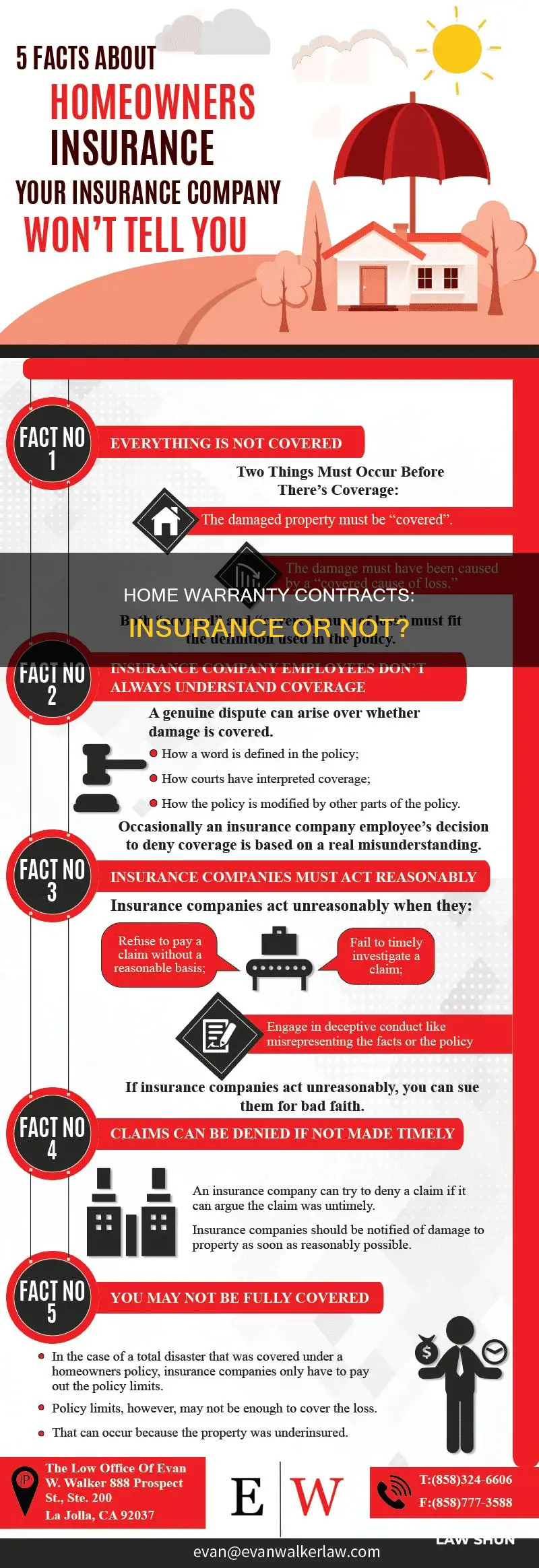

Home warranty and homeowners insurance are two different concepts that provide varying degrees of protection for homeowners. While a home warranty is a contract between a homeowner and a home protection company, promising to repair or replace parts of a home system or appliances, it is not an insurance policy. Home warranties are service contracts that cover general wear and tear, deterioration, or defects that existed when the home was purchased or leased. On the other hand, homeowners insurance covers damage to property and liability for injuries to guests, protecting against unexpected events that lead to damage. Homeowners insurance is often required by lenders, whereas home warranties are optional and may be purchased in addition to insurance for added peace of mind. Understanding the differences between the two is crucial for homeowners to make informed decisions about their protection needs.

| Characteristics | Values |

|---|---|

| Home warranty | A service contract that covers repairs or replacements of home systems and appliances due to general wear and tear. |

| Home insurance | A policy that covers financial losses due to damage or destruction of the home or its contents by "covered perils" such as fire, theft, or natural disasters. |

| Relationship to law | Home warranties are regulated and licensed by the California Department of Insurance, but they are not insurance policies and do not replace the need for home insurance. |

| Exclusions | Home warranties do not cover pre-existing issues, misuse, or neglect. They also have specific exclusions and limitations listed in the contract. |

| Cost | Home warranties typically cost a few hundred dollars per year, while home insurance costs vary based on coverage and risks. |

| Necessity | Home insurance is typically required by lenders, while home warranties are optional but can provide additional peace of mind. |

