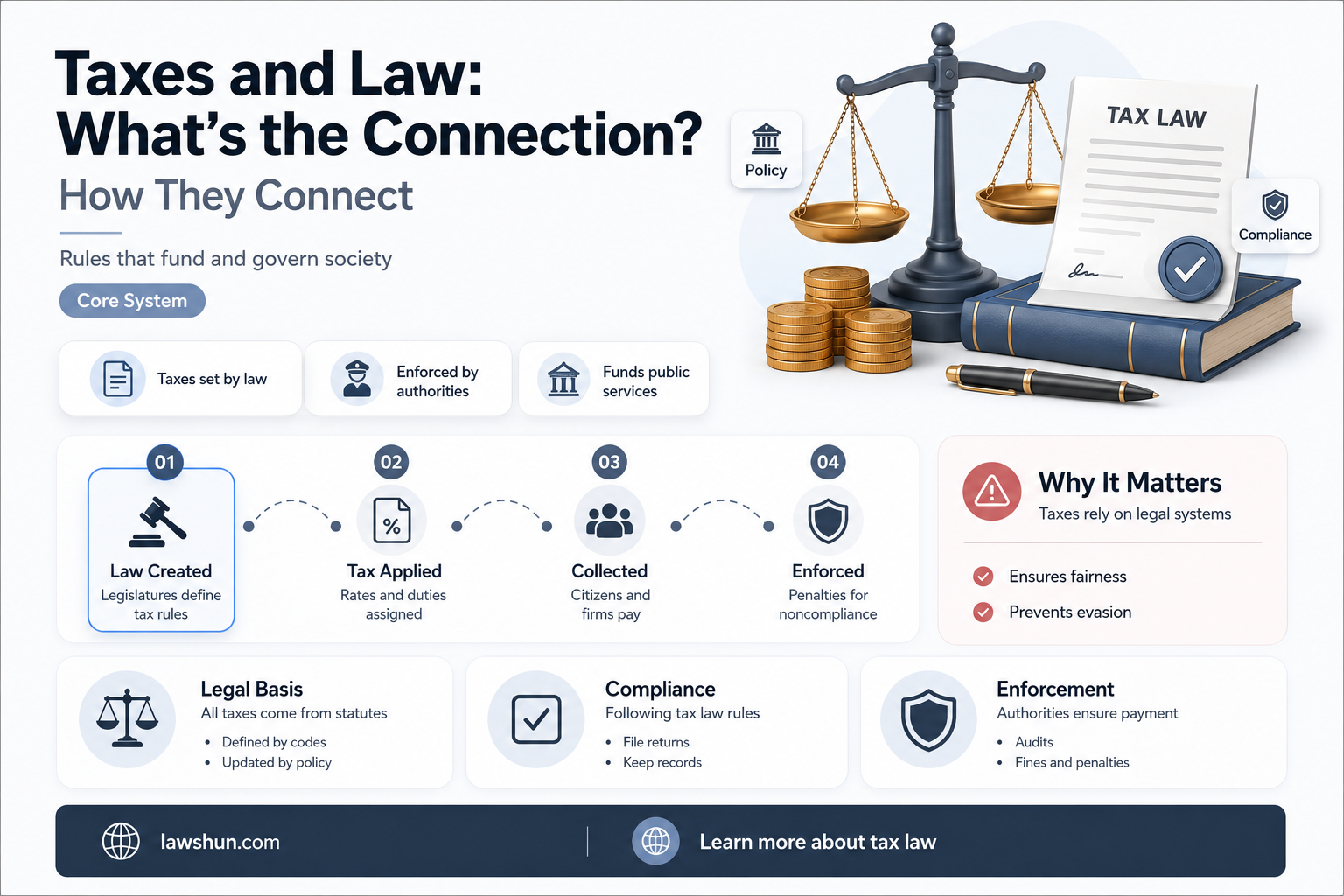

Taxation is a complex area of law that deals with the legal aspects of taxation, including the application of existing tax laws on individuals, entities, and corporations. The power to impose taxes is generally recognized as a right of governments, and tax laws are created through a political process. These laws outline the rules and procedures for assessing and collecting taxes, such as income tax, estate tax, business tax, and property tax. While tax laws aim to generate revenue, they are also subject to criticism for their complexity and potential negative impact on economic growth. The study of tax law is a specialization for professionals such as accountants, tax agents, and lawyers, who advise individuals and organizations on their legal obligations and rights regarding taxation.

| Characteristics | Values |

|---|---|

| Definition | Tax law is a body of rules and procedures (laws) that public authorities use to assess and collect taxes. |

| Complexity | Taxes are generally complex and can benefit high-income earners more than low-income earners. |

| Education | Tax law is a specialization for accountants, tax agents, and lawyers. |

| Political Nature | Tax law is concerned with the legal aspects of taxation, while decisions on the merits, levels, and rates of taxes are political. |

| Historical Development | Tax law has evolved relatively recently due to the expanding role of modern states in economic, social, and cultural matters. |

| Constitutional Limits | The power to tax is generally a right of governments, but its limits are set by constitutional law, with the legislature holding this power in democratic systems. |

| International Aspects | International tax law addresses issues of double taxation when an individual or corporation is taxed in multiple countries. |

| Enforcement Challenges | Some individuals and groups have encouraged non-compliance with tax laws, and tax evasion and avoidance reduce government revenue. |

| Academic Study | Tax law is an area of legal study, with courses available at the undergraduate and graduate levels, including Master of Laws (LL.M.) programs. |

Explore related products

What You'll Learn

![]()

Tax law education and qualifications

Tax law is an area of legal study that deals with the legal aspects of taxation. It covers the application of existing tax laws on individuals, entities, and corporations in areas where tax revenue is derived or levied, such as income tax, estate tax, business tax, and property tax.

