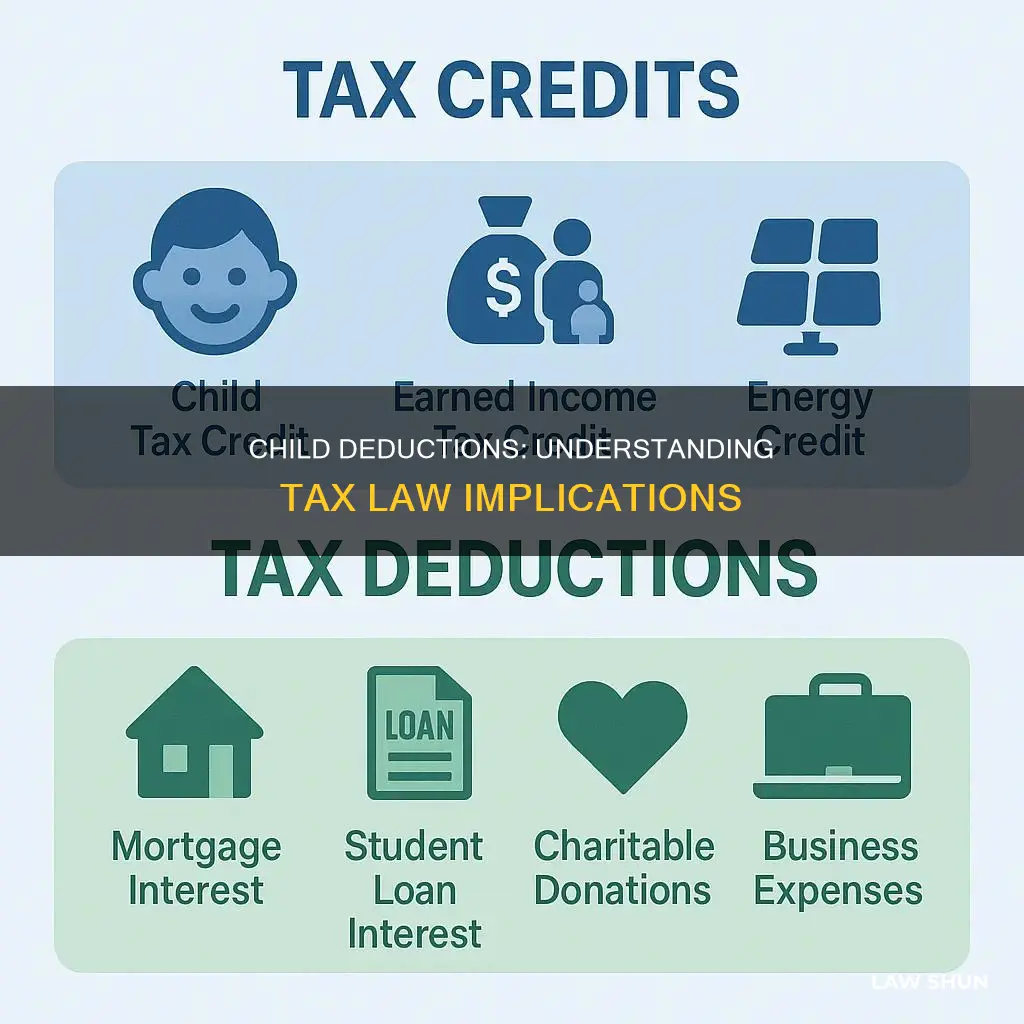

Families with children may be eligible for more tax deductions and credits than taxpayers without children. The Child Tax Credit (CTC) is a tax credit that can be claimed for each qualifying child. The definition of a qualifying child is broad and includes stepchildren, foster children, siblings, grandchildren, nieces, and nephews. For the 2024 tax year, the CTC allows eligible parents to claim a $2,000 credit per child under the age of 17, with income limits set at $200,000 for individuals and $400,000 for married couples. Parents and guardians with higher incomes may still be eligible to claim a partial credit. Additionally, there is no cap on the number of credits that can be claimed in one year. The CTC is just one example of how the tax law can affect child deductions, and there are other tax credits and deductions that families with children may be able to take advantage of.

| Characteristics | Values |

|---|---|

| Tax credit amount per child | $2,000 |

| Maximum age of child | 16 years |

| Maximum refundable amount per child | $1,700 |

| Tax credit amount for other dependents | $500 |

| Income limit for individuals | $200,000 |

| Income limit for married couples | $400,000 |

| Income limit for adoption credit | $252,150 |

| Income limit for reduced adoption credit | $252,151 to $292,150 |

| Standard deduction for head of household | $21,900 |

| Standard deduction for single person | $14,600 |

| Child support taxable | No |

Explore related products

![]()

