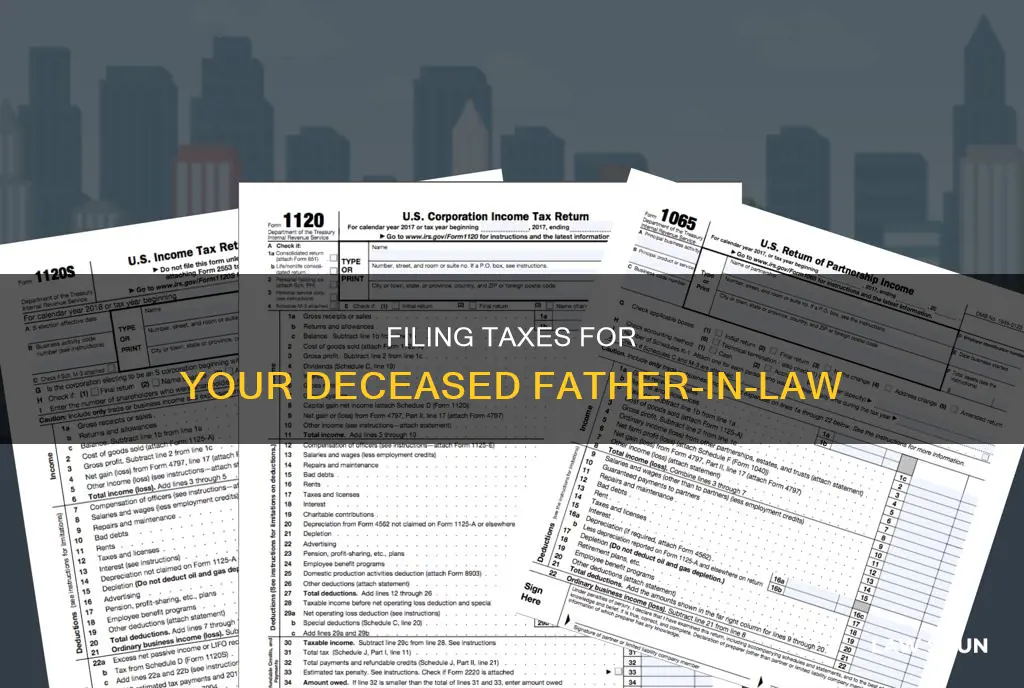

If you are the spouse or personal representative of your deceased father-in-law, you are responsible for filing their final individual income tax return and estate tax return. This includes federal income tax returns that would have been required for the year of their death, including all income up to the date of death and any eligible credits and deductions. You may need to file Form 1040 or 1040-SR, U.S. Individual Tax Return, and Form 1310, Statement of a Person Claiming Refund Due a Deceased Taxpayer, to claim any refunds. It is recommended to consult a tax professional or the IRS for detailed guidance on your specific situation.

| Characteristics | Values |

|---|---|

| Who files the tax return? | The surviving spouse or representative of the deceased files the final tax return. |

| What is included in the tax return? | All income up to the date of death, credits, and deductions. |

| What forms are required? | Form 1040 or 1040-SR, Form 1310 (if claiming a refund), Form 4506-T (to verify non-filing status and certain income documents). |

| When is the final return due? | By the regular April tax date, unless an extension is granted. |

| What if there is a balance due? | The filer is responsible for paying any balance and can submit payment with the return or explore other payment options on the IRS website. |

| What if there is a refund due? | The surviving spouse or representative can claim the refund by submitting Form 1310. |

| What if there is no surviving spouse or representative? | A personal representative, typically the executor of the will or court-appointed individual, is responsible for filing the final return. |

| What if there are beneficiaries and/or complex estate matters? | It is recommended to consult a local paid tax professional or CPA for guidance. |

| Where can I find more information? | IRS Publication 559, "Survivors, Executors, and Administrators," provides detailed guidance on managing a deceased person's tax affairs. |

Explore related products

What You'll Learn

- The executor of the will or a court-appointed representative must file the final tax return

- The final tax return must include all income up to the date of death

- If there is a surviving spouse, they may be able to file as a qualifying widow/widower

- If there is a refund due, Form 1310 must be completed

- If there is a tax balance due, it must be paid or a payment plan agreed

![]()

The executor of the will or a court-appointed representative must file the final tax return

When someone passes away, their surviving spouse or a representative is responsible for filing their final tax return. This representative is usually named in the person's will or appointed by a court. In the absence of a surviving spouse or appointed representative, a personal representative will file the final return. The personal representative can be an executor, administrator, or anyone else who oversees the decedent's property.