A career in tax law requires a strong academic background and a commitment to years of study and training. Here is a general overview of the educational path for becoming a tax attorney, a legal professional specializing in tax law:

Undergraduate Degree

To apply to law school, you typically need to earn a bachelor's degree. Although law schools may not require a specific major, choosing a relevant field such as accounting, political science, or finance can provide a solid foundation for understanding tax fundamentals. Maintaining a high GPA and building a well-rounded resume through extracurricular activities, internships, and volunteer work are also important for a competitive law school application.

Law School Admissions Test (LSAT)

The LSAT is a crucial component of the law school application process in many countries, including the United States and Canada. It assesses analytical reasoning, reading, and critical thinking skills. A high LSAT score can significantly improve your chances of gaining admission to a law school of your choice.

Juris Doctor (JD)

After completing your undergraduate degree and LSAT, you can pursue a Juris Doctor (JD) degree through an accredited law school. This typically involves a three-year full-time program, during which you will study basic law subjects in the first year and then move on to elective courses, internships, and clinical experiences in the following years.

Master of Laws in Taxation (LL.M.)

Following the completion of your JD degree, you may choose to further specialize in tax law by pursuing a Master of Laws in Taxation (LL.M.). This is a one-year program that can provide in-depth knowledge and expertise in tax law.

Bar Exam

The final step in becoming a qualified tax attorney is passing the Bar exam. This exam allows you to obtain your license to practice law and provide legal services to clients as a tax attorney.

It is important to note that the specific requirements and duration of each educational step may vary depending on the country and law school. Additionally, continuing education is often necessary for tax attorneys to stay updated with the latest changes in tax laws and regulations throughout their careers.

Mastering Constitutional Law: Strategies for Success

You may want to see also

Explore related products

$12.49 $21.99

![]()

Tax evasion and avoidance

Taxes are a form of law, and tax law is an area of legal study in which public or sanctioned authorities, such as federal, state, and municipal governments, use a body of rules and procedures to assess and collect taxes in a legal context. Tax evasion and avoidance are two different ways in which individuals or businesses may avoid paying taxes.

Tax evasion refers to illegal practices used to avoid paying taxes. It involves deliberately hiding income, inflating deductions, or providing false information on tax returns. It crosses legal boundaries and constitutes fraud. Common examples of tax evasion include not reporting cash payments, hiding assets in offshore accounts, or maintaining two sets of financial books. Tax evasion can lead to severe penalties, including criminal investigations, prosecution, court-imposed fines, jail time, and a criminal record.

On the other hand, tax avoidance refers to legal methods of reducing tax liability within the framework of tax laws. Unlike evasion, avoidance uses legitimate deductions, exemptions, and benefits provided by the tax system. It follows the letter of the law while minimizing tax burdens. Examples of tax avoidance include investing in tax-saving instruments, claiming legal deductions, or investing in a home to claim interest deductions. Understanding the difference between tax evasion and avoidance is crucial, especially when seeking housing finance. Proper tax avoidance strategies can strengthen an individual's financial profile and increase loan eligibility.

To combat tax evasion and avoidance, countries implement various measures such as global standards for the automatic exchange of financial information, enhancing mandatory disclosure rules, and implementing rules to prevent large corporations from obtaining unfair advantages. These measures aim to ensure greater tax certainty, transparency, and fairness on a global scale.

Bar vs Bench: Understanding the Legal Divide

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UL320_.jpg)

![]()

Tax law and consumer law

Taxes are a form of law, and tax law is an area of legal study in which public or sanctioned authorities, such as federal, state, and municipal governments, use a body of rules and procedures (laws) to assess and collect taxes. Tax law falls within the domain of public law, which governs the activities and reciprocal interests of the political community and its members. It covers the application of existing tax laws on individuals, entities, and corporations in areas where tax revenue is derived or levied, such as income tax, estate tax, business tax, and property tax.

The power to impose taxes is generally recognized as a right of governments, and the tax law of a nation is usually unique to it. While there are similarities and common elements across countries, international tax law addresses issues that arise when an individual or corporation is taxed in several countries. The rates and merits of various taxes are attained through the political process and are not directly attributable to the domain of tax law.

Consumer taxes, which are a type of tax addressed by consumer law, frequently change due to fiscal needs and political expediency. These include excise taxes, which are levied on specific categories of goods such as cigarettes, gasoline, and marijuana. Consumer taxes can also be used to influence behaviour, such as in the case of "sin" taxes, which target behaviour believed to be immoral or unhealthy.

