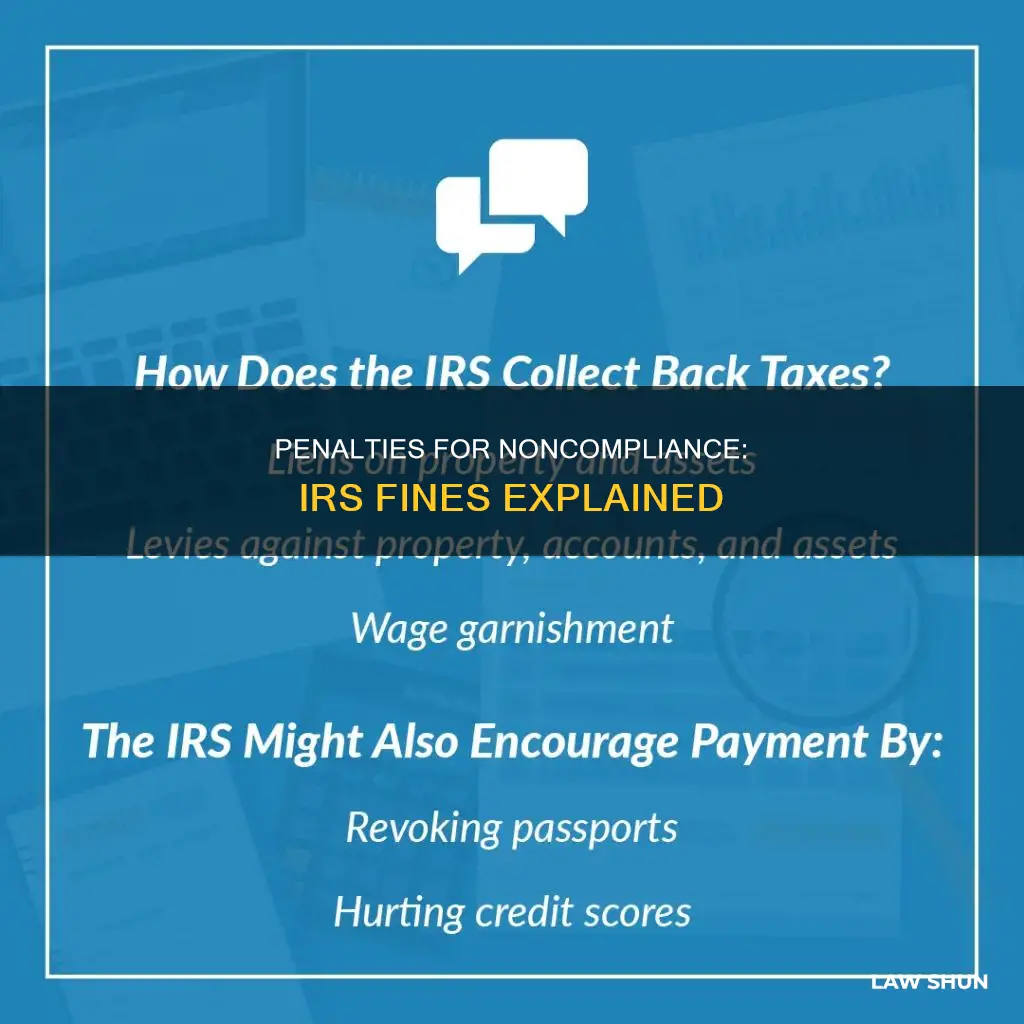

The IRS imposes penalties for noncompliance with tax laws, and these penalties vary in type and amount. The IRS encourages voluntary compliance, meaning taxpayers assess their tax liabilities and pay without external pressure. However, when taxpayers don't meet their tax obligations, the IRS can assess penalties and interest charges. These penalties can be related to failure-to-file, failure-to-pay, accuracy, erroneous refund claims, and more. The IRS also provides avenues for penalty relief, such as demonstrating reasonable cause or good faith. In some cases, the IRS may reduce or waive penalties under specific circumstances. It's important for taxpayers to understand their obligations, remain compliant, and promptly address any noncompliance issues to minimize financial consequences.

