The US tax code is a complex and ever-changing landscape, with new laws and adjustments being made regularly. The Internal Revenue Service (IRS) makes annual inflation adjustments, with over 60 tax provisions updated for the 2025 tax year. These adjustments can impact tax planning strategies and affect individuals, businesses, tax-exempt organizations, and governments. The Tax Cuts and Jobs Act (TCJA) of 2017 has also had a significant impact on taxes, with the One Big Beautiful Bill Act passed in July 2025 making some of its provisions permanent. The Senate Budget Bill has proposed tweaks to international tax policy, targeting US multinationals that hold intangible assets in low-tax jurisdictions to avoid US taxes. These changes aim to reduce revenue losses and encourage domestic investment. With frequent revisions and updates, it's important for taxpayers and businesses to stay informed about the latest tax laws and their implications.

| Characteristics | Values |

|---|---|

| Tax Year | 2025 |

| Tax Adjustments | Inflation adjustments |

| Tax Items | Standard deductions, marginal rates, alternative minimum tax exemption amounts |

| Standard Deduction | $15,000 for single taxpayers, $30,000 for married couples filing jointly, $22,500 for heads of households |

| Marginal Rates | 37% for individual single taxpayers with incomes greater than $626,350, 35% for incomes over $250,525, 32% for incomes over $197,300, 24% for incomes over $103,350, 22% for incomes over $48,475, 12% for incomes over $11,925, 10% for incomes $11,925 or less |

| Alternative Minimum Tax Exemption Amounts | $88,100 for unmarried individuals, $68,650 for married individuals filing separately |

| Tax Laws | Tax Cuts and Jobs Act (TCJA), One Big Beautiful Bill Act |

| Tax Brackets | Adjustments to tax brackets |

| Deductions | No limitation on itemized deductions, Lifetime Learning Credits |

| Retirement Contributions | No impact on retirement plan contribution limits |

| Tax Exemptions | Tax-exempt organizations |

| International Tax Policy | Senate Budget Bill revisits key international provisions of TCJA, taxes foreign profits, rewards exports, reduces revenues |

| Global Minimum Corporate Tax | 15% |

Explore related products

What You'll Learn

![]()

Tax Expenditures

The Congressional Budget and Impoundment Control Act of 1974 defines tax expenditures as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability." These provisions support favoured activities or groups of taxpayers. The Office of Management and Budget (OMB) and the Congressional Joint Committee on Taxation (JCT) publish annual lists of tax expenditures and estimates of their associated revenue losses.

Examples of tax expenditures include individual itemized deductions for charitable contributions, mortgage interest expense, and state and local taxes. These deductions can have a greater impact on revenue when considered individually rather than jointly. Exclusions from income, such as employment-based health insurance and pension contributions, also result in tax expenditures. Deductions from income, such as state and local taxes and mortgage interest, contribute to revenue losses. Preferential tax rates, such as those on capital gains and dividends, are another form of tax expenditure.

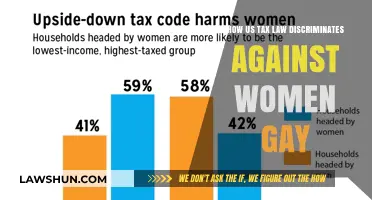

The distribution of tax expenditures across the income scale is uneven, with higher-income households receiving a disproportionately larger share. According to the Center on Budget and Policy Priorities, the top 1% of US households by income received approximately 17% of all tax expenditure spending in 2013, while the top 20% received 51%. Tax expenditures can be influenced by political ideologies, with Republicans tending to increase them, benefiting businesses and the wealthy.

The cost of tax expenditures varies annually with economic activity levels, and they can have timing effects. The present value estimates provide a more meaningful measure of the cost for certain types of tax expenditures with offsetting revenue impacts over time. Negative tax expenditures refer to revenue-increasing tax provisions, such as denying certain deductions or phasing out personal exemptions for high-income taxpayers.

