Retirement plans are the second most sought-after benefit after health insurance, and 401k plans are a powerful tool for employers to attract top talent. While companies are not legally required to offer a 401k plan or match employee contributions, matching contributions can provide tax benefits for the business. The amount a company can match by law depends on the type of 401k plan and the vesting schedule. For instance, in a safe harbor plan, employers can match each eligible employee's contribution, dollar-for-dollar, up to 3% of their compensation, and 50 cents on the dollar for contributions exceeding 3% but not 5%. Alternatively, they can make a 3% nonelective contribution to each eligible employee's account.

| Characteristics | Values |

|---|---|

| Average employer contribution | 4.8% |

| Typical plan contribution | 4% |

| Maximum income for a full employer match in 2024 | $345,000 |

| Maximum employee contribution in 2024 | $16,000 |

| Maximum employee contribution in 2023 | $15,500 |

| Maximum employee contribution in 2022 | $14,000 |

| Maximum employee contribution in 2021 and 2020 | $13,500 |

| Maximum employee contribution in 2019 | $13,000 |

| Maximum employee contribution in 2024 (aged 50 or over) | $23,000 |

| Maximum employee contribution in 2024 (aged 50 or over) with catch-up contributions | $30,500 |

| Average employer match in 2025 | 4% to 6% |

| Most common structure for employer match | 50% partial match |

| Maximum employer and employee contribution in 2024 | $69,000 |

| Maximum employer and employee contribution in 2024 (aged 50 or over) with catch-up contributions | $76,500 |

| Typical vesting period for employer 401(k) contributions | 5 years |

| Maximum tax deduction for employer | 25% of total compensation paid to employees |

Explore related products

What You'll Learn

![]()

Vesting schedules and employee retention

Vesting schedules can be a valuable tool for employee retention. Vesting refers to the process employees go through to unlock their ownership rights to assets and benefits. In the context of 401(k) plans, vesting schedules determine when employees acquire full ownership of the portion contributed by the employer.

A common vesting period is between three and five years, but this can vary depending on the employer and the type of vesting schedule in place. There are two main types of vesting schedules: cliff vesting and graded vesting. Cliff vesting gives the employee ownership of 100% of the employer's contributions all at once after a certain number of years, typically three years. Graded vesting, on the other hand, gives the employee ownership of a percentage of the employer's contribution each year. For example, in a six-year graded vesting schedule, the employee would be vested in 0% of the assets in the first year, 20% in the second year, 40% in the third year, and so on until they reach 100% vesting in the sixth year.

The use of vesting schedules can incentivize employees to stay with the company for a longer period of time. By tying the ownership of employer contributions to a vesting schedule, employers create a disincentive for employees to leave before the vesting period is complete. This is because employees may forfeit their employer match or a portion of it if they leave or are terminated before the vesting period ends.

While vesting schedules can be a useful tool for employee retention, it is important to note that research on this topic has yielded mixed results. Some studies suggest that vesting schedules do not have a significant impact on retention, as employees may be unaware of vesting requirements or may prioritize other factors when considering whether to leave their jobs. However, other sources argue that vesting schedules can still be beneficial for containing costs and improving retirement security for employees.

To maximize the potential benefits of vesting schedules for employee retention, it is crucial for employers to engage with experts in employer-sponsored retirement plans. This ensures that the vesting schedule is appropriately aligned with the goals and needs of the organization.

Can Cities Face RICO Lawsuits?

You may want to see also

Explore related products

$22.99 $16.99

![]()

Employer tax benefits

There are several employer tax benefits associated with 401(k) matching contributions. Firstly, employers can deduct matched contributions from their income taxes, leading to significant tax savings. Additionally, 401(k) matching can help attract and retain top talent, as employees value companies that offer strong benefits packages, including retirement plans.

Moreover, 401(k) matching can be more financially beneficial for both employees and employers than a pay raise. When employees receive a raise or bonus, they are subject to income and employment taxes on the additional income. In contrast, 401(k) matching contributions are often tax-deferred, providing tax advantages to both parties.

Qualifying businesses may also receive tax credits for a portion of the startup costs associated with implementing a 401(k) plan, including expenses for setup, administration, and employee education. These tax credits can further reduce the net cost of offering a 401(k) plan for employers.

Furthermore, employers have the flexibility to choose from various matching structures, such as dollar-for-dollar matching up to a certain percentage of employee compensation or partial matching contributions. This flexibility allows employers to design a matching program that aligns with their financial capabilities and business conditions.

Lastly, 401(k) plans can help employers meet legal requirements in certain states that mandate retirement plans for companies above a certain size. By offering a 401(k) plan, employers can ensure they comply with state legislation while also providing a valuable benefit to their employees.

The Law on Nighttime Escapades: Punishment for Sneaking Out?