If you are the executor of your deceased father-in-law's will or a court-appointed representative, you are responsible for filing their final tax return. This may include having to recreate their income records for that year, including any rental income. You can request all income reported to the IRS under your father-in-law's name and Social Security number by creating an online account as his personal representative. You may also need the assistance of a paid tax professional to sort out the income received before and after his death.

It is important to note that death does not relieve one's obligation to file a final federal income tax return. The final tax return should include all income up to the date of death, as well as any credits and deductions. If the deceased had not filed individual income tax returns for prior years, you may need to file those as well. It is your responsibility to pay any balance due and to submit a claim if a refund is owed.

To file the final tax return, you can use Form 1040, U.S. Individual Tax Return, or Form 1040-SR, U.S. Tax Return for Seniors. If you are claiming a refund, you will also need to complete and submit Form 1310, Statement of a Person Claiming Refund Due a Deceased Taxpayer. The final return is typically due by the regular April tax date, unless an extension has been granted.

Corporate Bylaws: Can They Be Broken?

You may want to see also

Explore related products

![]()

The final tax return must include all income up to the date of death

When a person passes away, their surviving spouse or representative is responsible for filing their final tax return. This task usually falls to the executor or administrator of the estate, but if neither is named, then the task needs to be taken over by a survivor of the deceased. The IRS considers a person married for the entire year that their husband or wife died if they do not remarry during that year. The surviving spouse is eligible to use filing status married filing jointly or married filing separately.

If the deceased had not filed individual income tax returns for the years prior to their death, you may have to file these. It is your responsibility to pay any balance due and to submit a claim if there is a refund due. If a refund is due on the individual income tax return of the deceased, claim the refund by submitting Form 1310, Statement of a Person Claiming Refund Due a Deceased Taxpayer. Form 1310 is not required for surviving spouses or court-appointed representatives.

UK Law: Can Women Legally Rape Men?

You may want to see also

Explore related products

![]()

If there is a surviving spouse, they may be able to file as a qualifying widow/widower

When a person dies, their surviving spouse or representative is responsible for filing the deceased person's final tax return. The IRS considers someone married for the entire year in which their spouse died, unless they remarry during that year.

The surviving spouse can file a joint return for the year of their spouse's death. They can also file as a Qualifying Widow/Widower (Qualifying Surviving Spouse) for the two years following their spouse's death. This status allows them to use the same tax brackets and deductions as those for married filing jointly, which can provide financial relief to those who lose their spouse and may be struggling with death-related expenses or household bills.

To qualify for the Qualifying Surviving Spouse status, the surviving spouse must meet the following requirements:

- They qualified for Married Filing Jointly with their spouse for the year their spouse died (it doesn't matter if they actually filed as Married Filing Jointly).

- They did not remarry.

- They have a child, stepchild, or adopted child who qualifies as their dependent for the year, or would qualify as their dependent except that the child does not meet the gross income or joint return test, or except that the surviving spouse may be claimed as a dependent of another taxpayer.

- They paid more than half the cost of maintaining their home, which must be the main home of their dependent child for the entire year, except for temporary absences.

It is important to note that the Qualifying Surviving Spouse status cannot be claimed for the year of the spouse's death, and there are no additional tax breaks specifically for widows or widowers. However, using this filing status means that the standard deduction will be double that of a Single filer status.

