Benford's Law is a widely used tool for detecting anomalies in financial data that may indicate fraud. It is based on the concept that the distribution of leading digits in a dataset should follow a specific pattern, with each subsequent digit having a diminishing probability of being the leading digit. By comparing the leading digits of financial data, such as ledger entries or income statements, to the expected distribution, accountants and auditors can identify potential fraud. Benford's Law is particularly useful because fabricating a set of falsified data that conforms to the law is challenging, and it can be applied to various data types, including general ledgers, trial balance reports, and income statements. However, it is important to note that Benford's Law has limitations and should be complemented with other analytical procedures and auditing processes to effectively detect financial statement fraud.

| Characteristics | Values |

|---|---|

| Use in accounting | Benford's Law is widely used in accounting to examine data for anomalies that may indicate fraud. |

| Use in forensic accounting | Forensic accountants, fraud examiners, accountants, and auditors use Benford's Law to detect anomalies that require investigation. |

| Use in fraud detection | Benford's Law can be used to detect fraud in financial statements, as it is difficult to fabricate a set of falsified data that conforms to the law. |

| Use in risk evaluation | Benford's Law can help investors evaluate risk by examining the annual report data of a company. |

| Use in network activity analysis | Benford's Law can be used to detect irregular network activity and other data that may indicate malicious insider activity. |

| Use in academic research | Benford's Law has been used in academic research to study the predictability of fraudulent financial statements and detect fraudulent banking practices. |

| Limitations | Benford's Law cannot predict financial statement fraud or categorize fraudulent and non-fraudulent companies. |

| Data requirements | Accountancy data generally follows four assumptions required for a valid conclusion on a Benford curve: general ledgers, income statements, and inventory listings. |

| Data analysis | Accountants compare the leading digits of financial transaction data to a Benford curve to spot anomalies. |

Explore related products

What You'll Learn

![]()

The use of Excel and Benford's Law to detect fraud

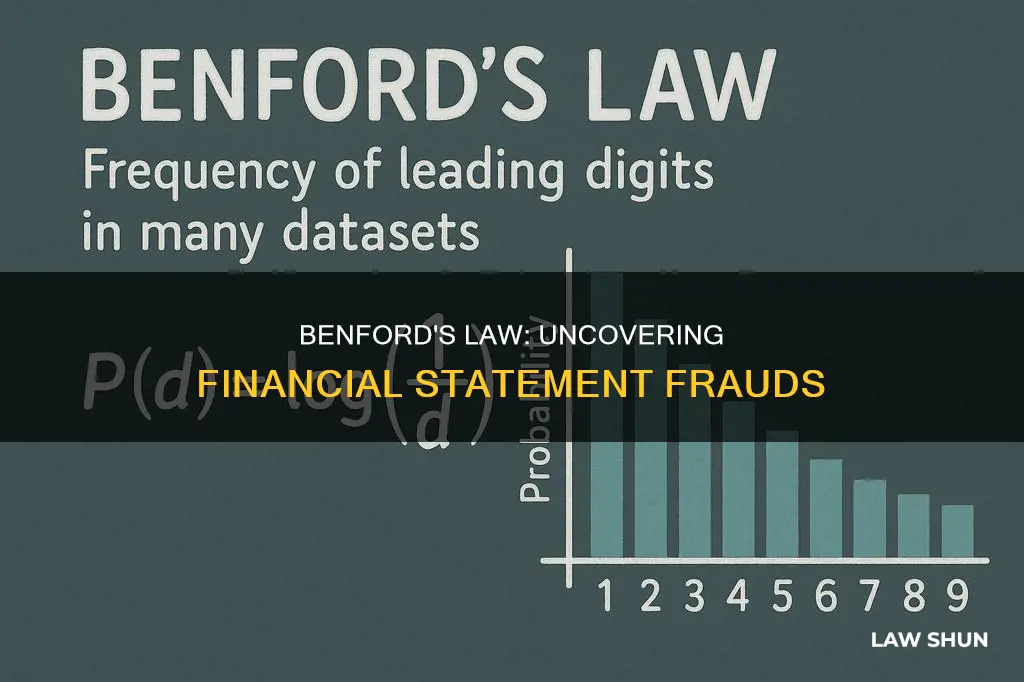

Benford's Law, based on base-10 logarithms, states that in a genuine data set of numbers, the numeral 1 will be the leading digit around 30% of the time, the numeral 2 will be the leading digit around 18% of the time, and so on, with each subsequent numeral from 3 to 9 decreasing in frequency. This law was first observed by astronomer Simon Newcomb in 1881, who noticed that the page numbers in a book of logarithm tables were more worn towards the front of the book and less worn towards the end, indicating that the earlier pages, containing numbers beginning with 1 as the first digit, were consulted more frequently.