| Characteristics | Values |

|---|---|

| Failure to pay by the due date | One-half of one percent for each month, or part of a month, up to a maximum of 25% of the amount of unpaid tax |

| Failure to pay 10 days after the IRS issues a notice of intent to levy property | One percent of the unpaid tax |

| Failure to file on time | Five percent of the tax owed for each month, or part of a month, up to a maximum of 25% |

| Minimum penalty | Applicable if the return is over 60 days late |

| Payment plan | Applicable if you can't pay the full amount of your taxes or penalty on time; may reduce future penalties |

| Interest on penalties | Charged by the IRS; increases the amount owed until the balance is paid in full |

| Accuracy-related penalty | 20% of the underpayment of tax; applies to negligence or disregard of rules or regulations, or substantial understatement of tax |

| Substantial understatement of tax | Exceeds the lesser of 10% of the tax required to be shown on the tax return (or, if greater, $10,000), or $10,000,000 |

| Underpayment of estimated tax | Applicable to individuals, estates, and trusts that don't pay enough estimated tax on their income or pay it late; can be waived due to casualty, local disaster, or other unusual circumstances |

| Penalty relief | Applicable if you acted in good faith and can show reasonable cause for noncompliance; the IRS may abate penalties for filing and paying late if reasonable cause is shown |

Explore related products

What You'll Learn

![]()

Failure to pay

The IRS may charge a penalty for failure to pay the tax you owe by the due date. This is separate from the failure-to-file penalty, which is for failing to file your tax return on time. The failure-to-pay penalty is one-half of one percent for each month, or part of a month, up to a maximum of 25% of the amount of tax that remains unpaid from the due date of the return until the tax is paid in full. This rate increases to one percent if the tax remains unpaid 10 days after the IRS issues a notice of intent to levy property.

If you file your return by its due date and request an installment agreement, the one-half of one percent rate decreases to one-quarter of one percent for any month in which an installment agreement is in effect. Setting up an IRS payment plan can therefore help to reduce the failure-to-pay penalty. If you can't pay the full amount of your taxes or penalty on time, pay what you can now and apply for a payment plan. You may reduce future penalties when you set up a payment plan.

If you owe a failure-to-pay penalty, you may be eligible for penalty relief under First Time Abate. If you are not eligible for this, the IRS may still abate your penalties for filing and paying late if you can show reasonable cause and that the failure wasn't due to willful neglect. Making a good faith payment as soon as possible may help to establish that your initial failure to pay on time was due to reasonable cause and not willful neglect. If you receive a penalty charge and you have reasonable cause for abatement, send your explanation along with the bill to your service center, or call the IRS for assistance.

The IRS does not generally abate interest charges, which continue to accrue until all assessed tax, penalties, and interest are fully paid. Interest accrues on any unpaid tax from the due date of the return (without any extensions) until the date of payment in full. The interest rate is determined quarterly and is the federal short-term rate plus 3%. Interest compounds daily.

In some cases, the penalty for underpayment of estimated tax may be removed or reduced if the underpayment is the result of a casualty, local disaster, or other unusual circumstance when it would not be fair to impose the penalty. If you think you qualify for a waiver of the penalty, send your written explanation, signed under penalty of perjury, to the address at the top of your notice.

Sunshine vs Sunset Laws: What's the Difference?

You may want to see also

Explore related products

![]()

Accuracy-related penalties

The Internal Revenue Service (IRS) may apply an accuracy-related penalty if a taxpayer underpays their taxes and this underpayment is related to one of the following triggers: negligence, disregard for rules or regulations, or substantial understatement of income tax liabilities. Negligence refers to the failure to follow tax regulations that any ordinary taxpayer would. This includes actions such as not keeping accurate or adequate books and tax records, or failing to accurately substantiate items on a tax return. Disregard means carelessly, recklessly, or intentionally ignoring tax rules or regulations. This may include actions such as not including income on a tax return that was shown on an information return. A substantial understatement of tax exists if a taxpayer underpays their tax liability by 10% of the tax required to be shown on their tax return or $5,000.

The accuracy-related penalty is 20% of the portion of the underpayment of tax that is attributable to negligence, disregard of rules or regulations, or substantial understatement of income tax. The IRS may impose a penalty charge higher than 20% in some cases. Interest is charged on penalties, increasing the amount owed until the balance is paid in full. The date from which interest is charged varies depending on the type of penalty.

