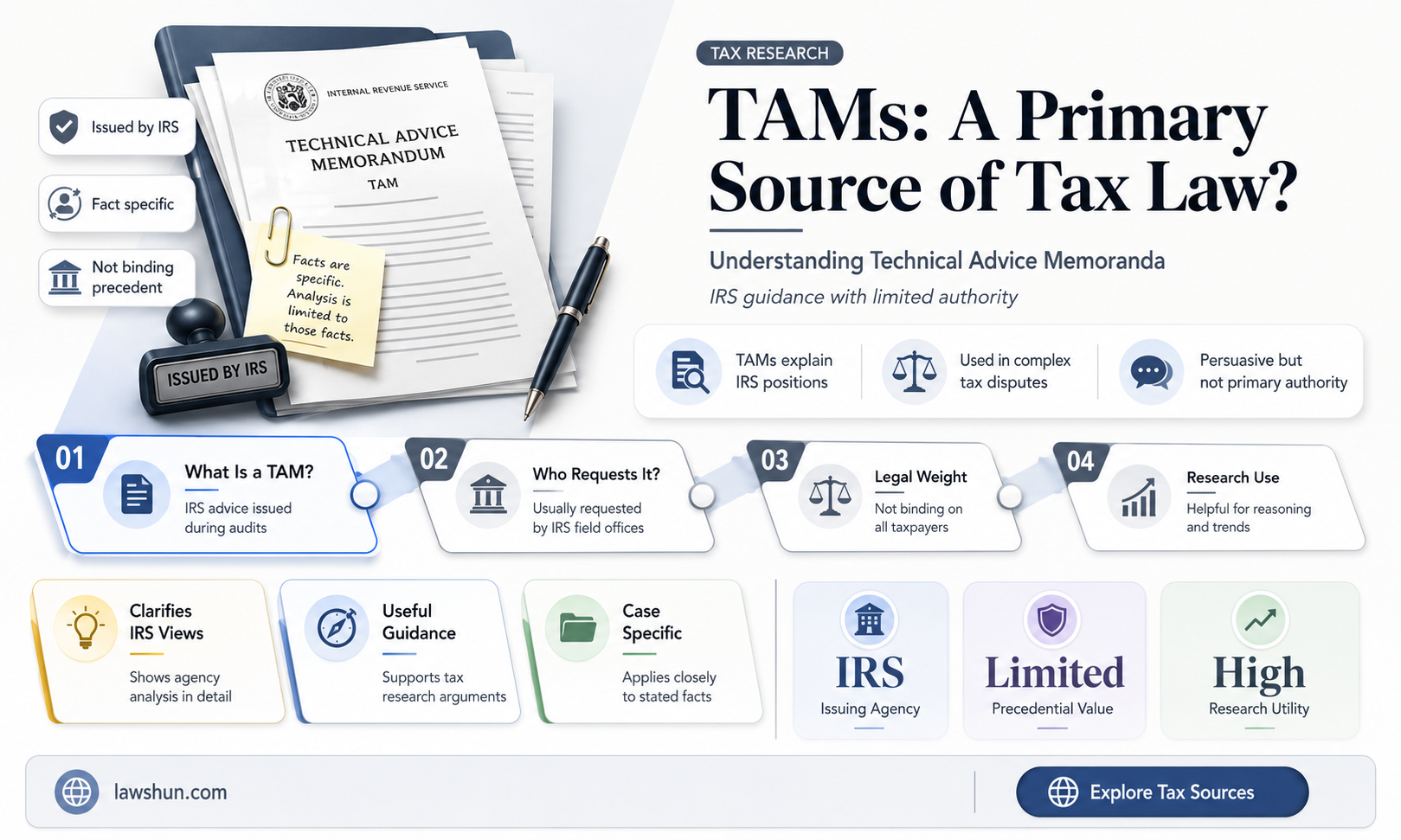

Technical Advice Memorandums (TAMs) are not primary sources of tax law. The primary sources of tax law include the Internal Revenue Code, U.S. Treasury Regulations, Revenue Rulings, Revenue Procedures, and primary judicial sources such as the Supreme Court of the United States, Courts of Appeal, District Courts, and the U.S. Tax Court. TAMs, on the other hand, are secondary sources that are issued by the Office of Chief Counsel upon the request of an IRS director or an area director appeals. They provide guidance on the interpretation and application of tax laws for closed transactions and represent the final determination of the IRS on a specific issue.

