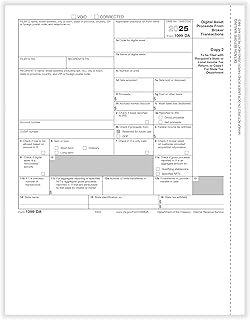

The question of whether law offices receive 1099 forms is a common one, particularly for attorneys and legal professionals who engage independent contractors or vendors. According to IRS regulations, law offices, like any other business, are required to issue 1099 forms to certain payees, such as independent contractors, who receive $600 or more in a tax year. This includes payments made for legal services, expert witness fees, or other professional services provided by non-employees. However, law offices themselves typically do not receive 1099s unless they are operating as independent contractors for another entity, which is less common. Instead, they are more likely to be the issuers of 1099 forms, ensuring compliance with tax reporting obligations. Understanding these requirements is crucial for law offices to avoid penalties and maintain proper financial records.

| Characteristics | Values |

|---|---|

| Applicability | Law offices may receive 1099s if they meet certain IRS criteria, such as receiving payments for services from clients or vendors. |

| Threshold | Payments totaling $600 or more in a calendar year from a single payer typically require a 1099-NEC (Nonemployee Compensation) to be issued to the law office. |

| Type of 1099 | 1099-NEC is the primary form used for reporting payments to law offices for services rendered as independent contractors. |

| Exemptions | Payments made to corporations (excluding medical or legal corporations) are generally exempt from 1099 reporting. |

| Reporting Requirements | Payers must file 1099-NEC forms with the IRS and provide copies to law offices by January 31st following the tax year. |

| Consequences of Non-Compliance | Failure to issue 1099s when required can result in penalties for the payer, ranging from $50 to $550 per form, depending on the delay. |

| Recipient Responsibility | Law offices receiving 1099s must report the income on their tax returns, typically on Schedule C (Form 1040) or as part of their business income. |

| Record-Keeping | Both payers and law offices should retain records of transactions and 1099s for at least four years for IRS audit purposes. |

| Electronic Filing | Payers can file 1099s electronically with the IRS, which is often faster and more efficient than paper filing. |

| State Requirements | Some states have additional 1099 filing requirements, so law offices and payers should check state-specific rules. |

Explore related products

What You'll Learn

![]()

1099 Requirements for Lawyers

Lawyers and law firms must navigate specific IRS rules regarding 1099 reporting, particularly when engaging independent contractors or vendors. The threshold is clear: if a law office pays an individual or unincorporated business $600 or more in a calendar year for services, a 1099-NEC must be issued. This includes payments to court reporters, expert witnesses, or freelance paralegals. Failure to comply can result in penalties ranging from $50 to $550 per missing form, depending on the delay in filing.

Consider a scenario where a law firm hires a graphic designer to create trial exhibits for $700. Since the designer is an independent contractor and the payment exceeds $600, the firm is obligated to issue a 1099-NEC. However, if the same firm pays a corporation for similar services, no 1099 is required unless the payment is for legal or medical services, in which case a 1099-MISC is necessary. This distinction highlights the importance of classifying payees correctly and tracking payments meticulously.

To ensure compliance, law offices should implement a systematic approach. First, maintain a vendor database with W-9 forms on file for all contractors. Second, categorize payments by type (e.g., legal fees, non-employee compensation) to determine the appropriate 1099 form. Third, use accounting software with 1099 tracking features to automate reporting. Finally, submit 1099s to the IRS and recipients by January 31st annually, with extensions available under specific conditions.

A common pitfall is assuming that payments for legal services are exempt from 1099 reporting. While attorney fees paid to another law firm or individual attorney are generally excluded, payments to non-attorney service providers (e.g., process servers) are not. Another misconception is that small payments can be ignored. Even if a contractor is paid $500 in one year and $200 the next, the cumulative total of $700 triggers the 1099 requirement in the second year.

In conclusion, understanding 1099 requirements is essential for law offices to avoid penalties and maintain compliance. By accurately classifying payees, tracking payments, and adhering to deadlines, firms can streamline reporting and focus on their core legal work. Proactive measures, such as regular audits of vendor payments, can further mitigate risks and ensure adherence to IRS regulations.

Navigating Local Sword Sales: Finding Sellers and Understanding Legal Laws

You may want to see also

Explore related products

![]()

Independent Contractors vs. Employees

Law offices, like any business, must navigate the complexities of classifying workers as either independent contractors or employees, a decision that directly impacts whether they issue 1099 forms. Misclassification can lead to significant legal and financial penalties, making this distinction critical. The IRS uses a multi-factor test to determine worker status, focusing on behavioral control, financial control, and the relationship between the parties. For law firms, this often means scrutinizing how attorneys or support staff are managed, paid, and integrated into the firm’s operations.