Child Tax Credit (CTC)

The Child Tax Credit (CTC) is a tax credit available to families with qualifying children that helps them get a tax break. The CTC was increased by the Tax Cuts and Jobs Act (TCJA) from the old $1,000 limit to a $2,000 credit per qualifying child under the age of 17. The credit is available to taxpayers with a Modified Adjusted Gross Income (MAGI) of up to $200,000 for single parents and $400,000 for married couples. Parents and guardians with higher incomes may still be eligible to claim a partial credit.

The Internal Revenue Service (IRS) has a broad definition of a qualifying child for the CTC, which includes stepchildren, foster children, siblings, grandchildren, nieces, and nephews. To be considered a qualifying child, the dependent must meet certain requirements, such as being under 17 at the end of the tax year, not providing more than half of their own financial support, and living with the taxpayer for more than half of the tax year.

The CTC is not just limited to biological children, and there is no cap on the number of credits that can be claimed in one year. This means that families with multiple children or other qualifying dependents can receive a significant tax benefit. For example, a married couple with two young children and an income under the threshold could receive a $4,000 tax credit, significantly reducing their tax bill.

In addition to the CTC, taxpayers can also claim other dependent care credits, such as the Child and Dependent Care Credit, which can help offset the cost of childcare expenses. Furthermore, the American Rescue Plan Act (ARPA) increased the CTC for the 2021 tax year, allowing tax filers to claim up to $3,600 per child under age 6 and up to $3,000 per child between the ages of 6 and 17. This change made the credit fully refundable, allowing low-income families to receive the maximum credit regardless of their earnings.

The CTC is a valuable tool for families to reduce their tax burden and keep more of their hard-earned money. It is important for taxpayers to stay informed about the latest tax laws and eligibility requirements to maximize their tax benefits.

Carter's Legal Legacy: Laws and Impact

You may want to see also

Explore related products

![]()

Qualifying child

The Child Tax Credit (CTC) is a tax credit offered by the Internal Revenue Service (IRS) to families with qualifying children. The CTC provides a credit of up to $2,000 per qualifying child under the age of 17. The credit is available to families with incomes up to $200,000 for individuals and $400,000 for married couples. For the 2024 tax year, the child must be under 17 at the end of the tax year to qualify.

To be considered a qualifying child for the CTC, the child must meet several requirements. Firstly, they must have a valid Social Security Number for employment in the United States. Additionally, they must be the dependent of the taxpayer, and the taxpayer must claim them as a dependent on their tax return. The child should not provide more than half of their own financial support for the tax year, and they should live with the taxpayer for more than half of the tax year.

The definition of a qualifying child for the CTC is broad and includes not only biological children but also stepchildren, eligible foster children, siblings, grandchildren, nieces, and nephews. This allows many families to take advantage of the tax credit and receive financial support for their dependents.

It is important to note that the CTC is subject to change and has been adjusted over the years. For example, in 2021, the American Rescue Plan Act (ARPA) increased the CTC to up to $3,600 per child under age 6 and up to $3,000 per child between the ages of 6 and 17. Additionally, the refundability of the CTC has varied, with a maximum refundable amount of $1,700 per qualifying child in some years.

For families with higher incomes, it is still possible to claim a partial credit. Additionally, for dependents who do not qualify for the CTC, such as children over the age of 16, there may be other tax credits available, such as the Credit for Other Dependents, which offers a credit of up to $500.

The Process of Creating Laws and Bills

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Income limits

The Child Tax Credit (CTC) is a key tax break that provides qualifying households with a credit of up to $2,000 per qualifying child under the age of 17. The credit is worth up to $2,200 per child under 17 for the 2025 tax year. The actual amount received depends on income, age, and other factors.

The CTC has a significant impact on the economic well-being of low-income families with children. Families with children in all income groups benefit from the CTC, but low-income families are most likely to be limited to the refundable portion of the credit. The refundable portion of the CTC is $1,700 for the 2025 tax year.

To qualify for the full amount of the CTC, your modified adjusted gross income (MAGI) must be under $200,000 for individual filers or $400,000 for joint filers. The credit phases out completely for incomes above that threshold. For every $1,000 that your MAGI exceeds the limit, your credit is reduced by $50. For example, a married couple with a MAGI of $415,000 and two qualifying children would qualify for a partial credit of $3,250.

