avoid double-dipping. Consult IRS Publication 525 for detailed guidance on this adjustment.

A critical distinction arises when settlements involve punitive damages, which are always taxable, regardless of the case’s nature. Suppose a medical malpractice suit awards $200,000, with $150,000 for medical expenses and $50,000 in punitive damages. The latter amount must be reported as income. This rule underscores the importance of understanding the breakdown of your settlement. Work with your attorney to clearly allocate amounts in the settlement agreement, separating taxable and non-taxable components to avoid surprises at tax time.

Practical tip: If you’re expecting a medical expense settlement, consult a tax professional early in the process. They can advise on structuring the settlement to minimize tax liability and ensure proper documentation. For instance, if you’re over 65 or have a chronic condition, certain deductions or credits may apply, further reducing your taxable burden. Proactive planning can save you from unexpected tax bills and streamline the post-settlement financial process.

In summary, medical expense settlements are generally tax-free, but the devil is in the details. Proper documentation, understanding settlement allocations, and professional guidance are key to navigating this complex area. By staying informed and organized, you can focus on recovery without the added stress of tax complications.

Stridhan: Understanding Women's Property Rights in India

You may want to see also

Explore related products

![]()

Lost Wages Taxation Rules

Lost wages awarded in a lawsuit often represent compensation for income you would have earned had the wrongful act not occurred. The IRS treats these payments as taxable income, aligning them with the category of wages or salary. This means if you receive a settlement or court award for lost wages, you must report it on your tax return, typically on Line 1 of Form 1040 as “Wages, salaries, tips.” The reasoning is straightforward: the IRS views lost wages as a replacement for income that would have been taxed had it been earned normally. For example, if you sue your employer for wrongful termination and receive $50,000 for lost wages, that $50,000 is taxable just as your regular paycheck would be.

However, the taxation of lost wages can become more complex when combined with other types of damages in a settlement. For instance, if your lawsuit includes compensation for emotional distress or punitive damages, those amounts may be taxed differently. Emotional distress damages are generally taxable unless they stem from a physical injury or sickness. Punitive damages, on the other hand, are always taxable, regardless of the underlying claim. To avoid overpaying or underpaying taxes, it’s crucial to carefully allocate the settlement amount between lost wages and other damages. This often requires detailed documentation and, in some cases, the assistance of a tax professional or attorney.

One practical tip for handling lost wages in a lawsuit is to ensure proper withholding. Unlike regular paychecks, settlement payments often do not have taxes automatically withheld. If you anticipate a large payout for lost wages, consider requesting that the payer withhold taxes or set aside a portion of the funds to cover your tax liability. Failing to account for taxes upfront can lead to a significant bill at tax time, along with potential penalties and interest. For example, if you receive a $100,000 settlement for lost wages, you might owe $24,000 or more in federal taxes, depending on your tax bracket.

It’s also worth noting that lost wages awarded in workers’ compensation cases are generally not taxable at the federal level. This exception applies because workers’ compensation benefits are considered a form of insurance rather than income replacement. However, if you also receive Social Security Disability Insurance (SSDI) benefits, part of your workers’ compensation payment may be taxable. State tax rules can vary, so it’s essential to check local regulations. For instance, some states, like Pennsylvania, do not tax workers’ compensation benefits, while others may treat them differently.

In summary, lost wages from a lawsuit are taxable as ordinary income, but careful planning and allocation of settlement funds can help you navigate this rule effectively. Always consult with a tax professional or attorney to ensure compliance with both federal and state tax laws. By understanding these rules and taking proactive steps, you can minimize surprises and manage your tax obligations efficiently.

Slavery in Mosaic Civil Law: Historical Context and Legal Analysis

You may want to see also

![]()

Attorney Fees Impact on Taxes

Attorney fees can significantly alter the tax implications of a lawsuit settlement or award. When these fees are deducted directly from the payout, they reduce the taxable portion of the amount received. For instance, if you receive a $100,000 settlement and your attorney takes $40,000 as a contingency fee, only $60,000 is considered taxable income. This reduction is crucial because it directly lowers your tax liability, potentially saving you thousands of dollars. However, this benefit only applies if the attorney fees are paid out of the settlement or award itself, not if they are paid separately by the client.

The tax treatment of attorney fees also depends on the nature of the lawsuit. In personal injury cases, for example, compensation for physical injuries or physical sickness is generally tax-free under IRS rules. If attorney fees are deducted from such an award, they do not affect the tax-exempt status of the remaining amount. Conversely, in cases involving employment disputes or breach of contract, where the payout is often fully taxable, the deduction of attorney fees becomes a critical factor in minimizing tax obligations. Understanding this distinction is essential for accurate tax planning.

One practical tip for taxpayers is to ensure clear documentation of how attorney fees are handled in the settlement agreement. The IRS requires that the allocation of fees be explicitly stated to determine the taxable portion of the payout. For example, if a settlement agreement specifies that $50,000 of a $150,000 award is for attorney fees, only $100,000 is reported as taxable income. Without such clarity, the IRS may treat the entire amount as taxable, leading to unexpected tax bills. Consulting a tax professional can help navigate these complexities and ensure compliance.

A comparative analysis reveals that the impact of attorney fees on taxes varies across jurisdictions. In some states, attorney fees may be treated differently under local tax laws, adding another layer of complexity. For instance, while federal tax rules allow for the reduction of taxable income by attorney fees in certain cases, state tax laws may not offer the same benefit. Taxpayers must therefore consider both federal and state regulations to fully understand their tax obligations. This dual-level scrutiny underscores the importance of tailored advice from professionals familiar with both federal and state tax codes.

In conclusion, attorney fees play a pivotal role in determining the tax consequences of lawsuit payouts. By reducing the taxable portion of a settlement or award, they can significantly lower tax liabilities, especially in cases where the payout is otherwise fully taxable. Clear documentation and an understanding of the specific legal and tax context are essential for maximizing this benefit. Whether through contingency fees or other arrangements, taxpayers should proactively address how attorney fees are structured to optimize their financial outcomes.

Mobile's Dog Roaming Laws: What Pet Owners Need to Know

You may want to see also

Frequently asked questions

Not all lawsuit payouts are taxable. Generally, compensation for physical injuries or physical sickness is tax-free, while punitive damages, interest, and compensation for non-physical injuries (e.g., emotional distress) may be taxable.

Yes, settlements from employment-related lawsuits, such as wrongful termination or discrimination, are typically taxable as ordinary income, unless they are specifically allocated to physical injuries or sickness.

Yes, you must report taxable portions of a lawsuit payout on your tax return. Consult the IRS guidelines or a tax professional to determine which parts are taxable and how to report them.

If your attorney fees are deducted from a taxable portion of the payout, that amount is still considered taxable income. However, if the fees are related to tax-free compensation (e.g., physical injury), they may not be taxable.