Benford's Law can be a useful tool for detecting fraud in financial statements and accounting practices. When individuals manipulate numbers to commit fraud, they tend to use more 8s and 9s as the first digit, deviating from the expected distribution set forth by Benford's Law. By applying Benford's Law analysis to financial data, auditors and accountants can identify unusual transactions or potential fraud.

Excel-based procedures have been developed to assist in this process. Using Microsoft Excel, CPAs can count the leading digits in a data set, create a chart of the findings, and compare the results to the expected distribution of Benford's Law, often referred to as the Benford curve. This method can be applied to various types of data, including general ledgers, income statements, balance sheets, and expense reports.

For example, in 2013, Papa Nikolaou & Grammatikos used Benford's law to detect fraudulent banking practices, uncovering distortions in financial information in banks' financial statements. Additionally, Hanselman and colleagues claimed that a company's annual report data followed Benford's law, providing investors with a tool to evaluate risk.

However, it is important to note that Benford's Law has its limitations. Some researchers have questioned its effectiveness in certain contexts, such as detecting election fraud. Furthermore, Gava and Vitiello's study in 2014 suggested that Benford's Law may not be suitable for identifying deviations in financial statements, as it has zero prediction accuracy for categorizing fraudulent and non-fraudulent companies.

In conclusion, while Benford's Law and Excel-based analyses can be valuable tools for detecting fraud, they should be used in conjunction with other analytical procedures and auditing processes to ensure comprehensive fraud detection and prevention.

Who Can Enforce Civilian Law? The National Guard's Role

You may want to see also

Explore related products

![]()

How Benford's Law can be used to detect anomalies

Benford's Law is a useful tool for detecting anomalies in financial statement data that may indicate fraud. The law is based on the concept that in a large and random set of natural numbers, the distribution percentage for each digit is not equal. For example, in a dataset of numbers that fit Benford's assumptions, the digit 1 is expected to be the most common leading digit, while 9 is expected to be the least common.

Accountants and auditors can use Benford's Law to compare the leading digits of financial data, such as ledger entries, to a Benford curve or distribution. This comparison helps spot anomalies that may indicate fraud. For instance, if the distribution percentages deviate significantly from the expected distribution, it could suggest artificial manipulation of the data.

Benford's Law can be applied to various financial statements, including general ledgers, income statements, balance sheets, and inventory listings. By analysing the leading digits and their distribution, accountants can identify potential red flags that warrant further investigation.

Additionally, Benford's Law can be used to detect irregular network activity and potential malicious insider activity. This involves examining network traffic data and applying the same principles of analysing leading digits and their distribution.

However, it is important to note that Benford's Law has limitations. Some studies suggest that it cannot predict financial statement fraud or categorise fraudulent and non-fraudulent companies accurately. Therefore, it should be used in conjunction with other analytical procedures and fraud detection methods to ensure comprehensive fraud risk assessment.

Whistleblower Laws: Protection for Non-Employees?

You may want to see also

Explore related products

![]()

Predicting financial statement fraud risk using Benford's Law

Benford's Law is a useful tool for predicting financial statement fraud risk and detecting anomalies in data that may indicate fraud. The law is based on the concept that in a large and random set of natural numbers, the distribution percentage for each digit is not equal. For example, in a dataset that fits Benford's assumptions, the digit '1' is expected to be the most common leading digit, while ''9' is expected to be the least common.

Accountants and auditors can use Benford's Law to compare the leading digits of financial data, such as ledger entries, to a Benford curve or distribution to identify potential fraud. This technique can also be applied to other types of data, such as network traffic, to detect malicious insider activity. The wide acceptance of Benford's Law in the forensic accounting community and the availability of experts in this field further contribute to its admissibility in fraud detection.

While Benford's Law is a valuable tool, it is important to note that it has limitations and should be used in conjunction with other analytical procedures. Standard analytical procedures, such as comparing financial ratios and auditing processes, remain essential in detecting fraud. Additionally, as Benford's Law gains popularity, fraudsters may become more aware of it and find ways to create falsified data that conforms to the law, making it more challenging to detect fraud.

To address these challenges, auditors and fraud examiners can utilise Excel-based Benford's Law analyses to enhance their fraud detection capabilities. By counting the leading digits in a data set and charting the findings, they can compare the results to the expected distribution set by Benford's Law. This method can be applied to various types of financial data, including general ledgers, income statements, and balance sheets.

