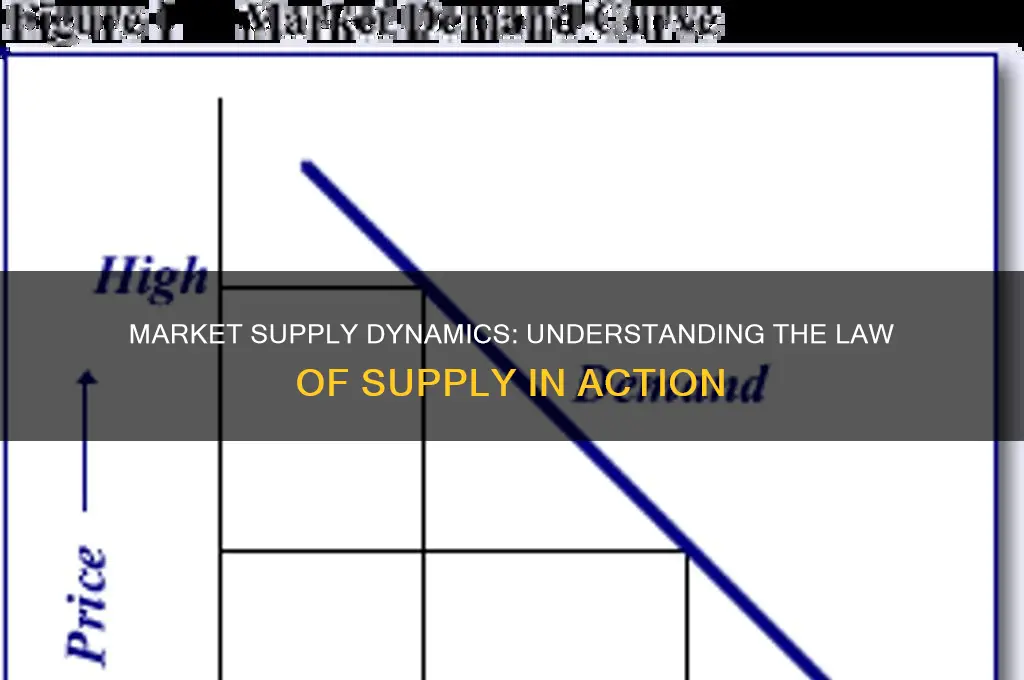

The market supply reflects the law of supply, which states that, all else being equal, as the price of a good or service increases, the quantity supplied by producers also increases, and vice versa. This relationship is driven by the profit motive: higher prices incentivize businesses to produce and sell more, as they can earn greater revenues and profits. Conversely, lower prices reduce the incentive to supply, leading to a decrease in the quantity offered. This dynamic is evident in supply curves, which slope upward, illustrating the direct correlation between price and quantity supplied. Factors such as production costs, technology, and the number of suppliers also influence market supply, but the core principle remains: suppliers respond to price changes by adjusting their output accordingly, ensuring that the law of supply holds as a fundamental concept in economics.

| Characteristics | Values |

|---|---|

| Direct Relationship | Market supply increases as prices rise, reflecting the law of supply. |

| Producer Incentives | Higher prices incentivize producers to supply more goods/services. |

| Production Costs | Lower production costs enable higher supply at existing price levels. |

| Technology Advancements | Improved technology reduces costs, increasing supply at all price levels. |

| Number of Sellers | More sellers in the market lead to higher overall market supply. |

| Expectations of Future Prices | If future prices are expected to rise, current supply may decrease. |

| Government Policies | Subsidies or tax cuts can increase supply, while regulations may reduce it. |

| Supply Curve Slope | The supply curve slopes upward, illustrating the positive price-supply link. |

| Market Equilibrium | Supply adjusts to meet demand at the equilibrium price. |

| Elasticity of Supply | Supply responsiveness to price changes varies across industries. |

| Time Frame | Short-term supply is less flexible compared to long-term supply. |

| Resource Availability | Increased availability of raw materials boosts supply. |

| Seasonality | Supply fluctuates based on seasonal factors (e.g., agriculture). |

| Global Market Conditions | International trade and exchange rates impact domestic supply. |

| Consumer Trends | Shifts in consumer preferences can influence production and supply. |

Explore related products

What You'll Learn

![]()

Price and Quantity Supplied Relationship

The relationship between price and quantity supplied is a cornerstone of the law of supply, illustrating how producers respond to changes in market conditions. As prices rise, firms are incentivized to increase production to maximize profits, assuming all other factors remain constant. This direct correlation is evident across industries, from agriculture to manufacturing. For instance, when coffee prices surge due to increased demand, farmers allocate more land and resources to coffee cultivation, boosting the overall supply. Conversely, a price drop often leads to reduced production, as seen in the oil industry during periods of oversupply, where drilling activity declines to cut costs.

