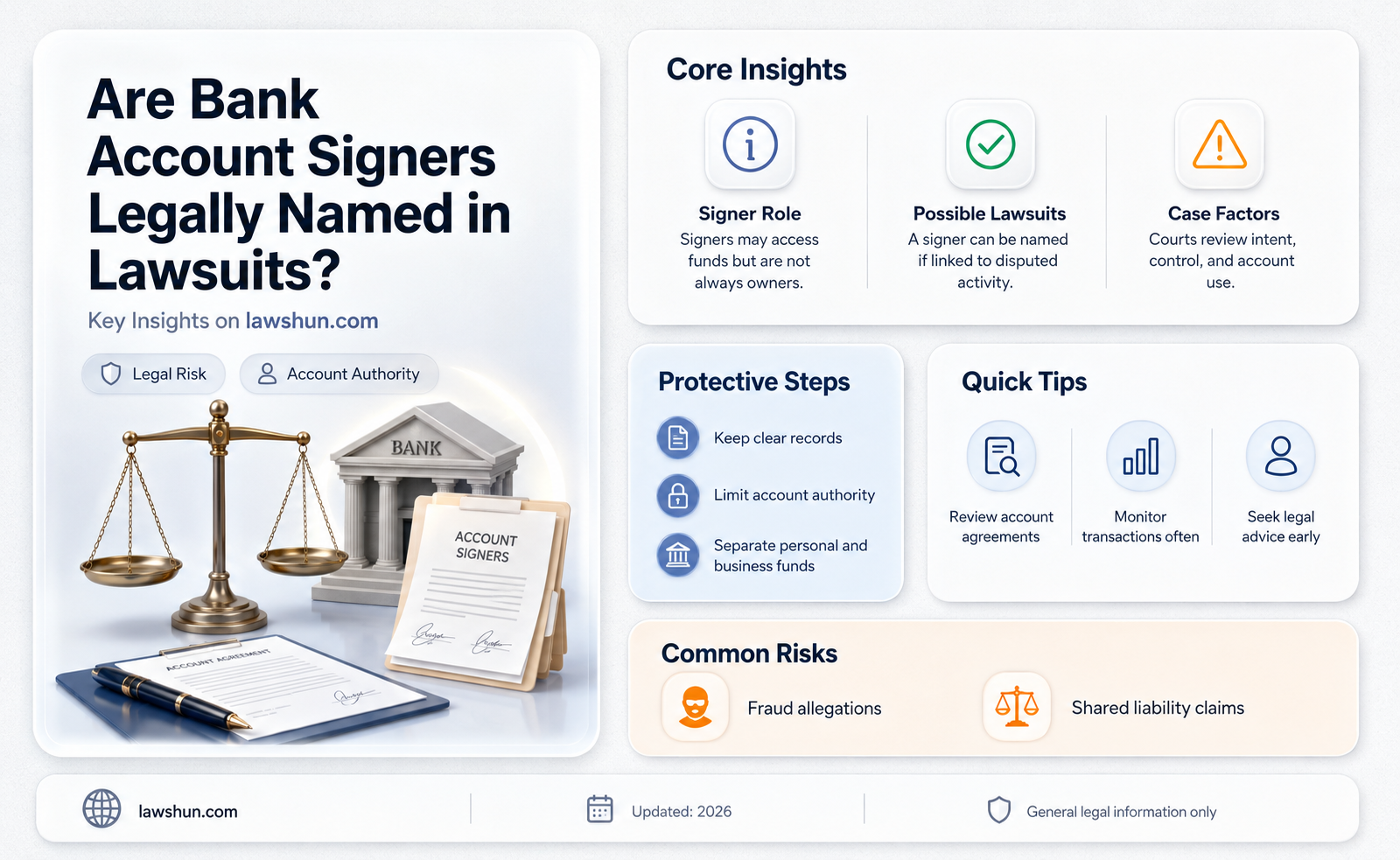

When individuals are named as signers on a bank account, they may face legal implications if the account becomes involved in a lawsuit. In many cases, if the account is jointly held or if the signer has authority over the funds, they could be named as a defendant in legal proceedings related to the account, such as disputes over ownership, fraud, or debt collection. Courts often consider the level of control and responsibility the signer has over the account when determining liability. Additionally, if the account is tied to a business or organization, signers may be held personally accountable in certain circumstances, depending on the jurisdiction and the specifics of the case. Understanding these risks is crucial for anyone who holds signing authority on a bank account, as it can impact their personal and financial liability.

