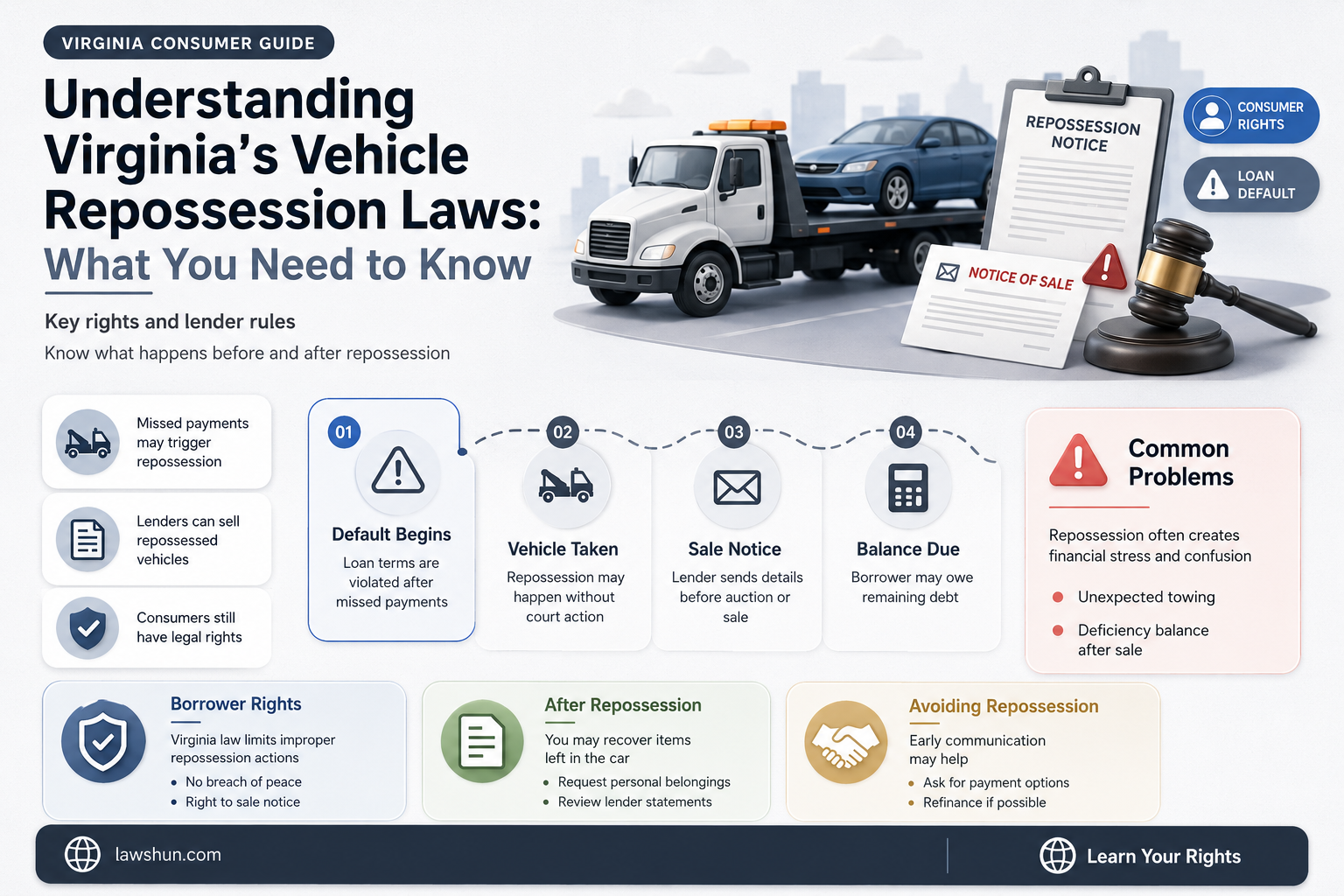

In Virginia, the repossession of a vehicle is governed by specific laws designed to protect both lenders and borrowers. Under Virginia law, if a borrower defaults on a car loan, the lender has the right to repossess the vehicle without prior notice, provided the repossession is conducted peacefully and without breaching the peace. However, lenders must follow certain procedures, such as ensuring the borrower has indeed defaulted and adhering to state regulations regarding the sale of the repossessed vehicle. Additionally, borrowers have rights, including the opportunity to redeem the vehicle by paying the outstanding balance before it is sold, and they may also be entitled to any surplus funds if the sale exceeds the debt owed. Understanding these laws is crucial for both parties to navigate the repossession process fairly and legally.