Consider a scenario where a law office hires a freelance legal researcher. If the researcher works on their own schedule, uses their own tools, and is paid per project without benefits, they are likely an independent contractor, and the firm would issue them a 1099-NEC. Conversely, a paralegal who works set hours, uses firm resources, and receives a regular salary with benefits would be classified as an employee, requiring a W-2 instead. The key lies in the degree of control the law office exerts over how the work is performed.

From a practical standpoint, law firms should implement clear contracts and policies to avoid ambiguity. For independent contractors, agreements should explicitly state the scope of work, payment terms, and the contractor’s autonomy. For employees, job descriptions, benefit packages, and tax withholdings must align with legal requirements. Regular audits of worker classifications can help firms stay compliant, especially as roles evolve over time.

The stakes are high: misclassifying an employee as an independent contractor can result in back taxes, penalties, and legal fees. For instance, if a law office fails to withhold taxes for a misclassified worker, the IRS may impose fines of up to 40% of the unpaid taxes. Additionally, misclassified workers may sue for denied benefits like overtime or health insurance. Proactive measures, such as consulting with an employment attorney or using IRS Form SS-8 for clarification, can save firms from costly disputes.

Ultimately, the decision to issue a 1099 hinges on accurate worker classification. Law offices must balance operational needs with legal obligations, ensuring that their practices align with IRS guidelines. By understanding the nuances between independent contractors and employees, firms can protect themselves while maintaining flexibility in their workforce. This diligence not only ensures compliance but also fosters trust with workers and regulatory bodies alike.

Understanding Open Meeting Law Training: Compliance Essentials for Public Officials

You may want to see also

Explore related products

![]()

Reporting Legal Fees on 1099s

Law offices, like other businesses, must navigate the complexities of tax reporting, particularly when it comes to 1099 forms. A critical aspect of this is understanding when and how to report legal fees on 1099s. The IRS requires businesses to issue a 1099-NEC (Nonemployee Compensation) to any independent contractor or law firm paid $600 or more during the tax year for services rendered. This includes legal fees paid to attorneys or law firms operating as independent contractors, not as employees. For instance, if a corporation hires a law firm to handle a contract dispute and pays them $10,000, the corporation must issue a 1099-NEC to the law firm.

The distinction between employee and independent contractor is crucial. Legal fees paid to an attorney who is an employee of the law firm, rather than an independent contractor, do not require a 1099. Instead, these payments are reported on a W-2 form. Misclassifying workers can lead to penalties, so it’s essential to verify the relationship. For example, if a solo practitioner operates as an independent contractor, they would receive a 1099-NEC, whereas an associate attorney on payroll would receive a W-2.

Reporting legal fees on a 1099-NEC involves specific steps. First, ensure the law firm or attorney provides a completed W-9 form, which includes their Taxpayer Identification Number (TIN). Second, track all payments made to the law firm throughout the year. Third, file the 1099-NEC with the IRS and provide a copy to the law firm by January 31st of the following year. Failure to file or late filing can result in penalties ranging from $50 to $580 per form, depending on the delay. For instance, a business filing 1099s late by 30 days could face penalties of $60 per form, up to a maximum of $206,000.

One common misconception is that legal fees paid to law firms are exempt from 1099 reporting. This is false. The IRS does not differentiate between types of services when it comes to 1099-NEC requirements. Whether the legal fees are for litigation, consultation, or drafting documents, if the threshold of $600 is met, reporting is mandatory. For example, a small business that pays a law firm $750 for drafting a partnership agreement must issue a 1099-NEC.

Finally, law offices themselves may receive 1099s if they operate as independent contractors for clients. For instance, a solo practitioner who provides legal services to multiple businesses would receive a 1099-NEC from each client paying $600 or more. This underscores the importance of maintaining accurate records and understanding both sides of the reporting equation. By adhering to IRS guidelines, businesses and law offices can avoid penalties and ensure compliance with tax laws.