Analyzing this relationship requires understanding the concept of the supply curve, which slopes upward to reflect the positive association between price and quantity supplied. Each point on the curve represents a specific price-quantity combination that firms are willing and able to supply. However, this relationship is not linear; it is influenced by factors like production capacity, input costs, and technological advancements. For example, a tech company might increase smartphone production in response to higher prices, but only up to the limit of its assembly line capacity. Beyond this point, further increases in supply would require costly investments in new machinery, altering the curve’s slope.

To leverage this relationship effectively, businesses must monitor market prices and adjust production strategies accordingly. A practical tip for small-scale producers is to use price thresholds as triggers for scaling operations. For instance, a bakery might increase bread production by 20% when prices rise above $3 per loaf, ensuring they capitalize on higher margins without overextending resources. Similarly, large corporations can employ dynamic pricing models to predict how changes in supply will impact profitability, allowing for more informed decision-making.

A comparative analysis highlights how this relationship varies across industries. In the pharmaceutical sector, where production involves high fixed costs and lengthy timelines, the response to price changes is often delayed. Conversely, in the retail industry, where production cycles are shorter, firms can quickly adjust supply to match price fluctuations. This disparity underscores the importance of industry-specific considerations when applying the law of supply. For instance, a clothing manufacturer can ramp up production within weeks in response to higher prices, while a pharmaceutical company might take years to increase output due to regulatory approvals and production complexities.

In conclusion, the price and quantity supplied relationship is a dynamic and industry-specific phenomenon that reflects the law of supply in action. By understanding this relationship, businesses can optimize production strategies, respond to market changes, and enhance profitability. Whether through threshold-based scaling, dynamic pricing models, or industry-specific adjustments, mastering this concept is essential for navigating the complexities of modern markets.

Navigating Holiday Gatherings with Your Ex-Daughter-in-Law: Tips for Harmony

You may want to see also

Explore related products

![]()

Producer Incentives and Profitability

Producers are the backbone of market supply, and their decisions are fundamentally driven by incentives and profitability. The law of supply dictates that as prices rise, producers are incentivized to supply more goods or services to maximize profits. This relationship is not merely theoretical; it’s observable in industries ranging from agriculture to technology. For instance, when coffee prices surge due to a poor harvest in Brazil, farmers in Vietnam increase their production to capitalize on higher revenues. This direct response to price signals illustrates how producer incentives align with the law of supply, ensuring markets adjust to changing conditions.

To understand this dynamic, consider the marginal cost and marginal revenue framework. Producers will continue to supply additional units as long as the marginal revenue exceeds the marginal cost. For example, a smartphone manufacturer might produce 10,000 units at a price of $500 each, but if the price rises to $600, they’ll expand production to 15,000 units because the additional revenue outweighs the incremental production costs. This decision-making process is universal across industries, from small-scale artisans to multinational corporations. The key takeaway is that profitability acts as the primary lever influencing supply decisions.

However, producer incentives are not solely driven by price. External factors such as government subsidies, technological advancements, and input costs also play a critical role. For instance, renewable energy producers are often incentivized by tax credits and grants, which lower their effective production costs and encourage greater supply. Conversely, rising oil prices can increase the cost of raw materials for manufacturers, reducing their profitability and, consequently, their willingness to supply. Producers must constantly weigh these factors to determine the optimal level of production, ensuring their actions remain aligned with both market signals and external influences.

A practical tip for producers is to monitor market trends and adapt strategies accordingly. For example, a clothing manufacturer might invest in automation to reduce labor costs when wages rise, maintaining profitability even as production scales up. Similarly, farmers can hedge against volatile commodity prices by using futures contracts, ensuring stable revenues regardless of market fluctuations. By proactively managing costs and leveraging incentives, producers can maximize their responsiveness to the law of supply, securing long-term viability in competitive markets.

In conclusion, producer incentives and profitability are the linchpins of market supply, driving the direct relationship outlined by the law of supply. By balancing price signals with external factors and adopting strategic cost-management practices, producers can effectively navigate market dynamics. This not only ensures their own success but also contributes to the stability and efficiency of the broader economy. Understanding these mechanisms empowers producers to make informed decisions, fostering a supply system that reflects both individual and collective interests.