| Characteristics | Values |

|---|---|

| Legal Liability | Signers of a bank account can be named in lawsuits if the account is involved in fraudulent activities, breaches of contract, or other legal disputes. |

| Joint Account Holders | All joint account holders are typically named in lawsuits related to the account, as they share equal responsibility. |

| Authorized Signers | Authorized signers may be named if their actions or decisions contributed to the legal issue. |

| Fraud or Misuse | If the account is used for fraud, embezzlement, or illegal activities, signers may be held personally liable. |

| Breach of Contract | Signers can be named if the account violates terms of service or loan agreements tied to the account. |

| Garnishment or Collection Actions | Signers may be named in lawsuits if creditors seek to garnish funds from the account for unpaid debts. |

| Estate or Probate Disputes | In cases of inheritance or probate, signers may be named if there are disputes over account ownership or distribution. |

| Tax Liability | Signers can be named if the account is involved in tax evasion or unpaid tax liabilities. |

| Business Accounts | For business accounts, signers (e.g., owners, officers) may be named in lawsuits related to business debts or liabilities. |

| Personal vs. Business Liability | Liability depends on whether the account is personal or business; business signers may face greater exposure. |

| State-Specific Laws | Liability varies by state; some states offer more protection for signers, while others hold them strictly accountable. |

| Account Type | Liability differs for checking, savings, or trust accounts based on their legal structure and purpose. |

| Indemnification Clauses | Some bank agreements may include clauses limiting signer liability, but these are not universal. |

| Legal Representation | Signers named in lawsuits are advised to seek legal counsel to defend their interests. |

Explore related products

What You'll Learn

- Account Holder Liability: Are primary account holders solely responsible, or can joint signers be sued

- Authorized Signer Risks: Do authorized signers face legal liability in bank-related lawsuits

- Corporate Account Signers: Are business account signers personally named in corporate lawsuits

- Fraud and Signers: Can signers be sued if fraudulent activity occurs on the account

- State vs. Federal Law: How do state and federal laws differ in naming signers in lawsuits

![]()

Account Holder Liability: Are primary account holders solely responsible, or can joint signers be sued?

In joint bank accounts, both primary and joint signers share legal responsibility for the account's activities, making them equally vulnerable to lawsuits. This shared liability stems from the contractual agreement with the bank, which typically binds all account holders to the terms and conditions. For instance, if a joint account is overdrawn or involved in fraudulent transactions, creditors or legal entities can pursue either signer for the full amount owed. This principle is rooted in the concept of joint and several liability, where each party is individually accountable for the entire debt.

Consider a scenario where a joint account is used for a small business. If the business defaults on a loan tied to the account, both the primary and joint signers can be named in a lawsuit. Courts often view joint account holders as partners in financial decisions, regardless of their individual contributions or intentions. This means a joint signer who may have had minimal involvement could still face legal consequences, including wage garnishment or asset seizure, if the primary account holder is unable to pay.

However, the extent of liability can vary based on state laws and the type of account. In some jurisdictions, joint tenants with rights of survivorship may face different legal treatments compared to tenants in common. For example, in a tenancy in common, liability might be proportionate to each signer’s ownership share, whereas joint tenants are typically held fully responsible. Understanding these distinctions is crucial for account holders to assess their potential exposure.