| Characteristics | Values |

|---|---|

| Type | Technical Advice Memorandum (TAM) |

| Source | Office of Chief Counsel |

| Requested by | IRS director or area director appeals |

| Requested after | A return has been filed, often with an ongoing examination |

| Applicable to | Closed transactions |

| Binding | Yes, but only on the specific issue at hand |

| Availability | Public, after personally identifiable information is removed |

| Use | To provide guidance on the interpretation and application of tax laws |

Explore related products

What You'll Learn

![]()

TAMs are binding on everyone

TAMs, or Technical Advice Memorandums, are a type of secondary source in tax law. They are issued by the Office of Chief Counsel or the Office of Associate Chief Counsel upon the request of an IRS director or an area director appeals. TAMs are requested after a tax return has been filed, often in conjunction with an ongoing examination.

TAMs are often requested when there is a need for clarification on a specific issue involving a taxpayer's return, a claim for a refund or credit, or any other matter within the jurisdiction of the territory manager or area director appeals. They are particularly useful when a taxpayer's circumstances are similar to those at issue in the guidance.

It is important to note that TAMs are not considered precedent and should not be relied upon as such in the disposition of other cases. However, they do provide valuable insight into the IRS's position on the law and serve as a guide for similar situations. TAMs are made available to the public once personally identifiable information has been removed.

Jude Law and Rob Lowe: Are They Related?

You may want to see also

Explore related products

$12.49 $21.99

![]()

TAMs are issued on closed transactions

TAMs, or Technical Advice Memorandums, are issued on closed transactions and are a type of secondary source of tax law. They are requested by IRS area offices after a return has been filed, often in conjunction with an ongoing examination. TAMs are issued only on closed transactions and provide guidance on the proper interpretation and application of tax laws. They represent the final determination of an IRS attitude concerning a matter but are limited to the specific issue at hand.

TAMs are similar to Private Letter Rulings (PLRs) but differ in that PLRs come from a taxpayer's request for advice on a proposed transaction, whereas TAMs arise from IRS employees' requests for advice regarding the examination of a tax return. TAMs are also binding on everyone, whereas PLRs may not be relied upon as precedent by other taxpayers or IRS personnel.

TAMs are highly persuasive in nature and can be quite helpful when utilized correctly. They are made available to the public once personally identifiable information has been removed. TAMs issued after October 31, 1976, may be used as substantial authority to avoid the substantial understatement penalty.

Primary sources of tax law, on the other hand, are tax law authorities that must be followed. These include the Internal Revenue Code, Treasury Regulations, Revenue Rulings, and Revenue Procedures. The Internal Revenue Service publishes several types of agency guidance that interpret or apply the IRC, Treasury regulations, and case law. They can also establish procedures.

Open Carry Laws: When Did They Begin?

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UL320_.jpg)

![]()

TAMs are a final IRS determination

TAMs, or Technical Advice Memoranda, are a final determination of the IRS's position concerning a matter. However, they are only binding with respect to the specific issue addressed in the specific case. TAMs are issued only on closed transactions and provide guidance on the proper interpretation and application of tax laws, tax treaties, regulations, revenue rulings, or other precedents. They are generally made public after removing all personally identifiable information about the taxpayer.

TAMs are a type of secondary source in tax law. Primary sources of tax law include the Internal Revenue Code, U.S. Treasury Regulations, Revenue Rulings, and Revenue Procedures. These sources are considered the most impactful and binding types of authority in tax law. They are issued by the Internal Revenue Service (IRS) and the Treasury Department to provide guidance for new legislation or to address issues arising from existing Internal Revenue Code sections.

Secondary sources, on the other hand, are never binding law but can be persuasive when utilized correctly. In addition to TAMs, other examples of secondary sources include private letter rulings (PLRs), journal and law review articles, treatises, and IRS publications. PLRs are written statements issued to taxpayers that interpret and apply tax laws to a taxpayer's specific set of facts. They are binding on the IRS if the taxpayer accurately described the proposed transaction and carried it out as described.

While TAMs are a final IRS determination on a specific issue, they may be relied upon with caution. It is important to ensure that the fact pattern in question is similar to the one addressed in the TAM. Additionally, there is a risk that the IRS could argue differently in certain circumstances.