| Characteristics | Values |

|---|---|

| State | Virginia (VA) |

| Repossession Laws | Governed by Virginia Code § 46.2-710 and § 6.2-2200 et seq. |

| Notice Requirement | No prior notice required before repossession if the borrower defaults. |

| Breach of Peace | Repossession cannot involve a breach of peace (e.g., violence or trespassing). |

| Post-Repossession Notice | Lender must provide written notice within 5 days of repossession. |

| Redemption Period | Borrower has the right to redeem the vehicle before sale by paying the outstanding balance. |

| Sale of Vehicle | Lender must sell the vehicle in a commercially reasonable manner. |

| Deficiency Balance | Lender can sue for the difference between sale proceeds and loan balance. |

| Personal Property in Vehicle | Lender must allow borrower to retrieve personal items left in the vehicle. |

| Voluntary Repossession | Borrower can voluntarily surrender the vehicle to avoid repossession fees. |

| Military Protections | Servicemembers Civil Relief Act (SCRA) provides additional protections for active-duty military. |

| Legal Recourse | Borrower can sue for damages if repossession violates state or federal laws. |

| Credit Reporting | Repossession can negatively impact the borrower's credit score. |

| Latest Update | Laws are current as of October 2023 (verify for the most recent updates). |

Explore related products

What You'll Learn

![]()

Virginia Repossession Laws Overview

In Virginia, vehicle repossession is governed by a specific set of laws designed to balance the rights of lenders and borrowers. Understanding these laws is crucial for both parties involved in a loan agreement, as they outline the legal process for repossession and the protections afforded to consumers. One key aspect is that Virginia allows lenders to repossess a vehicle without prior notice to the borrower, provided the repossession is conducted peacefully and without breaching the peace. This means that lenders can hire a repossession agent to take the vehicle from public or private property, but they cannot use force or enter locked premises to do so.

For borrowers, knowing your rights under Virginia law can help prevent unnecessary complications. If your vehicle is repossessed, the lender must provide written notice within 5 days, detailing the amount owed, repossession expenses, and the deadline to redeem the vehicle. This notice also informs you of your right to dispute the repossession if you believe it was conducted unlawfully. For instance, if the repossession involved a breach of peace or if you were not in default, you may have grounds to challenge the action. It’s essential to act promptly, as Virginia law allows borrowers a limited time to reclaim their vehicle by paying the full balance, including fees.

A critical distinction in Virginia’s repossession laws is the treatment of deficiency balances. If the lender sells the repossessed vehicle and the sale proceeds do not cover the outstanding loan balance, they may seek a deficiency judgment against the borrower. However, the lender must provide proof that the vehicle was sold in a "commercially reasonable manner," such as through a public auction or private sale at fair market value. Borrowers have the right to contest the deficiency amount if they believe the sale was not conducted properly, which can significantly reduce their financial liability.

Practical tips for borrowers include keeping detailed records of payments and communications with the lender, as these can be invaluable if a dispute arises. Additionally, if you’re facing repossession, consider negotiating with the lender for a repayment plan or voluntary surrender of the vehicle, which may minimize fees and damage to your credit. For lenders, adhering strictly to Virginia’s repossession laws not only ensures compliance but also helps maintain a positive reputation and reduces the risk of legal challenges. In both cases, consulting with an attorney specializing in consumer law can provide clarity and protect your interests.

In summary, Virginia’s repossession laws are designed to provide a fair framework for resolving loan defaults involving vehicles. By understanding the legal requirements for repossession, notice, and deficiency judgments, both borrowers and lenders can navigate the process more effectively. Whether you’re aiming to protect your rights or enforce a loan agreement, familiarity with these laws is essential for achieving a just outcome.

Colonial Reactions to the 1650 Navigation Law: Resentment and Resistance

You may want to see also

Explore related products

![]()

Notice Requirements Before Repossession

In Virginia, lenders must adhere to specific notice requirements before repossessing a vehicle, ensuring borrowers are informed and given a chance to remedy defaults. Under Virginia law, a lender typically cannot repossess a vehicle without first providing written notice to the borrower. This notice must clearly state the borrower’s delinquency, the amount owed, and a deadline to bring the account current, usually at least 10 days from the notice date. Failure to comply with these notice requirements can render the repossession unlawful, potentially exposing the lender to legal penalties or claims for damages.

The notice must be delivered in a manner that ensures the borrower receives it, such as via certified mail with return receipt requested or personal delivery. Email or verbal notifications are generally insufficient under Virginia law. Borrowers should carefully review the notice upon receipt, as it serves as their official warning before repossession proceedings begin. If the notice is unclear or incomplete, borrowers may have grounds to challenge the repossession in court.