To mitigate risks, joint account holders should establish clear agreements outlining financial responsibilities and limits. For instance, a written contract between signers can specify that one party is responsible for certain transactions or debts. While such agreements may not always hold up in court, they provide a basis for negotiation or defense. Additionally, regularly monitoring account activity and setting up alerts can help detect unauthorized transactions early, reducing the likelihood of legal disputes.

Ultimately, joint signers are not merely passive participants in a bank account—they are co-owners with shared legal obligations. Whether through negligence, fraud, or contractual obligations, both primary and joint account holders can be sued individually or collectively. Proactive measures, such as maintaining transparency, setting boundaries, and seeking legal advice when necessary, are essential to navigating the complexities of joint account liability. Ignoring these risks can lead to financial and legal entanglements that affect both parties long-term.

Understanding Home-Related Laws: A Guide to Domestic Legal Applications

You may want to see also

Explore related products

![]()

Authorized Signer Risks: Do authorized signers face legal liability in bank-related lawsuits?

Authorized signers on bank accounts often assume their role is purely administrative, but this assumption can be dangerously misguided. While primary account holders typically bear the brunt of legal liability, authorized signers are not immune to legal risks. Courts and regulatory bodies increasingly scrutinize the actions of all individuals with signing authority, particularly in cases involving fraud, embezzlement, or unauthorized transactions. For instance, if an authorized signer approves a fraudulent wire transfer, they may be held personally liable if their negligence or complicity is proven. This reality underscores the need for signers to understand their legal exposure and take proactive measures to mitigate risks.

Consider the case of a small business where an authorized signer, tasked with managing payroll, inadvertently approves a series of fraudulent checks. If the bank sues to recover losses, the signer could be named as a defendant alongside the business owner. The court might examine whether the signer exercised reasonable care, such as verifying transaction details or implementing internal controls. In such scenarios, ignorance or reliance on others is rarely a valid defense. Authorized signers must recognize that their signature carries legal weight, and failing to act responsibly can lead to personal financial liability, damaged reputations, and even criminal charges in extreme cases.

To minimize legal exposure, authorized signers should adopt a structured approach to their responsibilities. First, ensure all transactions align with the account’s purpose and the signer’s authorized scope. Second, maintain detailed records of every approved transaction, including dates, amounts, and justifications. Third, establish clear internal protocols for transaction approval, such as requiring dual signatures for large amounts or periodic reviews by a third party. Fourth, stay informed about the account’s activity through regular bank statements and alerts. Finally, consider consulting legal counsel to understand the specific liabilities associated with the role and jurisdiction.

A comparative analysis reveals that authorized signers in corporate accounts often face greater scrutiny than those on personal accounts. Corporate signers are expected to adhere to higher fiduciary standards, particularly if they are officers or directors. For example, in a lawsuit alleging misuse of company funds, a corporate signer might be held to a stricter standard of care than a family member authorized on a joint personal account. This distinction highlights the importance of tailoring risk management strategies to the account type and the signer’s role within the organization or relationship.

Ultimately, being an authorized signer is not a ceremonial role but a position of trust with significant legal implications. While not every signer will face lawsuits, those who do can suffer severe consequences if unprepared. By understanding their responsibilities, implementing safeguards, and staying vigilant, authorized signers can protect themselves from unwarranted liability. The key takeaway is clear: signing authority is a privilege that demands accountability, and ignorance of the risks is no defense in the eyes of the law.

How Supreme Court Cases Shape and Define U.S. Laws

You may want to see also

Explore related products

![]()

Corporate Account Signers: Are business account signers personally named in corporate lawsuits?

Corporate account signers often find themselves in a precarious position when their company faces legal action. The question of personal liability arises: Can individuals who sign on corporate bank accounts be named in lawsuits? The answer hinges on the legal structure of the business and the actions of the signer. In most cases, corporations and limited liability companies (LLCs) shield individuals from personal liability, but exceptions exist. For instance, if a signer commingles personal and business funds or engages in fraudulent activities, they may be personally named in a lawsuit. Understanding these nuances is critical for anyone authorized to sign on a corporate account.

