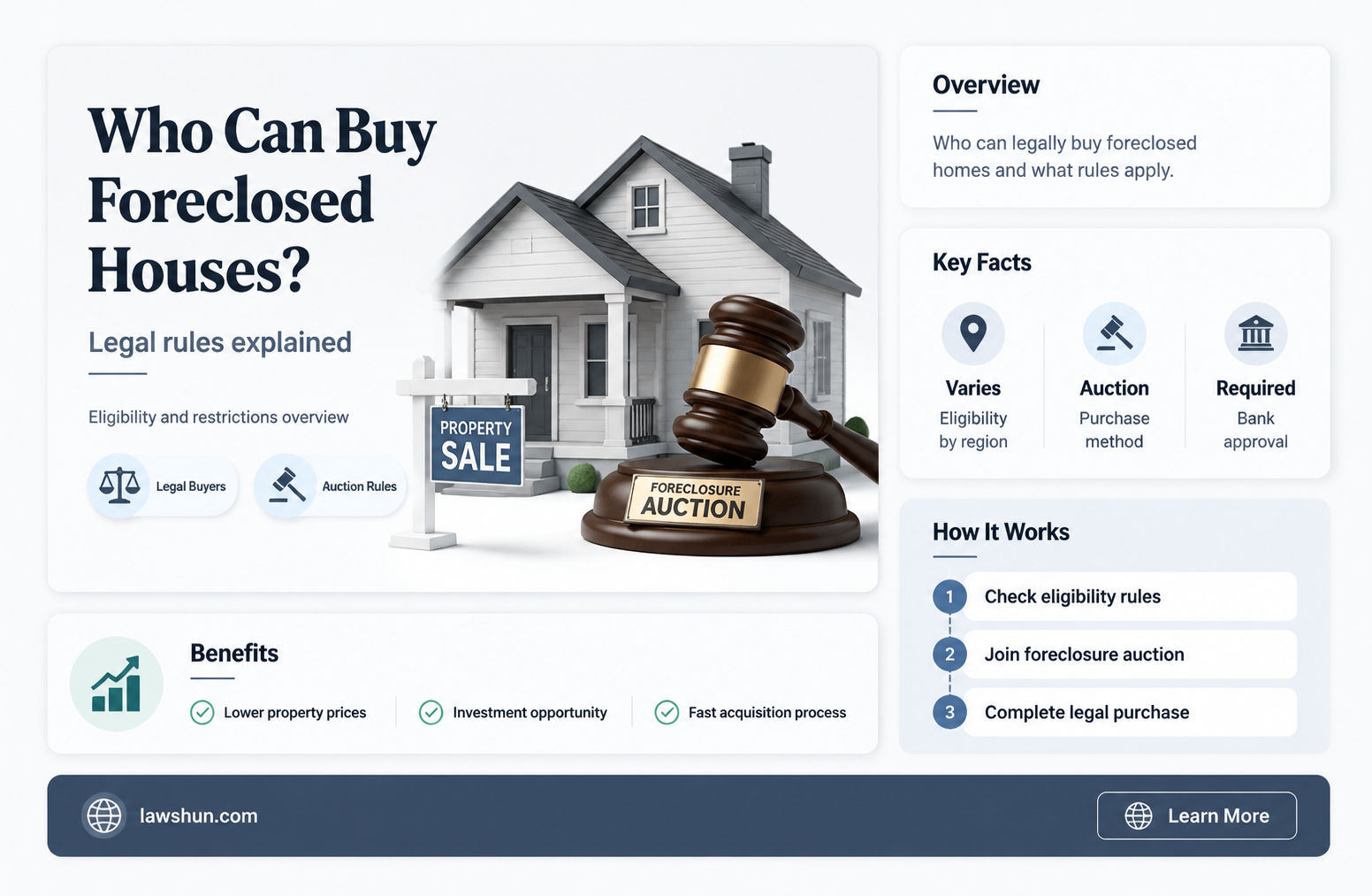

Buying a foreclosed home is a unique process that differs from buying a house owned by an individual. While it can be a fantastic investment option due to lower prices, there are legal complications and potential challenges that buyers should be aware of. Foreclosed homes are usually sold as is, which means that the buyer is responsible for any unforeseen issues, repairs, and maintenance. Understanding the laws and regulations specific to the state or region is crucial before purchasing a foreclosed home.