You may want to see also

![]()

Contribution matching methods

Matching 401k contributions are additional funds that an employer contributes to an employee's 401k retirement plan. This is typically done as a percentage of the employee's total contribution, up to a certain limit. The most common type of matching is a 50% partial match, where the employer contributes half of the employee's contribution, up to a maximum of 6% of the employee's salary. For example, if an employee contributes $100, the employer will contribute $50. This is also known as a dollar-for-dollar match, where the employer matches the employee's contribution dollar for dollar up to a certain percentage of their salary.

Employers can also offer a full match, where they match 100% of the employee's contributions up to a specified limit. This is the best type of match for employees as it allows them to maximize their retirement savings. In this case, if an employee contributes $1, the employer will also contribute $1. It's important to note that employers are not required by law to offer any matching contributions, and the percentage they choose to match is at their discretion.

Some companies may also offer a true-up option, where they make up the difference if an employee doesn't get the full annual match because they maxed out their 401k contributions too early in the year. Additionally, employers can make non-matching contributions to an employee's 401k retirement savings account even if the employee doesn't contribute, as a way to attract or retain talent. These non-matching contributions can be a set percentage of an employee's compensation, such as 3%, and they are made to each eligible employee's account.

Vesting schedules also play a role in contribution matching. Vesting refers to how much of the employer's contributions belong to the employee, and it is based on how long the employee has worked at the company. Some companies offer immediate vesting, while others have a waiting period. If an employee leaves the company before their contributions are fully vested, they may forfeit some or all of the employer's matched contributions. A typical vesting period for employer 401k contributions is five years.

Finally, it's worth noting that employer contributions to 401k plans offer tax benefits for businesses. Companies can deduct matching contributions on their federal income tax returns up to a specific amount determined by the IRS, usually up to 25% of the total compensation paid to employees.

Gaining Support: Strategies for Bills in Congress

You may want to see also

![]()

Contribution timing

The timing of contributions to a 401(k) plan is essential and can impact the overall value of the plan over time. The Department of Labor (DOL) has strict guidelines on how long an employer can hold elective deferrals before depositing them into the plan. The general rule is that contributions must be deposited as soon as it is reasonably possible to separate them from the company's assets, but no later than the 15th business day of the month following the month in which amounts are withheld from pay. This 15-day deadline is not a safe harbour, and the DOL may consider a shorter period as more reasonable.

For plans with fewer than 100 participants at the start of the plan year, the DOL provides a safe harbour standard, where deposits made within seven business days of a pay date are considered timely. This is optional, and smaller plans may choose to follow this seven-day guideline or the general 15-day deadline.

Employers may match contributions according to different schedules, such as twice a year, every two weeks, or per pay period. It is important for employees to understand their company's matching schedule, as failing to make a contribution according to the schedule could result in missing out on matching funds for that period. For example, if an employer matches per pay period and an employee maxes out their contributions early in the year, they may not receive the match for the remainder of the year. Some companies may offer a "true-up" to make up for this discrepancy and ensure employees receive the full annual match.

Additionally, vesting schedules impact the timing of contributions. Vesting refers to how much of the employer's contributions belong to the employee based on their tenure at the company. A typical vesting period for employer 401(k) contributions is five years, and employees may forfeit some or all of the employer's contributions if they leave before this period ends.

There are also annual deadlines for employer matching contributions, which depend on the company's tax status and contribution type. For deductibility purposes, contributions must be deposited by the due date (including extensions) of the company's federal tax return. For "annual additions" purposes, safe harbour matching contributions calculated per payroll must be deposited by the end of the following plan year quarter.

Consequences for missing contribution deadlines can range from mild to severe, including losing tax deductions, paying penalties, or even plan disqualification.

The Abortion Law: Can It Be Overturned?

You may want to see also

![]()