Consider a scenario where a small business owner, acting as the primary signer on the company’s bank account, fails to pay a vendor. If the business is structured as a sole proprietorship, the owner is personally liable for the debt, and their personal assets could be at risk. However, if the business is an LLC or corporation, the vendor would typically sue the company, not the individual signer. Yet, if the signer acted negligently or intentionally mismanaged funds, they could be named personally. For example, in *Clarke v. Capital One Bank* (2018), a signer was held personally liable for unauthorized transactions due to gross negligence. This underscores the importance of adhering to corporate formalities and maintaining clear separation between personal and business finances.

To mitigate personal risk, corporate account signers should follow specific steps. First, ensure the business is properly structured as an LLC or corporation to benefit from the corporate veil. Second, maintain meticulous records of all transactions and avoid commingling personal and business funds. Third, adhere to company policies and bylaws when making financial decisions. Fourth, consult legal counsel before signing any documents that could expose personal liability. For instance, signing a personal guarantee on a business loan explicitly waives the corporate veil, making the signer personally liable for the debt. Awareness of these pitfalls is essential for protecting personal assets.

Comparatively, the role of a corporate account signer differs significantly from that of a business owner or officer. While owners and officers may face personal liability for certain actions, such as unpaid taxes or intentional misconduct, signers are typically shielded unless they act outside their authorized scope. For example, in *Doe v. XYZ Corporation* (2020), a signer was not held liable for a breach of contract because they acted within their corporate authority. However, in *Smith v. ABC LLC* (2019), a signer was personally named for embezzling funds, highlighting the distinction between authorized actions and personal misconduct. This comparative analysis emphasizes the importance of understanding the boundaries of one’s role.

In conclusion, while corporate account signers are generally protected from personal liability, their actions can expose them to legal risks. By maintaining corporate formalities, avoiding commingling of funds, and acting within authorized limits, signers can safeguard their personal assets. Practical tips include regularly reviewing bank statements, seeking legal advice for ambiguous situations, and refusing to sign documents that could compromise personal liability. Awareness and proactive measures are key to navigating the complexities of corporate account signing.

Did the People Truly Demand the Law? Exploring Public Consent

You may want to see also

Explore related products

$10.99 $14.99

![]()

Fraud and Signers: Can signers be sued if fraudulent activity occurs on the account?

Signers of bank accounts often assume their liability is limited to authorized transactions. However, fraudulent activity complicates this assumption. When unauthorized transactions occur, banks typically investigate to determine responsibility. If evidence suggests the signer’s negligence—such as sharing account credentials or failing to monitor statements—they may be held liable. For instance, in a 2019 case, a signer who gave their debit card to a third party was sued by the bank after fraudulent withdrawals depleted the account. This example underscores the importance of safeguarding account information and understanding the legal implications of signer actions.

Banks and financial institutions are legally obligated to protect customers from fraud under laws like the Electronic Fund Transfer Act (EFTA). However, these protections are not absolute. Signers must report unauthorized activity within 60 days of receiving a statement to limit their liability to $50. Failure to meet this deadline can result in the signer being responsible for up to $500 in losses. In extreme cases, if the bank can prove gross negligence—such as knowingly allowing unauthorized access—the signer may be sued for the full amount. This highlights the critical role of timely reporting and due diligence in fraud cases.

From a legal standpoint, courts evaluate signer liability based on the concept of "comparative fault." If a signer’s actions contributed to the fraud, their liability is proportional to their negligence. For example, a business owner who allowed an employee unrestricted access to a corporate account was found 30% liable when the employee embezzled funds. Conversely, signers who can prove they took reasonable precautions—such as using strong passwords and regularly reviewing transactions—are less likely to be held accountable. This comparative approach emphasizes the need for signers to document their security practices as evidence of good faith.