Explore related products

What You'll Learn

![]()

Home warranties are not insurance policies

Home warranties are not a substitute for homeowners' insurance policies. While home warranties cover repairs and replacements of specific items, they do not provide the same level of protection as insurance. Home warranties often have exclusions and limitations, and the coverage varies depending on the plan chosen. For example, a warranty might cover plumbing repairs but exclude certain types of leaks or plumbing stoppages. It is important to carefully read the contract and understand the exclusions, conditions, and limitations before purchasing a home warranty.

Additionally, home warranties differ from insurance policies in how they pay for repairs or replacements. Home warranties may have limits on the amount they will pay, and if the cost of a repair exceeds this limit, the homeowner may have to pay the difference. Home warranty companies may also deny claims for various reasons, such as unauthorised work performed on a covered item or modifications made to a system or appliance.

In terms of regulation, home warranty companies are licensed and regulated by the California Department of Insurance, and consumers can file complaints with the department if they have issues with their home warranty company. However, it is important to note that home warranty companies are not held to the same standards as insurance companies, and there may be differences in how claims and disputes are handled.

Furthermore, home warranties and insurance policies serve different purposes. Home warranties are designed to cover the cost of repairing or replacing specific items in the home, such as appliances or home systems, whereas insurance policies provide financial protection against a range of risks, including damage to the property itself. While a home warranty may help with the cost of maintaining and repairing certain items, it does not provide comprehensive protection for the home in the same way that insurance does.

Leadership Laws: 10 Irrefutable Rules for Effective Guidance

You may want to see also

Explore related products

![]()

Home warranties are service contracts

Home warranties are contracts between a homeowner and a home warranty or protection company. These contracts promise to repair or replace parts of a home system or certain appliances due to wear and tear, deterioration, or defects that existed when the home was purchased or leased.

The specific appliances and systems covered by a home warranty vary depending on the contract. For example, a basic plan might cover heating, AC, plumbing, and electrical systems, while a more comprehensive plan might include kitchen and laundry appliances, roof leak repairs, and unlimited AC refrigerant.

Home warranties typically have a deductible, and there may be certain costs not covered, such as permits or hauling away equipment. It is important to carefully read the contract before purchasing a plan, as home warranties always have exclusions to coverage.

In California, home warranties are regulated and licensed by the Department of Insurance, and consumers can investigate a company's license and track record before purchasing a warranty.

The Law of Conservation of Energy: Who Was the Founder?

You may want to see also

Explore related products

![]()

Home warranties cover wear and tear, not accidents

Home warranties are not insurance policies, but service contracts between a homeowner and a home protection company. They cover the repair or replacement of parts of a home system or certain appliances due to "normal" wear and tear, deterioration, or defects that existed when the home was bought or leased.

Wear and tear refer to the deterioration of systems and appliances from everyday use or ageing. Home warranties cover systems and appliances that become inoperable due to normal wear and use, including rust, corrosion, and chemical or sediment buildup. However, they do not cover accidents or abnormal events, such as a child's toy clogging the toilet drain.

Home warranties are regulated and licensed by the California Department of Insurance, and consumers can file complaints and seek assistance if their claims are unfairly denied. It is important to carefully review the terms, limitations, and exclusions of a home warranty contract before purchasing it to understand what is covered and what falls outside the scope of the warranty.

While home warranties cover repairs and replacements due to wear and tear, they do not cover all associated costs. For example, they may not cover permits or the hauling away of equipment. Additionally, there are often caps and limits on the amount paid for replacements, and homeowners may have to pay the difference if the cost exceeds the limit stated in the contract.