Parents and guardians with higher incomes may be eligible to claim a partial credit. For the 2022 tax year, the credit was capped at $1,500 for low-income families, while the full nonrefundable credit was $2,000. After 2025, the CTC is scheduled to revert to its pre-2021 form, with a credit of up to $1,000 for each child under age 17. This credit will be reduced by 5% of adjusted gross income over $75,000 for individual filers ($110,000 for married couples).

Creating Laws in Micronations: Who Makes the Rules?

You may want to see also

Explore related products

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Child support

The IRS defines a "qualifying child" for the Child Tax Credit (CTC) as a dependent who is under 17 at the end of the tax year, and who does not provide more than half of their own financial support. The child must be the taxpayer's son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, half-sibling, or a descendant of one of these (for example, a grandchild, niece, or nephew). The child must also have lived with the taxpayer for more than half of the tax year and have a valid Social Security Number for employment in the United States.

For the 2024 tax year, the CTC allows eligible parents to claim a $2,000 credit per qualifying child under age 17, with income limits set at $200,000 for individuals and $400,000 for married couples. Single parents may benefit from filing as head of household, which offers a higher standard deduction and lower tax rates.

The CTC is not the only tax benefit available to parents. The Child and Dependent Care Credit can help parents who pay for childcare so that they can work or look for a job. Additionally, the American Opportunity Tax Credit can help parents and students with the expenses of higher education. For families who have adopted children, there is an adoption credit with an income limit of $252,150 for the full amount.

While child support itself does not impact taxes, it is important to note that state child support agencies can intercept federal tax refunds to collect past-due child support payments. Therefore, staying current on child support payments is important for maintaining financial stability and ensuring that any tax refunds due are received in a timely manner.

Obligor in Contract Law: Who is Bound?

You may want to see also

Explore related products

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![]()

Adoption credit

The Adoption Credit is a tax credit available to those who adopt a qualified child. For 2024, the maximum credit amount is $16,810 per child for qualified expenses, and this amount is set to increase to $17,280 per child for adoptions finalized in 2025. Qualified expenses include reasonable and necessary expenses paid to adopt a child, such as agency fees, attorney fees, court costs, and travel expenses. The credit applies to international, domestic, private, or public foster care adoptions.

To be eligible for the Adoption Credit, taxpayers must meet certain income requirements. For 2024, the modified adjusted gross income must be $252,150 or less, with the credit reduced for incomes between $252,151 and $292,150 and unavailable for incomes above $292,150. Additionally, taxpayers must file jointly if married to claim the credit. Furthermore, the credit is non-refundable, meaning taxpayers cannot receive more than they owe in taxes.

If taxpayers receive adoption benefits from their employer, they can exclude up to $16,810 of those benefits from their income for 2024. This exclusion is in addition to the credit, but taxpayers cannot claim both for the same expenses. Taxpayers must claim any allowable exclusion before claiming the credit by completing Part III of Form 8839.

It is important to note that the Adoption Credit only applies to the adoption of a qualified child. A qualified child is typically one who is physically or mentally incapable of self-care and is unlikely to be adopted without assistance. For special needs adoptions, the child must be a U.S. citizen or a qualifying non-citizen. Additionally, taxpayers cannot claim the credit for expenses related to adopting their spouse's child.

The Internal Revenue Service (IRS) has recognized the need to improve its communication and outreach regarding the Adoption Credit. In response to recommendations from the Government Accountability Office (GAO), the IRS agreed to develop a comprehensive educational outreach plan to engage with adoption stakeholders and provide clear and consistent information to taxpayers. This includes working with relevant agencies and improving documentation to help taxpayers understand and claim the credit appropriately.

US-UK Tax Treaty: What's Covered?

You may want to see also

Frequently asked questions

The Child Tax Credit (CTC) is a credit of up to $2,000 per child under the age of 17. The exact amount depends on your income. For the 2024 tax year, the income limit is $200,000 for individuals and $400,000 for married couples.

To be eligible for the Child Tax Credit, your dependent must meet the following criteria: be under 17 at the end of the tax year, be your son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, half-brother, half-sister, or a descendant of one of these; not provide more than half of their own financial support for the tax year, live with you for more than half the tax year, be claimed as a dependent on your return, and not file a joint return for the year.

You can claim the Child Tax Credit by entering your children and other dependents on Form 1040, U.S. Individual Income Tax Return, and attaching a completed Schedule 8812, Credits for Qualifying Children and Other Dependents.

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)