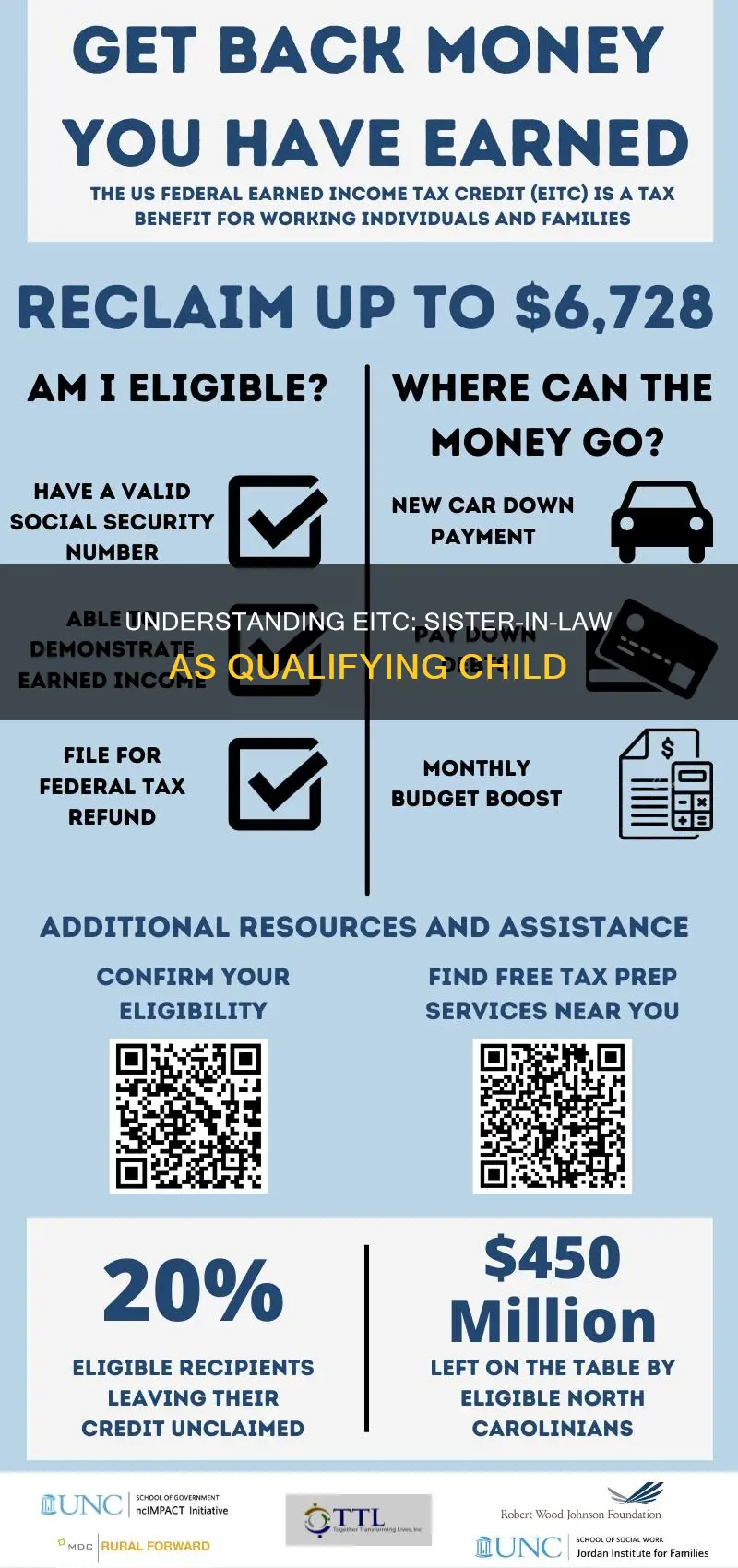

The Earned Income Tax Credit (EITC) is a refundable tax credit for low- to moderate-income workers with qualifying children. To be a qualifying child for the EITC, the child must be your son, daughter, stepchild, foster child, or a descendant of any of them. They can also be your brother, sister, half-sibling, step-sibling, or a descendant of any of them. The child must live in the same home as you in the United States for more than half of the tax year. They must also be under the age of 19 at the end of the year and younger than you, or under 24, a student, and younger than you. So, can a sister-in-law be a qualifying child for the EITC?

Explore related products

![]()

Relationship test

To be a qualifying child for the Earned Income Tax Credit (EITC), the child must be a son, daughter, stepchild, foster child, or a descendant of the taxpayer. This also includes the taxpayer's brother, sister, half-sibling, step-sibling, or a descendant of any of them.

The child must also meet the age, residency, and joint return tests. For the age test, the child must be under the age of 19 at the end of the year and younger than the taxpayer (or the taxpayer's spouse, if filing jointly). Alternatively, the child must be under the age of 24 at the end of the year, a full-time student, and younger than the taxpayer (or the taxpayer's spouse, if filing jointly). The child must also live in the same home as the taxpayer in the United States for more than half of the tax year. The child must not have filed a joint return with another person unless it is only to claim a refund of taxes withheld or estimated taxes paid.