Is Desecrating the American Flag Legal? Exploring Free Speech Limits

You may want to see also

Explore related products

![]()

Production Costs Impact on Supply

Production costs are the backbone of supply dynamics, dictating how much of a good or service producers are willing to offer at various price points. When input costs—such as raw materials, labor, or energy—rise, the cost of production increases, squeezing profit margins. For instance, a surge in oil prices directly impacts industries reliant on petroleum-based products, like plastics or transportation. As costs climb, producers may reduce output or raise prices to maintain profitability, illustrating the inverse relationship between production costs and supply. This phenomenon is a cornerstone of the law of supply, where higher costs lead to a decrease in the quantity supplied at a given price.

Consider the agricultural sector, where production costs are highly sensitive to weather conditions and commodity prices. A drought can skyrocket the cost of water, while a spike in fertilizer prices can strain farmers’ budgets. If the cost of producing wheat increases by 20%, farmers may cut back on planting or shift to more profitable crops. This reduction in supply, assuming demand remains constant, would drive up wheat prices in the market. Conversely, advancements in technology or economies of scale can lower production costs, encouraging producers to increase supply. For example, the adoption of precision farming techniques has reduced waste and lowered costs, allowing farmers to expand output without raising prices.

To mitigate the impact of rising production costs, businesses often employ strategies such as vertical integration or hedging. Vertical integration, where a company owns multiple stages of production, can reduce dependency on external suppliers and stabilize costs. Hedging, on the other hand, involves using financial instruments to lock in prices for raw materials, protecting against volatility. Small businesses, however, may lack the resources for such strategies, making them more vulnerable to cost fluctuations. For instance, a local bakery facing higher flour prices might absorb the cost, reduce portion sizes, or pass the increase to consumers, each decision influencing the supply of baked goods.

The interplay between production costs and supply is not just theoretical—it has real-world implications for consumers and policymakers. During the 2021 global supply chain crisis, shipping costs soared, and port congestion delayed deliveries, driving up production costs across industries. Automakers, for example, faced semiconductor shortages, forcing them to halt production lines and reduce vehicle supply. This scarcity led to higher car prices, demonstrating how production cost shocks ripple through markets. Policymakers must therefore monitor cost trends to anticipate supply disruptions and implement measures like subsidies or tax breaks to stabilize production.

In conclusion, production costs are a critical determinant of market supply, shaping the quantity of goods and services available at any price. Whether through technological innovation, strategic business practices, or external shocks, changes in production costs directly influence supply decisions. Understanding this relationship allows businesses, consumers, and policymakers to navigate market fluctuations more effectively. By focusing on cost management and adaptability, producers can maintain supply stability even in the face of rising expenses, ensuring that markets function efficiently and meet demand.

Statute Law in the UK: Understanding the Basics

You may want to see also

Explore related products

![Law School Stickers Decals[100Pack], Vinyl Law School Stickers Lawyer Stickers Decals for Laptop Water Bottle Bumper Luggage Computer Skateboard Snowboard. Gift for Kids Girls Teens](https://m.media-amazon.com/images/I/81oB4JStWeL._AC_UY218_.jpg)

![]()

Technological Advancements and Efficiency

Technological advancements have revolutionized the way businesses operate, directly influencing market supply and reinforcing the law of supply. Consider the smartphone industry: the introduction of automated assembly lines reduced production time by 30%, allowing manufacturers to increase output significantly. This efficiency gain lowered costs, enabling suppliers to offer more units at each price point, a classic illustration of the law of supply in action. As technology continues to evolve, its impact on production efficiency becomes a critical determinant of supply elasticity.

To harness the benefits of technological advancements, businesses must strategically invest in innovation. For instance, adopting robotics in manufacturing can reduce labor costs by up to 50% while increasing output by 40%. However, this requires substantial upfront capital and skilled personnel to manage the transition. Small and medium-sized enterprises (SMEs) should start with incremental upgrades, such as implementing IoT sensors to monitor equipment performance, before scaling to full automation. Caution must be exercised to avoid over-reliance on technology, as system failures or cyberattacks can disrupt supply chains.

A comparative analysis of industries reveals that sectors embracing technology experience faster supply growth. Agriculture, for example, has seen a 25% increase in crop yields through precision farming techniques, which use drones and data analytics to optimize resource use. In contrast, industries slow to adopt technology, like traditional textiles, face stagnant or declining supply due to higher costs and inefficiencies. This disparity underscores the competitive advantage of technological integration in enhancing supply responsiveness to market demands.