The study of tax law is a specialization for accountants, tax agents, and lawyers. In some countries, a Bachelor of Laws (LL.B.) is the typical undergraduate law degree, after which graduates may pursue a Master of Laws (LL.M.) or a Juris Doctor (JD) to become practitioners of the law.

Escrow in Contract Law: How It Works

You may want to see also

Explore related products

![]()

Historical origins of tax law

The historical origins of tax law date back to ancient civilizations, with the first records of taxation found in ancient Egypt around 3000 BCE. Egyptian pharaohs employed collectors or scribes to impose levies on goods and produce, such as cooking oil and livestock. Archaeology also reveals that ancient Mesopotamia (modern-day Iraq) had tax records dating back to around 3300 BCE.

Ancient Greece and Rome are also known for their early tax systems. Greek city-states imposed taxes on commodities during wars or emergencies, and direct taxation was applied to those entitled to vote. In ancient Rome, the second Caesar, Augustus, introduced a wealth tax on Roman citizens, distinguishing between nationals and residents of conquered territories. Tariffs, or taxes on imported goods, were also significant in Roman times and were used to control the trade of goods like wool, leather, and cheese.

In medieval Europe, rulers like England's William the Conqueror imposed property taxes to raise funds for protection against invaders. International trade and tariffs were crucial sources of revenue, with the earliest tariffs dating back to 3000-2000 BCE in the ancient city of Kanesh (modern-day Turkey). Direct taxes were introduced in India before 300 BC, and ancient Chinese civilizations imposed levies on property, with 10% of cultivated land going to emperors.

The history of taxation in the United States began with tariffs, including the ""Tariff of Abominations" in 1828, which increased tensions between the North and South. The need to finance the Civil War led to the first income tax in 1862, signed into law by President Lincoln. This version was repealed in 1872, but income tax was reintroduced in 1894 with the Wilson Tariff Act, only to be deemed unconstitutional by the Supreme Court. The 16th Amendment to the U.S. Constitution in 1913 finally established the federal income tax.

Taxation has been a subject of political controversy, with instances like the rebellion of American colonies against Great Britain's taxation without representation, and the French Revolution of 1789, where tax inequities played a significant role. Wars have often influenced tax policies, with income tax introduced in Britain in 1799 and the withholding method of income tax collection originating as a wartime innovation in several countries.

Constitutional Law: Complexities of a Nation's Legal Foundation

You may want to see also

Explore related products

![]()

Tax law and economic models

Taxes are a form of law, and tax law is an area of legal study in which public authorities such as federal, state, and municipal governments use a body of rules and procedures to assess and collect taxes. The power to impose taxes is generally recognized as a right of governments, and tax laws are created through a political process.

Economic and tax modelling programs are used to educate lawmakers and the public about the trade-offs in tax policy and their impact on taxpayers and the economy. Dynamic scoring is an example of an analytical tool that can be used to make informed decisions about policy changes. For example, the Tax Foundation uses a General Equilibrium Model, known as the Taxes and Growth (TAG) Model, to simulate the effects of government tax and spending policies on the economy and government revenues.

The relationship between taxation and economic growth has been a subject of interest, with some arguing that lower taxes promote economic growth. Supply-side economics and neoclassical models, prominent in the 1970s and 1980s, championed the idea that taxes hinder economic growth. However, empirical evidence has sometimes shown the opposite effect, with increases in top tax rates coinciding with growth in the bottom 99% of incomes.

The 2017 Tax Cuts and Jobs Act (TCJA), which lowered the corporate tax rate from 35% to 21%, was a significant test case for the theory that tax rates affect economic growth. While the Trump administration predicted positive effects on output and investment, the act did not appear to boost economic growth and instead reduced government revenue and increased inequality.

Tax law education is a specialization for accountants, tax agents, and lawyers, who must complete courses in taxation law and financial services. Understanding tax law and economic modelling is crucial for policymakers to make informed decisions that promote economic growth and fiscal responsibility.

Lawmaking: India vs England

You may want to see also

Frequently asked questions

Tax law is an area of legal study in which public authorities, such as federal, state, and municipal governments, use a body of rules and procedures (laws) to assess and collect taxes. Tax law falls within the domain of public law, which determines and limits the activities and interests of the political community.

The purpose of tax law is to provide a legal framework for the assessment and collection of taxes. Taxes are a form of revenue for the government, and tax law ensures that taxpayers transfer a portion of their income or property to the governing authority.

Tax law is primarily concerned with the legal aspects of taxation, such as the rules and procedures for assessing and collecting taxes. It does not directly address the financial, economic, or other implications of taxation. Additionally, tax law is unique to each nation, although there may be similarities between different countries' tax laws.

Yes, the historical origins of tax law are closely tied to the principles of political liberty and representative government. The idea of "no taxation without consent" was established in the Declaration of Independence of the United States and the English Bill of Rights of 1689. The British system of income taxation, for example, dates back to 1799 as a temporary measure during the Napoleonic Wars.