In the case of a sister-in-law, she can only be a qualifying child if she meets the above requirements and is the sister of the taxpayer's spouse. If the sister-in-law is the taxpayer's own sister, she cannot be a qualifying child, but she may qualify as a dependent.

Secret Laws: Can Congress Keep Us in the Dark?

You may want to see also

Explore related products

![]()

Age test

To be a qualifying child for the EITC, the child must meet the age, residency, relationship, and joint return tests.

The age test for the EITC qualifying child is as follows:

- Under age 19 at the end of the year and younger than the taxpayer (or the taxpayer's spouse, if filing jointly).

- Under age 24 at the end of the year, a full-time student for at least 5 months of the year, and younger than the taxpayer (or the taxpayer's spouse, if filing jointly).

- Any age and permanently and totally disabled at any time during the year.

For example, if the sister-in-law is under 19 years old and single, she can be claimed as a qualifying child. If she is married, she cannot be claimed as a qualifying child unless she files a joint return only to claim a refund of withholding or estimated tax paid.

Federal Law vs State Civil Rights: Who Wins?

You may want to see also

Explore related products

![]()

Residency test

To be a qualifying child for the Earned Income Tax Credit (EITC), the child must meet the relationship, age, residency, and joint return tests.

The residency test requires that the qualifying child must have lived with the taxpayer in the United States for more than half of the tax year. The United States includes the 50 states, the District of Columbia, and U.S. military bases, but it does not include U.S. possessions such as Guam, the Virgin Islands, or Puerto Rico.

If the child was born or died during the year for which the taxpayer claims the EITC, the child is considered to have lived with the taxpayer for more than half of the year if the taxpayer's home was the child's main home for more than half of the time the child was alive during that year. Temporary absences, such as a child being away from home, are counted as time lived with the taxpayer.

If the child meets the residency test and all other requirements but is claimed as a qualifying child by multiple taxpayers, tiebreaker rules are applied to determine which taxpayer can claim the child. The custodial parent, or the parent with whom the child lived for the greater number of nights during the year, is generally given priority. If the child spent an equal number of nights with each parent, the custodial parent is the parent with the higher adjusted gross income.

Martial Law: Can Cities Take This Step?

You may want to see also

![]()

Joint return test

To be a qualifying child for the Earned Income Tax Credit (EITC), the child must not have filed a joint return with another person. The only exception to this is if they are filing a joint return to claim a refund of taxes withheld or estimated taxes paid. In this case, there must be no tax liability if separate returns were filed.

A qualifying child must meet the relationship, age, residency, and joint return tests. The age test states that the child must be under the age of 19 at the end of the year and younger than the taxpayer (or the taxpayer's spouse, if filing jointly). If the child is a full-time student, they can be under the age of 24 at the end of the year and still meet the age test. The child must be younger than the taxpayer (or the taxpayer's spouse, if filing jointly).

The residency test requires that the child lives with the taxpayer in the United States for more than half of the tax year. If the child was born or died during the year, and the taxpayer's home was the child's main home for more than half of the time they were alive, this also meets the residency test. Temporary absences are also included in this test.

If the qualifying child is married, they cannot be claimed as a qualifying child if they filed a joint return for the year, unless the joint return was only to claim a refund of withholding or estimated tax paid.

Minors' Corruption: Megan's Law Implications

You may want to see also

![]()

Qualifying child rules

To be a qualifying child for the Earned Income Tax Credit (EITC), the child must be your son, daughter, stepchild, foster child, or a descendant of any of them. This also includes adopted children who are lawfully placed with you for legal adoption. Additionally, the child could be your brother, sister, half-sibling, step-sibling, or a descendant of any of them.

The child must be under the age of 19 at the end of the year and younger than you (or your spouse, if filing jointly). Or, the child is under the age of 24 at the end of the year, a full-time student for at least five months of the year, and younger than you (or your spouse). The child can also be of any age and permanently and totally disabled at any time during the year.

The child must live in the same home as you in the United States for more than half of the tax year. This includes the 50 states, the District of Columbia, and U.S. military bases, but not U.S. possessions such as Guam, the Virgin Islands, or Puerto Rico. Temporary absences, such as a child being born or dying during the year, or a kidnapped child, are counted as time lived with you.

The child must not have filed a joint return with another person unless it was only to claim a refund of taxes withheld or estimated taxes paid, and there is no tax liability if separate returns were filed. If the child was married at the end of the tax year, they generally cannot be your qualifying child if they filed a joint return unless it was only to claim a refund.

To claim the EITC, you, your spouse (if filing jointly), and the qualifying child must have a valid Social Security Number (SSN).

Federal Inmates: Law Library Volunteering Opportunities?

You may want to see also

Frequently asked questions

Yes, a sister-in-law can be a qualifying child for EITC as long as she meets the relationship, age, residency, and joint return tests.

The relationship test requires that the qualifying child be related to the taxpayer by blood, marriage, or adoption.

The age test requires that the qualifying child be under the age of 19 at the end of the year and younger than the taxpayer (or the taxpayer's spouse, if filing jointly).

The residency test requires that the qualifying child live with the taxpayer in the United States for more than half of the tax year.

The joint return test states that the qualifying child cannot file a joint tax return with another person unless it is only to claim a refund of taxes withheld or estimated taxes paid.