Persuasively, governments and policymakers play a pivotal role in accelerating technological adoption. Incentives such as tax credits for R&D investments or subsidies for automation equipment can encourage businesses to modernize. For instance, Germany’s Industry 4.0 initiative has spurred a 15% increase in manufacturing efficiency among participating firms. Similarly, public-private partnerships can fund training programs to upskill workers, ensuring they can operate advanced technologies. Without such support, the gap between tech-savvy and traditional industries will widen, distorting market supply dynamics.

In conclusion, technological advancements and efficiency are not just trends but essential drivers of market supply. By reducing costs, increasing output, and enhancing responsiveness, technology amplifies the law of supply. Businesses, governments, and workers must collaborate to navigate this transformation, ensuring that the benefits of innovation are widely distributed. As the pace of technological change accelerates, staying ahead of the curve will be the key to maintaining a competitive edge in the global market.

How to Find the USCIS Office That Granted Your Green Card

You may want to see also

Explore related products

![]()

Market Expectations and Future Supply

Market expectations act as a crystal ball for future supply, shaping producer behavior and industry trajectories. When businesses anticipate rising demand for electric vehicles due to tightening emissions regulations, for instance, they invest in battery production facilities and secure lithium supply chains years in advance. This forward-looking response is a direct manifestation of the law of supply: as expectations of future profitability increase, producers expand capacity to meet anticipated demand. Conversely, gloomy forecasts for a product category, like declining sales of physical books, prompt publishers to reduce print runs and allocate resources to digital publishing instead. These adjustments, driven by market expectations, ensure supply aligns with projected demand, minimizing waste and maximizing efficiency.

Example: The global chip shortage of 2020-2022 highlights the critical role of expectations. Automakers, underestimating the pandemic-driven surge in demand for vehicles, failed to secure sufficient semiconductor orders. This miscalculation, based on outdated expectations, led to production halts and skyrocketing prices, demonstrating the high costs of misaligned supply and demand.

Understanding the link between expectations and supply is crucial for businesses navigating volatile markets. Step 1: Monitor leading indicators like consumer confidence surveys, industry forecasts, and technological trends to gauge future demand. Step 2: Analyze competitor actions – are they expanding production, acquiring new assets, or diversifying product lines? These moves signal their expectations and can inform your own supply decisions. Caution: Avoid overreacting to short-term fluctuations. Distinguish between temporary spikes and sustainable shifts in demand to avoid costly overproduction or missed opportunities.

The law of supply operates not just in the present but also in the realm of anticipation. Comparative Analysis: Consider the contrasting responses of oil producers to peak oil theories. Some, anticipating dwindling reserves and rising prices, invested heavily in exploration and extraction technologies. Others, skeptical of the theory, focused on maximizing short-term profits. The former group positioned themselves to benefit from higher prices, while the latter risked being left behind as the energy landscape evolved. This illustrates how divergent expectations can lead to vastly different supply strategies.

Takeaway: Proactive management of supply based on informed expectations is essential for long-term success.

Finally, government policies and technological advancements can significantly influence market expectations and, consequently, future supply. Descriptive Example: Subsidies for renewable energy technologies create expectations of growing demand for solar panels and wind turbines, prompting manufacturers to expand production capacity. Similarly, breakthroughs in battery technology can shift expectations for electric vehicle adoption, leading to increased investment in charging infrastructure and battery manufacturing. Practical Tip: Stay abreast of policy changes and technological breakthroughs in your industry to anticipate shifts in market expectations and adjust your supply strategy accordingly. By proactively aligning supply with future demand, businesses can capitalize on emerging opportunities and mitigate risks.

Understanding the Law of Demand: A Fundamental Economic Relationship

You may want to see also

Frequently asked questions

The law of supply states that, all else being equal, as the price of a good or service increases, the quantity supplied by producers also increases, and vice versa. Market supply reflects this law by showing the total quantity of a product that all producers are willing and able to supply at various price levels.

According to the law of supply, market supply responds positively to price changes. When prices rise, producers are incentivized to supply more of the product to maximize profits, shifting the supply curve upward. Conversely, when prices fall, producers reduce supply to minimize losses.

The law of supply assumes "all else being equal" (ceteris paribus) to isolate the relationship between price and quantity supplied. In reality, other factors like production costs, technology, and producer expectations can influence supply. Market supply curves may shift due to these factors, but the law of supply still holds as a fundamental principle.

The law of supply dictates that the market supply curve slopes upward, reflecting the direct relationship between price and quantity supplied. As price increases, producers are willing to supply more, creating a positive slope. This curve visually represents the collective behavior of all suppliers in the market adhering to the law of supply.