One critical aspect of the notice is its timing. Lenders cannot initiate repossession until the notice period has expired. For example, if the notice grants the borrower 10 days to pay the outstanding balance, repossession cannot occur until after that period. Borrowers should use this time wisely, either by paying the overdue amount or negotiating with the lender to avoid repossession. Ignoring the notice will likely result in the lender taking swift action to reclaim the vehicle.

Practical tip: If you receive a repossession notice, document everything. Keep a copy of the notice, track all communications with the lender, and note the dates and times of any interactions. This documentation can be invaluable if the lender violates notice requirements or if you need to dispute the repossession later. Additionally, consider consulting an attorney specializing in consumer law to review the notice and ensure your rights are protected.

In summary, Virginia’s notice requirements before repossession are designed to protect borrowers from unfair practices. Lenders must provide clear, written notice with a reasonable deadline for the borrower to address the default. Borrowers who understand these requirements and act promptly can minimize the risk of losing their vehicle and potentially negotiate a resolution with the lender. Ignoring the notice, however, leaves borrowers vulnerable to immediate repossession and further financial consequences.

Judicial Perspectives on Law: Shaping Law Professor Roles and Influence

You may want to see also

Explore related products

![]()

Post-Repossession Rights of Owners

In Virginia, once a vehicle is repossessed, owners are not left without recourse. The law provides specific post-repossession rights to ensure fairness and protect consumers from predatory practices. Understanding these rights is crucial for anyone facing this situation, as they dictate how to respond and potentially recover from the repossession.

Notification and Redemption Period: After repossession, Virginia law requires the lender to notify the owner in writing within 15 days. This notice must include details about the repossession, the amount owed, and the owner’s right to redeem the vehicle. Owners have a limited time—typically 60 days—to pay the outstanding balance, including fees, to reclaim their vehicle. This redemption period is a critical window, and failing to act within it may result in the lender selling the vehicle.

Right to Surplus or Liability for Deficiency: If the lender sells the repossessed vehicle, the owner has rights depending on the sale outcome. If the sale generates a surplus (the sale price exceeds the debt), the lender must return the excess to the owner. Conversely, if the sale results in a deficiency (the debt exceeds the sale price), the lender may seek a deficiency judgment against the owner. However, the owner has the right to contest this in court, particularly if the sale was not conducted commercially reasonably, as required by law.

Disputing Unfair Practices: Owners can challenge the repossession if they believe it was conducted unlawfully. For instance, if the lender breached the peace during repossession or failed to provide proper notice, the owner may have grounds for legal action. Consulting an attorney to review the circumstances and potential violations of the Virginia Consumer Protection Act or federal laws like the Fair Debt Collection Practices Act is advisable.

Practical Steps for Owners: To navigate post-repossession rights effectively, owners should first review their loan agreement and all communications from the lender. Document every interaction and keep records of payments made. If redemption is an option, calculate the total amount required and explore financial resources to meet the deadline. For those facing a deficiency judgment, gathering evidence of the vehicle’s fair market value and the sale’s reasonableness can strengthen a defense in court.

In summary, Virginia’s post-repossession laws offer owners a framework to protect their interests, but proactive and informed action is essential. Whether redeeming the vehicle, disputing a deficiency, or challenging the repossession, understanding these rights empowers owners to make strategic decisions in a stressful situation.

Dubai's Child Protection Laws: Safeguarding Minors and Legal Framework Explained

You may want to see also

Explore related products

![]()

Deficiencies and Surplus Funds

In Virginia, when a lender repossesses a vehicle, the sale of that vehicle often results in either a deficiency or a surplus. Understanding these outcomes is crucial for both borrowers and lenders, as they dictate financial responsibilities and potential benefits post-repossession. A deficiency occurs when the sale proceeds fall short of covering the outstanding loan balance, while a surplus arises when the sale generates more than what is owed. Virginia law provides specific guidelines on how these situations are handled, ensuring fairness and clarity in the process.

For deficiencies, Virginia Code § 46.2-723 requires the lender to notify the borrower of the sale and the amount still owed. The borrower remains liable for this deficiency unless they can prove the sale was not conducted in a commercially reasonable manner. This means the lender must sell the vehicle through a fair and transparent process, such as a public auction, to maximize its value. Borrowers should carefully review the sale details provided by the lender to ensure compliance with these standards. If the sale was not commercially reasonable, the borrower may challenge the deficiency claim in court, potentially reducing or eliminating their liability.