To obtain IRS penalty reduction for an accuracy-related penalty, the taxpayer must demonstrate that they acted in good faith. The abatement process can be complex and nuanced, so it is generally advised that taxpayers seek professional tax help. If a taxpayer can attribute their underpayment to a reasonable cause, an accuracy-related penalty cannot be applied. Reasonable causes may include a casualty, local disaster, or other unusual circumstances.

First Step Act: Law or Empty Promise?

You may want to see also

Explore related products

$17.99

![]()

Underpayment of estimated tax

The IRS imposes an underpayment penalty on taxpayers who do not pay all of their estimated income taxes for the year or pay their taxes late. This is because taxes are pay-as-you-go, meaning that you need to pay most of your tax during the year as you receive income, rather than paying at the end of the year. The penalty for underpayment of estimated tax applies to individuals, estates, and trusts that don't pay enough estimated tax on their income or pay it late.

The IRS calculates the underpayment penalty by calculating the amount based on the taxes accrued (total tax minus tax credits) on your original tax return or a more recent one you filed. The penalty for underpayment of estimated tax is not a static percentage or flat dollar amount. Interest increases the amount you owe until you pay your balance in full. The failure-to-pay penalty is one-half of one percent for each month or part of a month, up to a maximum of 25%, of the amount of tax that remains unpaid from the due date of the return until the tax is paid in full. This one-half of one percent rate increases to one percent if the tax remains unpaid 10 days after the IRS issues a notice of intent to levy property. On the other hand, if you file your return by its due date and request an installment agreement, the one-half of one percent rate decreases to one-quarter of one percent for any month in which an installment agreement is in effect.

There are certain exceptions to the penalty for underpayment of estimated tax. You may qualify for an exception if you don't have a liability for the prior year, you're a U.S. citizen or a resident alien for the entire year, and your prior tax year covered 12 months. You may also qualify for a waiver of the penalty if you had a reasonable cause for not making the payment, the underpayment was not due to willful neglect, and you experienced an unforeseen, uncommon, or noteworthy event, such as a casualty or disaster. Additionally, the IRS may reduce a penalty if you or your spouse retired in the past two years after reaching age 62 or became disabled and you had reasonable cause to underpay or pay your estimated tax late.

To avoid the underpayment penalty for estimated taxes, you can pay at least 90% of the tax on your current-year return or 100% of the tax shown on the prior year's return. Another way to avoid the penalty is to adjust your withholdings on your W-4 if you have an employer. Reducing your number of dependents or adding an extra withholding amount can help ensure that enough tax is withheld from your paycheck to cover your tax bill. You can use the IRS withholding estimator to check whether you're on track. If you're an independent contractor who pays quarterly estimated taxes, stay on top of each quarter's due date and make sure you're accurately calculating and paying what you owe.

Understanding Contract Law: Damages and Their Purpose

You may want to see also

Explore related products

![Un jour sans fin - Edition collector [Import belge]](https://m.media-amazon.com/images/I/419cMGyjWnL._AC_UY218_.jpg)

![]()

Non-filing penalties

The non-filing penalty is calculated as 5% of the tax due (excluding any tax paid on time and available credits) for each month or partial month that the return is late, up to a maximum of 25%. If the return is delayed by more than 60 days, a minimum penalty is applied, which is either the amount listed or 100% of the underpayment, whichever is less. This penalty is charged for up to 12 months.

It is important to note that the failure-to-file penalty is separate from the failure-to-pay penalty. If both penalties apply, the failure-to-file penalty is reduced by the amount of the failure-to-pay penalty (0.5% for each month). After five months, the failure-to-file penalty reaches its maximum, but the failure-to-pay penalty continues to accrue.

In certain situations, taxpayers may be eligible for penalty relief or abatement. The IRS provides relief for first-time offenders under the First Time Abate program. Additionally, if taxpayers can demonstrate reasonable cause and that the failure was not due to willful neglect, the IRS may reduce or waive the penalty. Examples of reasonable cause include casualty, local disaster, or other unusual circumstances that make it unfair to impose the penalty. Taxpayers can submit a written explanation, signed under penalty of perjury, to request penalty relief.