In conclusion, Benford's Law is a powerful tool for predicting financial statement fraud risk and detecting anomalies. However, it should be used in conjunction with other analytical procedures to ensure the effectiveness and accuracy of fraud detection and prevention. The ongoing development of new methods and procedures is crucial in staying ahead of fraudsters and protecting investors and organisations from financial crimes.

Impeachment and Lawmaking: Can a President Still Legislate?

You may want to see also

Explore related products

![]()

The effectiveness of Benford's Law in predicting fraud

Benford's Law is based on the observation that in many naturally occurring datasets, the frequency of numbers beginning with a certain digit follows a specific distribution. This distribution, known as the Benford distribution, has been found to occur in various natural phenomena, including the lengths of rivers, populations of cities, and front-page headlines in The New York Times. This distribution is depicted as a curve, often referred to as the Benford curve, which closely resembles a steep water slide.

The law states that the probability of a number beginning with a particular digit is proportional to the number itself. For example, numbers starting with the digit "1" are more common than those starting with "2", and so on. This distribution is not valid for randomly generated numbers but applies to many datasets found in nature and human activity, including financial data.

To use Benford's Law for fraud detection, auditors can compare the distribution of leading digits in a company's financial data with the expected Benford distribution. Significant deviations from the expected distribution may indicate potential fraud or data manipulation. For example, a bookkeeper writing fictitious checks below a certain threshold might result in the numbers "4" and "9" occurring more frequently as leading digits than predicted by Benford's Law.

However, critics argue that Benford's Law has limitations and cannot be solely relied upon for fraud detection. It is claimed that Benford's Law cannot predict financial statement fraud risk or categorize companies with and without fraud risk. Additionally, the law should not be considered definitive, as it cannot decidedly prove the absence or presence of fraud. Other factors, such as built-in bias toward certain numerals, can also affect the distribution of leading digits and lead to false positives or negatives.

In conclusion, while Benford's Law provides a useful tool for auditors and fraud investigators, it should be used in conjunction with other analytical procedures and fraud detection methods. The effectiveness of Benford's Law in predicting fraud may depend on the specific context and nature of the data being analyzed, and further studies are needed to evaluate its applicability in different scenarios.

How Laws Are Made: Creating, Altering, and Repealing

You may want to see also

Explore related products

![]()

How Benford's Law can be used to detect irregular network activity

Benford's Law, also known as the Newcomb-Benford Law, the law of anomalous numbers, or the first-digit law, is an observation that in many real-life sets of numerical data, the leading digit is likely to be small. In naturally occurring systems, the frequency of numbers' first digits is not evenly distributed. Numbers beginning with 1 occur about 30% of the time, while 9 appears as the leading digit less than 5% of the time. This law tends to be most accurate when values are distributed across multiple orders of magnitude, especially if the process generating the numbers follows a power law, which is common in nature.

Benford's Law can be applied to detect irregular network activity. Measures of network traffic generally follow a Benford curve. An unexpected increase in a co-founder's normal network activity, for example, can shift the distribution of leading digits in the company's network traffic, signalling an abnormality. Benford's Law is especially useful in detecting Denial-of-Service (DoS) attacks because flooding a network with data breaks the naturalness of network traffic.

Benford's Law has been applied to online social networks, with studies showing that the distribution of first significant digits (FSD) of friend and follower counts on Facebook, Twitter, Google Plus, Pinterest, and LiveJournal follows Benford's Law. A preliminary analysis of over 20,000 Twitter accounts showed that the 100 users whose egocentric networks deviated most strongly from the Benford's Law distribution were all engaged in suspicious activity. This indicates the possibility of using Benford's Law to detect malicious or irregular behaviour on social media.

Benford's Law can also be used to detect anomalous packets in legitimate traffic. The Interactive Data Extraction and Analysis with Newcombe-Benford power law can detect the first occurrences of leading digits in each packet, indicating the usage of automated scripts for attack purposes.

Claiming Father-in-Law as Dependent: Tax Implications

You may want to see also

Frequently asked questions

Benford's Law states that if you take the first digit of any large and random set of natural numbers, the distribution percentage for each digit will not be equal.

Accountants often compare the leading digits of financial transaction data to a Benford curve to spot anomalies that may indicate fraud.

One example is if the distribution of the first digit of transactions is heavily skewed towards digits 8 and 9, which could indicate that people are trying to circumvent the need to report transactions above a certain amount.

Benford's Law cannot predict financial statement fraud or categorise fraudulent and non-fraudulent companies. It also cannot complement the analysis of financial ratios and auditing processes as a means of predicting financial statement fraud.

Other methods include using ratios or relationships and comparing those results to expected ratio results or industry averages. Positive confirmations can also be used to verify vendor and customer balances.