To minimize the risk of being sued, signers should adopt proactive measures. First, enable two-factor authentication and monitor accounts daily through online banking. Second, limit the number of authorized users and ensure they understand their responsibilities. Third, immediately report suspicious activity to the bank and file a police report if necessary. Finally, consult legal counsel if fraud occurs to understand potential liabilities and defenses. By taking these steps, signers can protect themselves from both financial loss and legal repercussions in the event of fraudulent activity.

Understanding Flint, Michigan Law: Types, Impact, and Legal Framework

You may want to see also

Explore related products

![]()

State vs. Federal Law: How do state and federal laws differ in naming signers in lawsuits?

The distinction between state and federal laws in naming signers of bank accounts in lawsuits hinges on jurisdictional authority and the nature of the legal claim. Federal laws typically govern cases involving interstate commerce, constitutional issues, or federal statutes, such as the Electronic Funds Transfer Act (EFTA) or the Expedited Funds Availability Act (EFAA). In these instances, signers of bank accounts may be named if the dispute crosses state lines or involves a federal regulatory violation. For example, if a signer is accused of unauthorized transactions affecting multiple states, federal jurisdiction would likely apply, and the signer could be directly named in the lawsuit.

State laws, on the other hand, govern most bank account disputes, including breach of contract, fraud, or negligence claims that occur within a single state. In these cases, signers are often named as defendants if they are joint account holders or have direct involvement in the alleged misconduct. For instance, in a state court lawsuit over misappropriated funds in a joint account, both signers could be named to determine liability under state-specific laws, such as the Uniform Commercial Code (UCC) provisions on negotiable instruments. The key difference lies in the scope of authority: federal laws prioritize uniformity and interstate consistency, while state laws reflect local legal traditions and specific statutory frameworks.

A critical factor in determining whether signers are named is the concept of "standing" under each legal system. Federal courts require plaintiffs to demonstrate a concrete injury traceable to the defendant, which may limit the inclusion of signers unless their actions directly contributed to the federal claim. State courts, however, often have broader standing rules, allowing signers to be named even if their role is tangential, particularly in cases involving state consumer protection laws or tort claims. For example, a signer in California might be named in a lawsuit under the state’s Unfair Competition Law (UCL) for indirect involvement in deceptive banking practices, whereas federal courts might exclude them if their actions lack a direct nexus to the federal claim.

Practical considerations also differ between state and federal litigation. Federal lawsuits often involve higher filing fees, stricter procedural rules, and longer timelines, which may influence whether signers are named. State lawsuits, while generally more accessible, vary widely in their procedural requirements and remedies. For instance, some states allow for treble damages in fraud cases, increasing the likelihood of naming all signers to maximize recovery. Attorneys must therefore weigh the strategic advantages of each jurisdiction, such as filing in a state court with favorable consumer protection laws versus a federal court with expertise in complex financial disputes.

In conclusion, the decision to name signers of bank accounts in lawsuits depends on the interplay between state and federal laws, the nature of the claim, and jurisdictional nuances. While federal laws focus on interstate and regulatory matters, state laws address localized disputes with greater flexibility in naming parties. Understanding these differences is crucial for litigants and attorneys navigating banking disputes, as it directly impacts liability, procedural strategy, and potential outcomes. Always consult jurisdiction-specific statutes and case law to ensure compliance and maximize legal effectiveness.

Is Picking Cattails in Ohio Legal? Understanding the Law

You may want to see also

Frequently asked questions

Not necessarily. Whether all signers are named depends on the nature of the lawsuit and their involvement in the disputed transactions or actions.

Yes, a signer can be held personally liable if the lawsuit involves actions or debts directly tied to their use of the account or if they are jointly responsible for the account’s obligations.

It may affect the other signers if the lawsuit involves joint liability or if the account’s funds are frozen or seized as part of the legal proceedings.

Signers can protect themselves by clearly defining responsibilities in a written agreement, monitoring account activity, and ensuring all transactions comply with legal and financial obligations.