Congress: How Laws Are Made

You may want to see also

Explore related products

![Fin [Explicit]](https://m.media-amazon.com/images/I/813rUPtJE8L._AC_UY218_.jpg)

![Sans Fin [DVD - MK2]](https://m.media-amazon.com/images/I/81Ub3iEZCCL._AC_UY218_.jpg)

![]()

Tax preparer penalties

The IRS imposes tax preparer penalties on attorneys, certified public accountants, enrolled agents, or anyone who gets paid to prepare tax returns if they don't follow tax laws, rules, and regulations. The IRS will mail a notice or letter if you owe a penalty and will charge monthly interest until the full amount is paid.

Penalty Scenarios

- Understatement due to unreasonable positions — IRC § 6694(a): This applies to tax preparers who understate taxpayers' liabilities on tax returns by taking unreasonable positions or engaging in willful or reckless conduct.

- Understatement due to willful or reckless conduct — IRC § 6694 (b): The penalty is $5,000 or 75% (whichever is greater) of the tax preparer's income for preparing the tax return or claim.

- Failure to furnish a copy to the taxpayer — IRC § 6695(a): The penalty is $50 for each instance of failure to provide a copy of the tax return or refund claim to the taxpayer, with a maximum penalty of $27,000 in 2022. The penalty increases to $55 and $60 for returns filed in 2023 and 2024, respectively, with a maximum penalty of $30,000. For returns filed in 2025, the penalty remains $60 per failure, but the maximum penalty increases to $31,500.

- Failure to sign the return — IRC § 6695(b): The penalty is $50 for each instance of failure to sign a tax return or refund claim, with a maximum penalty of $27,000.

- Failure to furnish an identifying number — IRC § 6695(c): The penalty is $50 for each instance of failure to include a preparer tax identification number (PTIN) on a tax return or claim, with a maximum penalty of $27,000 in 2022. The penalty increases to $55 and $60 for returns filed in 2023 and 2024, respectively, with a maximum penalty of $30,000. For returns filed in 2025, the penalty remains $60 per failure, but the maximum penalty increases to $31,500.

- Failure to retain a copy or list — IRC § 6695(d): The penalty is $50 for each instance of failure to keep a copy or list of a tax return or claim prepared, with a maximum penalty of $27,000 in 2022.

- Failure to file correct information returns — IRC § 6695(e): The penalty is $50 for each instance of failure to include correct information on tax returns, with a maximum penalty of $27,000 in 2022. The penalty increases to $55 and $60 for returns filed in 2023 and 2024, respectively, with a maximum penalty of $30,000. For returns filed in 2025, the penalty remains $60 per failure, but the maximum penalty increases to $31,500.

- Negotiation of check — IRC § 6695(f): In 2022, the penalty is $545 for a tax preparer who endorses or negotiates any check payable to another person. The penalty increases to $560 and $600 for returns filed in 2023 and 2024, respectively.

It's important to note that these penalties are subject to change and may have been updated since the last published date. The IRS may consider reducing or removing penalties if you acted in good faith and can demonstrate reasonable cause for not meeting your tax obligations.

Cybersecurity Law: A Historical Perspective

You may want to see also

Frequently asked questions

Some IRS penalties for noncompliance with tax law include:

- Underpayment of estimated tax by individuals penalty

- Accuracy-related penalty

- Failure-to-file penalty

- Failure-to-pay penalty

- Tax preparer penalties

The IRS may reduce or remove penalties if:

- You acted in good faith and can show reasonable cause for why you weren't able to meet your tax obligations

- The underpayment is the result of a casualty, local disaster, or other unusual circumstance when it would not be fair to impose the penalty

- You qualify for First Time Abate penalty relief

- You can show that the failure was due to reasonable cause and not due to willful neglect

If you receive an IRS penalty notice with incorrect information, you should:

- Call the IRS to review its account or send correspondence noting the error

- Confirm that all extensions, payments, and total tax are reflected as expected on the notice

- Follow the instructions on the notice or letter, which will include information about the penalty, the reason for the charge, and what to do next