In summary, home warranty contracts are not insurance policies, and they specifically cover wear and tear, deterioration, or existing defects, but not accidents or abnormal events. It is essential to carefully review the terms and exclusions of a home warranty contract to understand the specific coverage provided.

Thermodynamics Laws: Interdependence or Independence?

You may want to see also

Explore related products

![]()

Home warranties are optional, unlike insurance

Home warranties are not a replacement for homeowners insurance, and they differ in what they cover and how they pay for repairs or replacements. Warranties often have exclusions and limitations, and it is essential to read the contract carefully before purchasing to understand what is covered and what is not. For example, a warranty might cover air conditioning systems but exclude certain parts, or cover plumbing repairs but not pay to clear all plumbing stoppages or repair certain types of leaks.

Home warranties are regulated and licensed by the California Department of Insurance, and consumers can investigate a company's license and track record before purchasing a warranty. While home warranties can provide peace of mind and help with home maintenance costs, they are not required by law or most lenders, and the choice to purchase one is up to the homeowner.

Homeowners insurance is crucial for overall protection, while a home warranty can provide additional coverage for specific home components. Depending on individual needs, having both can provide comprehensive security. However, it is important to understand the differences between the two and how they can work together to protect your home and its contents.

DUI Laws: A Historical Perspective

You may want to see also

Explore related products

![]()

Home warranties are regulated by the Department of Insurance

Home warranties are regulated on a state-by-state basis in the United States. While they are not considered insurance policies, some states include home warranties under the authority of their insurance departments. For example, California's Department of Insurance oversees home warranty regulation and places strict requirements on home warranty companies. The department regulates everything, from the contracts these companies can offer to how claims are handled. It even requires company names to be approved before they can operate.

In Texas, the Texas Real Estate Commission is in charge of home warranties, while New York handles these contracts under the Department of Financial Services. Some states, like South Dakota, do not specifically regulate home warranties but do regulate other service contract types, such as automobile service contracts. Additionally, the Federal Trade Commission (FTC) plays a crucial role in ensuring that businesses, including home warranty companies, adhere to regulations. They mandate that contracts are transparent and easy to understand.

Home warranty companies are regulated and licensed by the Department of Insurance in each state to protect consumers. These departments investigate consumer complaints and enforce insurance laws, as some companies have tried to sell warranties illegally without a license. Consumers can contact these departments to inquire about a company's license status and review consumer complaints. It is recommended that individuals understand the exclusions, conditions, and limitations of a home warranty contract before purchasing one.

While home warranties and home insurance policies share some similarities, such as paying a monthly premium for coverage, they differ in their offerings. Home insurance covers home damage due to fire, natural disasters, storms, or theft, while home warranties cover the appliances and systems inside the home from normal wear and tear. Home warranties are not a replacement for home insurance and have their own exclusions and limitations.

America's Anti-Gay Marriage Law: A Historical Perspective

You may want to see also

Frequently asked questions

No. A home warranty is a service contract that covers general wear and tear, deterioration, or defects that existed when you bought or leased your home. It is not a supplement for homeowners insurance. Homeowners insurance, on the other hand, covers damage to your property and liability for injury to guests that occurs on your property.

A home warranty covers most major appliances and systems in your house. This includes items like washers, dryers, ovens, refrigerators, plumbing, electrical, and HVAC systems. However, it's important to read the contract carefully as certain components of a covered item may be excluded from coverage.

It is recommended to have both a home warranty and homeowners insurance as they provide different types of protection. Homeowners insurance covers unexpected events that lead to damage, while home warranties cover expected events such as the aging and breakdown of appliances and systems. Additionally, home warranties can be transferred from one owner to the next, unlike insurance policies.

![Problems in Contract Law: Cases and Materials [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/71KVwHbBZ1L._AC_UY218_.jpg)