Explore related products

$10.95

What You'll Learn

![]()

Liens and delinquent taxes

A lien is a legal claim on a property, typically resulting from unpaid taxes or other debts. When a property owner fails to pay their taxes, government authorities may place a tax lien on the property, which can lead to a tax lien foreclosure if the owner does not resolve the debt. The government authorities issue a certificate for the lien, which can be sold at auction to a buyer who then has the legal right to collect the underlying debt, plus interest. This process can be complex and time-consuming, with specific technicalities, laws, and deadlines that vary across different states and localities.

In some cases, the original property owner may be granted a redemption period, during which they can pay off the lien and associated fees, thus regaining ownership of the property. However, if the debt remains unresolved, the lien holder can initiate judicial foreclosure proceedings and acquire the property. It is important to note that the government must be paid any delinquent taxes before the sale of a foreclosed property can proceed.

When purchasing a foreclosed home, it is essential to be aware of any existing liens and to understand that addressing these liens may require additional costs and paperwork. Furthermore, as foreclosed homes are typically sold "as is," buyers should be cautious of potential issues and unforeseen costs associated with repairs and maintenance.

To navigate the complexities of buying a foreclosed property with liens and delinquent taxes, it is advisable to seek guidance from a knowledgeable real estate agent and legal professionals experienced in foreclosure sales and real estate law.

Conflict of Interest Laws: Limiting Presidential Power?

You may want to see also

Explore related products

![]()

Title issues

Due to the nature of foreclosure, there may be title defects or claims that could affect your ownership rights. It is crucial to understand any liens or past-due taxes associated with the property, as these can become the responsibility of the new owner. Liens may be imposed by the Internal Revenue Service (IRS), the state, or other creditors, adding unexpected costs to the purchase.

Conducting a thorough title search is essential when buying a foreclosed home. Review county records to understand the property's ownership history and look for any liens, judgments, or administrative orders that may have survived foreclosure. Be cautious of any restrictions, leases, easements, or other agreements that may still be in effect. Securing title insurance is highly recommended, as it can provide protection against potential title issues.

Quitclaim Deeds and Special Warranty Deeds

When buying a foreclosed home, it is common to receive a quitclaim or special warranty deed instead of a general warranty deed. A quitclaim deed transfers the ownership interest of the seller to the buyer without providing any guarantees about the title. This means that the buyer assumes any risks associated with the title, including unresolved issues from the previous owner.

Legal Challenges

In some cases, the former owner of a foreclosed home may challenge the new owner's title through legal action. This can result in a lengthy and complex process, potentially requiring court intervention to clear the title and transfer it to the new owner.

State-Specific Variations

It is important to note that state laws and policies regarding foreclosure vary. Different states have different approaches to creditors' rights and foreclosure law, so it is advisable to consult with a local attorney or real estate professional familiar with the laws in your specific state.

Working Hours: Understanding Your Legal Work Day Limits

You may want to see also

Explore related products

![]()

Pre-foreclosure

When a house is in pre-foreclosure, it means that the bank or lender does not own it yet, and the homeowners still have the right to possession. At this stage, potential buyers can get in touch with the owner and inspect the property before making an offer. Buyers can benefit from purchasing pre-foreclosure homes as they can get a good deal and have clear information about the property's condition and required renovations. However, there may be challenges, such as the need for extensive repairs or difficulties in obtaining financing due to the higher risks associated with these properties.