Is Traffic Court Legally Charged? Understanding the Law and Your Rights

You may want to see also

Explore related products

![]()

Tax Obligations for Law Firms

Law firms, like any other business, have specific tax obligations that extend beyond the typical corporate tax return. One critical aspect often overlooked is the requirement to issue 1099 forms to certain vendors and contractors. For instance, if a law firm pays an independent contractor, such as a legal researcher or a court reporter, more than $600 in a tax year, the firm must file a 1099-NEC (Nonemployee Compensation) form with the IRS and provide a copy to the contractor. This ensures compliance with federal tax laws and helps prevent underreporting of income by recipients.

The process of issuing 1099s involves meticulous record-keeping. Law firms must maintain detailed records of payments made to independent contractors throughout the year. This includes tracking the contractor’s name, address, taxpayer identification number (TIN), and the total amount paid. Failure to collect a contractor’s TIN can result in penalties of up to $280 per instance, emphasizing the importance of due diligence. Additionally, law firms should be aware of the January 31st deadline for providing 1099-NEC forms to contractors and the February 28th (or March 31st if filing electronically) deadline for submitting copies to the IRS.

A common pitfall for law firms is misclassifying employees as independent contractors to avoid payroll taxes. The IRS scrutinizes such arrangements closely, and misclassification can lead to significant penalties, back taxes, and legal liabilities. To avoid this, firms should assess the degree of control they exercise over the worker and the independence of the worker’s business. For example, if a paralegal works regular hours, uses firm resources, and is supervised by an attorney, they are likely an employee, not an independent contractor.

Beyond 1099 obligations, law firms must also consider state-specific tax requirements. Some states mandate additional forms or have lower thresholds for reporting contractor payments. For instance, California requires a 1099-MISC for payments over $600, while Vermont’s threshold is just $100. Firms operating in multiple states must navigate these variations carefully to avoid noncompliance. Consulting a tax professional or using specialized software can streamline this process and reduce the risk of errors.

Finally, law firms should proactively educate their staff about tax obligations to ensure seamless compliance. This includes training bookkeepers and administrative staff on the proper classification of workers, the importance of timely 1099 filings, and the consequences of noncompliance. By integrating these practices into their operational workflow, firms can minimize tax-related risks and focus on their core mission: serving clients effectively.

Understanding the Authority to Enforce Laws: The Power to Execute

You may want to see also

Explore related products

![]()

Common 1099 Mistakes to Avoid

Law offices, like many businesses, often engage independent contractors, making them responsible for issuing 1099 forms. However, the process is riddled with potential pitfalls that can lead to penalties and legal complications. One common mistake is failing to correctly identify whether a worker is an independent contractor or an employee. Misclassification can result in hefty fines from the IRS, as employees require W-2 forms, not 1099s. To avoid this, law offices should carefully review the IRS’s 20-factor test, which examines the degree of control over the worker and the independence of their business operations.

Another frequent error is neglecting to collect a completed W-9 form from contractors before payments are made. Without this form, law offices risk issuing incorrect taxpayer identification numbers, leading to bounced 1099s and potential penalties. It’s crucial to request a W-9 at the start of the contractor relationship and verify the information for accuracy. Additionally, law offices should ensure they have a system in place to track payments to contractors, as any individual or entity paid $600 or more during the tax year must receive a 1099-NEC form.

Timing is also critical. Missing the 1099 filing deadlines can result in penalties ranging from $50 to $280 per form, depending on how late they are filed. Law offices must provide contractors with Copy B of the 1099-NEC by January 31 and file Copy A with the IRS by the end of February (or March 31 if filing electronically). Creating a calendar reminder system can help ensure compliance. Moreover, failing to file electronically when required (for 250 or more forms) can lead to additional penalties, so law offices should familiarize themselves with IRS e-filing requirements.

Lastly, law offices often overlook the importance of double-checking data accuracy before submitting 1099s. Errors in names, addresses, or taxpayer identification numbers can cause delays and require corrective filings. Implementing a review process, such as cross-referencing W-9 forms and payment records, can minimize mistakes. By proactively addressing these common pitfalls, law offices can streamline their 1099 reporting process and avoid unnecessary complications with the IRS.

Barack and Michelle Obama: Law Licenses and the Truth

You may want to see also

Frequently asked questions

Yes, law offices may receive 1099s if they have received payments that meet IRS reporting requirements, such as income from clients exceeding $600 in a tax year.

Payments to law offices for legal services, consulting, or other professional fees exceeding $600 in a year typically require a 1099-NEC (Nonemployee Compensation).

Yes, law offices must issue 1099-NEC forms to any independent contractors or vendors paid $600 or more during the tax year for services rendered.

No, law offices are not exempt and must comply with IRS 1099 reporting rules for both receiving and issuing 1099s, just like any other business.