Contribution limits

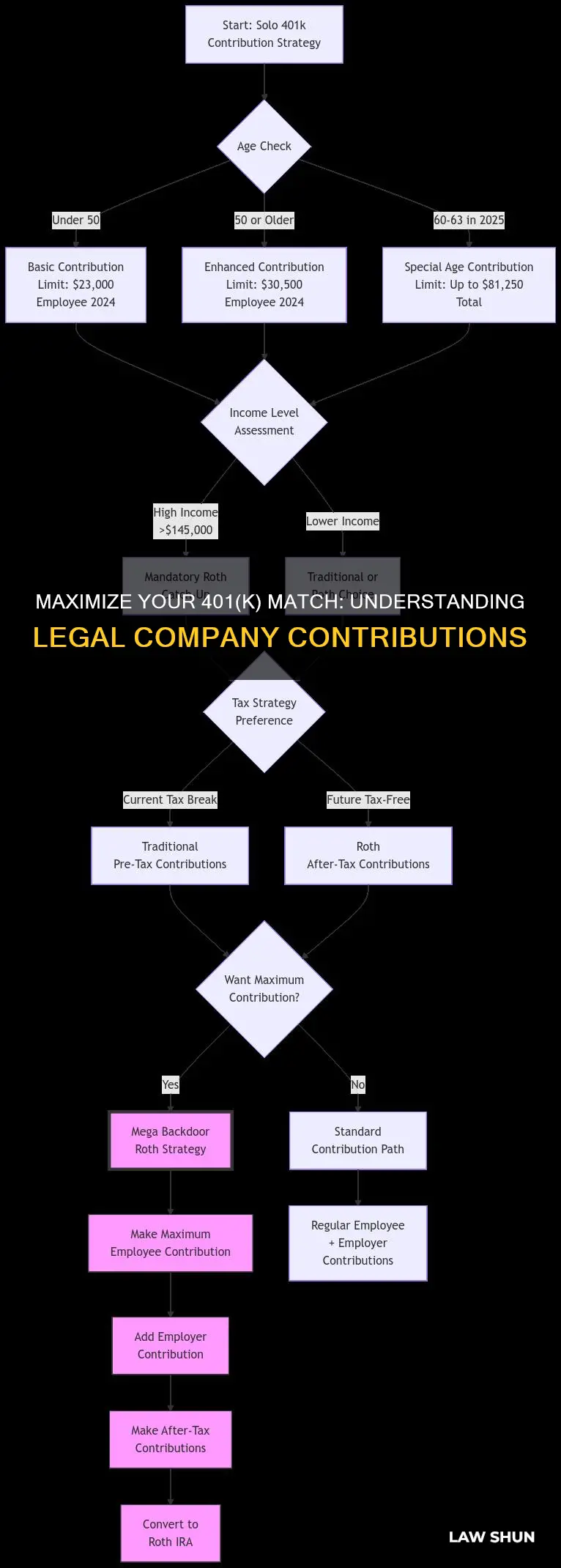

The contribution limits for 401(k) plans are reviewed and sometimes adjusted annually by the Internal Revenue Service (IRS) to reflect the effects of inflation. The IRS also sets clear guidelines for 401(k) contribution limits each year that both employees and employers must adhere to.

For 2025, the contribution limit for employee salary deferrals is $23,500, with a catch-up contribution of $7,500 for those aged 50 and over, and $11,250 for those aged 60 to 63. The total contribution limit for employers and employees combined is $70,000, or $77,500 with the catch-up contribution.

In 2024, the contribution limit for employee salary deferrals was $23,000, with a catch-up contribution of $7,500 for those aged 50 and over. The total contribution limit for employers and employees combined was $69,000, or $76,500 with the catch-up contribution.

For 2023, the contribution limit for employee salary deferrals was $22,500, with a catch-up contribution of $7,500 for those aged 50 and over. The total contribution limit for employers and employees combined was $66,000.

It is important to note that these limits do not include any post-tax contributions, which may be made in addition to pre-tax and Roth contributions. However, the total contributions cannot exceed the annual compensation of the employee at the company sponsoring the plan.

Employers can contribute to their employees' 401(k) accounts in addition to employee salary deferrals. Employer contributions can be made as a percentage of each employee's compensation (nonelective contribution) or by matching the amount the employee contributes (matching contribution). Alternatively, employers can do both. For example, an employer may decide to contribute 50% of an employee's contribution, resulting in a 50-cent increase for every dollar the employee sets aside.

Employers can also match each eligible employee's contribution dollar-for-dollar, up to 3% of the employee's compensation. For contributions exceeding 3% but not 5%, the employer can contribute 50 cents on the dollar. Under a traditional 401(k) plan, the amount of nonelective contributions can be changed annually according to business conditions.

A common partial match provided by employers is 50% of what the employee contributes, up to 6% of their salary. For instance, if an employee earns $80,000 per year, the contributions that will be eligible for matching are 6% of their salary, or $4,800. To maximise the amount of 401(k) match, the employee must contribute at least 6%. If the employee contributes more, the employer will still only match half of 6% of the salary, as that is the maximum.

It is important to understand the vesting schedule for employer contributions, as this determines how much of the employer contributions belong to the employee based on their length of service at the company. A typical vesting period for employer 401(k) contributions is five years.

Additionally, employees who qualify as highly compensated employees (HCEs) may not be eligible for a full employer match. The IRS defines an HCE as someone who owns more than 5% of a company or whose compensation exceeds a certain dollar limit, placing them in the top 20% of earners at their employer. In 2024, the HCE threshold was set at $155,000 in compensation, and the maximum income an employer could match was $345,000.

Aiming for UGA Law: Is an LSAT Score of 159 Enough?

You may want to see also

Frequently asked questions

A 401k match is when your employer contributes a certain amount to your retirement savings plan based on how much you contribute.

By law, companies can match up to 3% of an employee's compensation. They can also contribute 50 cents on the dollar for an employee's contribution that exceeds 3% but is less than 5% of their compensation.

The maximum that an employer and employee can contribute together is $69,000 in 2024. This limit increases to $76,500 for employees who are 50 or older.

No, companies are not required to match employee contributions or even offer a 401k plan. However, 98% of companies with a 401k plan also offer matching contributions.