Contract Law: What's Its Purpose?

You may want to see also

Explore related products

![]()

TAMs are not precedent

TAMs, or Technical Advice Memorandums, are not considered precedent in tax law. They are a type of secondary source that provides guidance and interpretation of tax laws for specific cases. TAMs are issued by the Office of Chief Counsel or the Office of Associate Chief Counsel in response to requests from IRS directors or area directors for advice on technical or procedural questions that arise during a taxpayer's proceeding. They are typically requested after a tax return has been filed and are related to the examination of that return, a taxpayer's claim for a refund or credit, or other matters involving a specific taxpayer.

While TAMs represent the final determination of the IRS's position on a matter, they are limited in scope to the specific issue addressed and are not binding on other cases. TAMs are highly persuasive and can be used as a guide or source of insight into the IRS's interpretation of tax laws. However, they are not considered precedent in the same way that primary sources, such as the Internal Revenue Code, Treasury Regulations, Revenue Rulings, and Revenue Procedures, are binding and must be followed.

The weight of authority of different sources in tax planning is critical to understand. While TAMs can provide valuable guidance and insight, they do not carry the same weight as primary sources of tax law. Primary sources are the highest form of authority and are binding, meaning they must be followed. These include the Internal Revenue Code, Treasury Regulations, Revenue Rulings, and Revenue Procedures, as well as judicial sources such as the Supreme Court of the United States, Courts of Appeal, District Courts, and the U.S. Tax Court.

It is important to distinguish between the different types of sources and their respective authority. While TAMs can be influential and persuasive, they do not set a binding precedent for future cases or interpretations of tax law. Each TAM is specific to the circumstances of the case for which it was issued and should be understood in that context. This specificity is a key feature of TAMs, as they are designed to address particular issues and provide guidance on the proper interpretation and application of tax laws for those specific situations.

In summary, TAMs are not precedent in tax law. They are secondary sources that provide guidance and interpretation of tax laws for specific cases. While they represent the final determination of the IRS's position on a particular matter, they are limited in scope and are not binding on other cases. The weight of authority lies with primary sources, which are the highest form of authority in tax law and must be followed. Understanding the distinction between primary and secondary sources, and their respective authority, is crucial in tax planning and interpretation.

Understanding Legal Capacity: Key to Contract Law

You may want to see also

Explore related products

![]()

TAMs are highly persuasive

TAMs, or Technical Advice Memorandums, are not primary sources of tax law. However, they are highly persuasive in nature. TAMs are requested by IRS area offices after a return has been filed, often in conjunction with an ongoing examination. They are similar to private letter rulings (PLRs) but differ in that they arise from IRS employees' requests for advice regarding the examination of a tax return.

TAMs are issued only on closed transactions and provide guidance on the proper interpretation and application of tax laws, tax treaties, regulations, revenue rulings, or other precedents. They represent the final determination of an IRS attitude concerning a matter but are limited to the specific issue addressed. TAMs are binding on everyone involved in the specific issue but are not to be applied or relied upon as a precedent in other cases. However, they provide valuable insight into the Service's position on the law and serve as a guide.

In summary, while TAMs are not primary sources of tax law, they play a significant role in tax planning due to their highly persuasive nature. They offer guidance, insight, and authority that taxpayers and practitioners can utilize to navigate the complexities of tax planning effectively.

Nevada HR Laws: Unique or Universal?

You may want to see also

Frequently asked questions

Technical Advice Memorandums (TAMs) are issued by the Office of Chief Counsel upon the request of an IRS director or an area director appeals in response to technical or procedural questions that develop during a taxpayer’s proceeding.

No, TAMs are not a primary source of tax law. Primary sources of tax law include the Internal Revenue Code, U.S. Treasury Regulations, Revenue Rulings, and Revenue Procedures.

Examples of primary sources of tax law include the Internal Revenue Code, U.S. Treasury Regulations, Revenue Rulings, Revenue Procedures, and Notices.

Yes, TAMs are binding on everyone. They represent the final determination of the IRS but are limited to the specific issue at hand.

TAMs are issued only on closed transactions and provide guidance on the interpretation and application of tax laws. On the other hand, PLRs are issued before a transaction is consummated or before a taxpayer's return is filed and are not binding precedent.