To find pre-foreclosure properties, potential buyers need to be persistent and creative. They can search public records, real estate websites, and local newspapers for notices of default or work with a real estate agent specialising in pre-foreclosures. It is important to research the neighbourhood to ensure it meets the buyer's expectations regarding crime rates, schools, and other factors.

Once a pre-foreclosure home is purchased, the previous homeowners typically have a period of time before they need to vacate the property. In some states, the previous owners may have the right to buy back the property at auction, even after it has been foreclosed upon. It is important for buyers to be aware of the laws and policies specific to their state when purchasing a pre-foreclosure home.

CDC's Legal Authority: Mandating Laws Explained

You may want to see also

Explore related products

![]()

Judicial vs non-judicial foreclosure

While there are no explicit laws about who can buy a foreclosed house, there are laws that govern the foreclosure process. The foreclosure process can be judicial or non-judicial, and it is important to understand the differences between the two.

Judicial Foreclosure

In a judicial foreclosure, the lender goes to court to obtain a judgment to foreclose on a property. The judicial foreclosure process takes place in court and can be lengthy, often taking several months or even years. The lender will bring a lawsuit, and a judge will review the evidence submitted by both sides. A hearing may be held to decide whether the homeowner is in default on the loan. If the parties cannot reach a settlement, and the court finds in favour of the lender, the court will enter a judgment of foreclosure, triggering a foreclosure sale. This process can give the homeowner time to repair their finances and develop contingency plans.

Non-Judicial Foreclosure

A non-judicial foreclosure is a process that takes place outside of court, unless the homeowner raises a defence. In this case, the homeowner will need to file a lawsuit in court to defend themselves. The non-judicial foreclosure process is typically faster and less expensive for the lender than the judicial process, often concluding within a few months or even sooner. In some states, a trustee typically handles a non-judicial foreclosure, and the lender designates this trustee in the deed of trust that the borrower signs when purchasing the home.

The choice between judicial and non-judicial foreclosure depends on various factors, including state laws, the complexity of the case, and the lender's preference. It is important to note that each state's procedures may vary, so seeking specific legal guidance is advisable when dealing with foreclosure.

A Widow's Dilemma: Marrying Her Brother-in-Law in Islam

You may want to see also

Explore related products

![]()

Lender complications

Another complication arises from the fact that private lenders are often reluctant to finance foreclosure deals due to the high risk associated with these properties. As a result, buyers may struggle to secure financing for their purchase. To address this issue, the Federal Housing Administration (FHA) offers 203(k) loans, which are designed to facilitate high-risk REO purchases. These loans allow buyers to finance both the home purchase and any necessary repairs with a single mortgage. The streamlined version of the 203(k) loan covers basic repairs, while the standard version is suitable for more extensive structural issues.

Furthermore, foreclosed homes are usually sold "'as is," meaning the buyer assumes responsibility for any unforeseen issues, repairs, and maintenance. This can result in additional costs and liabilities for the buyer, who may need to possess home repair skills or have a plan for extensive renovations. Title issues, such as defects or claims, can also affect ownership rights, adding to the complexity of the transaction.

To navigate these lender complications, buyers should consider working with a qualified foreclosure agent or a real estate agent experienced in foreclosure sales. These professionals can guide buyers through the unique challenges of purchasing a foreclosed property, including understanding the legal complications and potential liabilities associated with the transaction.

Law and Order: When Your Words Turn Toxic

You may want to see also

Frequently asked questions

Anyone can buy a foreclosed house. However, the process of acquiring a home through foreclosure is unique in its legal complications and can be overwhelming to someone unfamiliar with the laws.

There are two main ways to buy a foreclosed house: at auction or from a bank or lender.

Foreclosed homes are often priced below market value to sell quickly, which can result in significant savings for the buyer. They can also be great investments as fixer-uppers, either to live in or to resell.

Foreclosed homes are usually sold "as is", so buyers are responsible for any repairs and maintenance. They may also come with legal complications, such as liens and delinquent taxes, and may have been poorly maintained or vandalised by the previous owners.