Martial Law: Air Travel Restrictions and Your Rights

You may want to see also

Explore related products

![[5 Pack] Estate Sale Signs Set - 16 x 12 Inch Double-Sided Yard Signs With Arrows and Metal H Stakes - Property Sale Directional Signs - Weather-Proof](https://m.media-amazon.com/images/I/71vlCeOw-UL._AC_UY218_.jpg)

![]()

If there is a refund due, Form 1310 must be completed

If your deceased father-in-law is due a tax refund, you will need to complete Form 1310, 'Statement of Person Claiming Refund Due a Deceased Taxpayer', to notify the IRS and ensure the refund is sent to the correct beneficiary. Form 1310 is a one-page form that must be completed and mailed to the IRS, it cannot be e-filed.

Form 1310 is usually filed by the surviving spouse, another beneficiary, or a court-appointed representative of the deceased's estate. If there is no will, a probate court will name an executor, who is then responsible for Form 1310. Surviving spouses and court-appointed representatives do not need to complete this form.

The form is filed as an attachment to the standard Form 1040 tax return, which must be prepared on behalf of the beneficiaries. The executor may also need to file Form 1041, but only if the estate generates more than $600 in annual income. If Form 1041 is required, the IRS will issue the refund to the estate rather than an individual.

It is important to note that Form 1310 is not the only form that needs to be filed. The deceased's final individual income tax return must also be filed, reporting all income up to the date of death, as well as any eligible credits and deductions. This return can be filed using Form 1040, U.S. Individual Tax Return, or 1040-SR, U.S. Tax Return for Seniors.

If you have any questions or concerns about filing taxes for your deceased father-in-law, it is recommended to seek professional advice from a tax specialist or attorney.

Common-Law Partners: Can They Transfer Funds?

You may want to see also

Explore related products

![The Estate [DVD]](https://m.media-amazon.com/images/I/71hfjtYRRrL._AC_UY218_.jpg)

![]()

If there is a tax balance due, it must be paid or a payment plan agreed

When it comes to filing a deceased person's final tax return, their surviving spouse or representative is responsible for filing the return. This is done in the same way as if the deceased were still alive, reporting all income up to the date of death, as well as any eligible credits and deductions.

- Short-term Payment Plans: The IRS offers short-term payment plans, providing up to 180 days to settle tax debts. Interest and penalties will continue to accrue during this period, with a failure-to-pay penalty of 0.5% per month.

- Long-term Payment Plans: For those who need more time, long-term payment plans are available, typically allowing up to 72 months to pay off the debt. These plans may involve a setup fee, and the monthly payment amount must be sufficient to clear the debt within this timeframe.

- Guaranteed Installment Agreements: Individuals owing $10,000 or less in taxes may qualify for a Guaranteed Installment Agreement. This option requires timely filing and payment compliance over the past five years and agreement to pay the full amount within three years.

- Simple Payment Plans: Most individual taxpayers qualify for a Simple Payment Plan if their total balance of tax, penalties, and interest owed is $50,000 or less. The proposed payment amount must cover the tax liability in full by the Collection Statute Expiration Date, typically within 10 years.

- Direct Debit Installment Agreements: Low-income taxpayers who agree to make electronic debit payments through a Direct Debit Installment Agreement (DDIA) can have the user fee waived.

- Financial Hardship Options: If you can prove financial hardship, you may qualify for "currently not collectible status" and avoid payment until your circumstances improve.

It is important to note that penalties and interest charges may apply if you cannot pay your tax debt in full by the original due date. Therefore, it is in your best interest to pay as much as you can as soon as possible to minimize these additional charges. Additionally, ensure that you understand the terms of your payment plan to avoid defaulting on your agreement.

Tracing Cell Phones: Can Law Enforcement Track Your Device?

You may want to see also

Frequently asked questions

The IRS requires a personal representative to file the final tax return of a deceased person. This representative can be the surviving spouse, an executor, administrator, or anyone else who oversees the decedent's property. If there is no personal representative, a court-appointed representative will file the final return.

You will need to file Form 1040, U.S. Individual Tax Return or 1040-SR, U.S. Tax Return for Seniors. You may also need to file Form 1310, Statement of a Person Claiming Refund Due a Deceased Taxpayer, if you are claiming a refund on behalf of your deceased father-in-law.

To claim a refund, you will need to submit Form 1310, Statement of a Person Claiming Refund Due a Deceased Taxpayer. Surviving spouses and court-appointed representatives are not required to complete this form.