Surplus funds, on the other hand, belong to the borrower. Under Virginia law, any amount exceeding the outstanding loan balance, plus repossession and sale expenses, must be returned to the borrower. Lenders are required to provide a detailed accounting of the sale and notify the borrower of the surplus within a reasonable time. Borrowers should promptly claim these funds, as failure to do so could result in complications. For instance, if the lender does not return the surplus, the borrower may need to take legal action to recover the money.

Practical tips for borrowers include keeping detailed records of all communications with the lender, including notices of sale and deficiency or surplus calculations. If facing a deficiency, borrowers should explore options like negotiating a settlement or seeking legal advice to dispute the claim. For surpluses, borrowers should act quickly to claim their funds and verify the accuracy of the lender’s accounting. Understanding these processes empowers borrowers to protect their financial interests and navigate repossession outcomes effectively.

In summary, deficiencies and surplus funds are critical aspects of vehicle repossession in Virginia, governed by specific legal requirements. Borrowers must be proactive in reviewing sale details, challenging deficiencies when appropriate, and claiming surpluses promptly. Lenders, meanwhile, must adhere to commercially reasonable sale practices and ensure transparency in handling both deficiencies and surpluses. By understanding these dynamics, both parties can mitigate risks and ensure a fair resolution in the repossession process.

Mastering Beer's Law: A Simple Guide to Finding Eb in Solutions

You may want to see also

Explore related products

![]()

Legal Remedies for Wrongful Repossession

In Virginia, wrongful repossession occurs when a creditor seizes a vehicle without adhering to the legal requirements outlined in state law. If your car was repossessed despite your compliance with the loan agreement, you may have grounds for legal action. Understanding your rights and the available remedies is crucial to recovering damages or reinstating your vehicle.

Identifying Wrongful Repossession in Virginia

Virginia law permits repossession without prior notice if the borrower defaults, but creditors must follow specific procedures. For instance, they cannot breach the peace during repossession, meaning no threats, violence, or illegal entry onto private property. Additionally, the creditor must provide a post-repossession notice detailing redemption rights and the vehicle’s sale terms. If these steps are skipped, or if the repossession occurred despite your payments being current, it may be deemed wrongful. Document all communications, payment records, and details of the repossession to support your claim.

Legal Remedies Available to Victims

Victims of wrongful repossession in Virginia can pursue several remedies under state and federal law. The primary federal statute, the Fair Debt Collection Practices Act (FDCPA), allows for damages up to $1,000 plus attorney fees if the creditor violated its provisions. Under Virginia law, you may file a lawsuit for conversion (unlawful taking of property) or breach of contract, seeking compensatory and, in some cases, punitive damages. If the creditor’s actions were particularly egregious, such as selling the vehicle without proper notice, the court may award additional penalties.

Steps to Take After Wrongful Repossession

Act promptly if you believe your vehicle was wrongfully repossessed. First, send a certified letter to the creditor demanding the return of the vehicle and outlining the legal violations. If they refuse, consult an attorney specializing in consumer law to file a lawsuit. In court, you’ll need to prove the repossession was unlawful, such as by showing you were not in default or the creditor breached the peace. Keep all related documents, including loan agreements, payment receipts, and correspondence with the creditor, as evidence.

Preventive Measures and Practical Tips

To avoid wrongful repossession, stay current on payments and maintain detailed records of all transactions. If you anticipate difficulty making payments, contact your lender immediately to discuss alternatives, such as loan modification or deferment. Be cautious of predatory lending practices, and review your loan agreement for any clauses related to repossession. If repossession occurs, do not attempt to physically intervene; instead, focus on gathering evidence and seeking legal recourse. Proactive communication and documentation are your strongest defenses against wrongful repossession.

Clarksville, TN Cat Leash Laws: What Owners Need to Know

You may want to see also

Frequently asked questions

In Virginia, repossession is typically allowed without prior court approval if the borrower defaults on the loan. The lender or repossession agent must follow peaceful methods and cannot breach the peace, such as causing a disturbance or entering locked property.

A: Generally, a lender can repossess a vehicle if the borrower defaults on the loan agreement, which often includes missing payments. However, the specific terms depend on the contract. Missing a single payment may not always trigger repossession unless explicitly stated in the agreement.

A: Yes, repossession does not eliminate the debt. The lender may sell the vehicle and apply the proceeds to the loan balance. If the sale does not cover the full amount owed, you may still be responsible for the deficiency, plus any repossession and storage fees.