Is "Brother-in-Law" Hyphenated? Capitalization Rules Explained

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Retirement plans

Secure Act 2.0

The Secure Act 2.0 introduces significant changes to retirement plans, aiming to facilitate retirement savings and encourage employers to sponsor tax-favoured retirement plans. One notable provision is the reduction in the eligibility timeframe for part-time workers to access company retirement plans. Previously, it took three years, but now part-time employees working 500 hours or more annually for two consecutive years can qualify. This provision takes effect in 2025, and to be covered, the employee must be at least 21 by the end of the second year.

Penalty-Free Emergency Withdrawals

The Secure Act 2.0 also allows taxpayers to make one penalty-free distribution of up to $1,000 per year from their tax-favoured retirement plans for emergency expenses. This distribution can be repaid over three years, and during this period, no further emergency distributions are permitted unless the previous one is restored. Additionally, employers can now automatically enrol employees in emergency savings account programs funded by after-tax contributions.

K) Plans

The IRS has increased the contribution limit for 401(k) plans for 2025 to $23,500, a $500 increase from 2024. Additionally, catch-up contribution limits will be adjusted for inflation. For 2025, taxpayers aged 60 to 63 can contribute an extra $10,000 to their 401(k)s, up from $7,500. However, catch-up contributions for incomes over $145,000 will not be tax-deferred and will be treated as Roth contributions.

Required Minimum Distributions (RMDs)

The age at which RMDs kick in has been increasing. For those born in 1960 or later, RMDs commence at age 75. However, for those born between 1951 and 1959, RMDs start at age 73. It's important to note that RMD rules apply to various retirement plans, including 401(k) plans, traditional IRAs, and IRA-based plans.

Tax Strategies

When considering retirement tax strategies, it's important to remember that there is no one-size-fits-all approach. Consult a tax professional for personalised advice. However, some general strategies include:

- Tapping taxable accounts first, then tax-deferred, and finally tax-free accounts.

- Considering the timing of withdrawals to avoid bumping into a higher tax bracket.

- Taking advantage of tax-free withdrawals from health savings accounts for qualified medical expenses.

- Exploring the benefits of converting traditional IRA balances to Roth, especially in the early retirement years.

The Ultimate Guide to Using Apostrophes in Brother-in-Law

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act (TCJA) is a United States federal law that amended the Internal Revenue Code of 1986. It was enacted in 2017 and is also known as the Trump Tax Cuts. The TCJA made significant changes to individual and business taxes, with the aim of simplifying the tax code and boosting the economy.

One of the key provisions of the TCJA was the reduction in corporate income tax rates from 35% to 21%, which was expected to increase corporate investment and make the US a more attractive destination for foreign investment. The act also included a variety of other tax cuts and changes, such as increasing the standard deduction for single filers to $12,400 and $24,800 for married filers, eliminating personal exemptions, and limiting certain itemized deductions.

The TCJA was projected to lower taxes across the board, with the top 20% of Americans by income expected to receive around 65% of the tax savings. However, it was also estimated that 72% of taxpayers would be adversely impacted if the tax cuts were paid for by spending cuts, as these would primarily affect lower- to middle-income taxpayers.

While the TCJA did lead to an increase in corporate investment, its effects on economic growth and median wages were smaller than expected. Additionally, the act contributed to an increase in federal debt. Some analysts have argued that the benefits of the TCJA were unevenly distributed, disproportionately favouring the most affluent.

In 2025, the "One Big Beautiful Bill Act" was passed, making permanent certain provisions of the TCJA that were initially set to expire at the end of 2025. These adjustments may have significant implications for taxpayers' future tax planning strategies.

The First Law Series: Is It Over?

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

Tax Brackets

The US tax code is notoriously complex, and tax brackets are no exception. The federal income tax system has seven tax brackets, ranging from 10% to 37%. These brackets are adjusted annually for inflation, and the income limits for each bracket vary depending on filing status. For example, in 2025, the top tax rate of 37% applies to single taxpayers with incomes greater than $626,350, while married couples filing jointly must have incomes above $751,600 to fall into this bracket.

The IRS uses the Chained Consumer Price Index (C-CPI) to adjust income thresholds, deduction amounts, and credit values. These adjustments ensure that income tax brackets remain in line with changes in the cost of living. However, "bracket creep" can occur when inflation pushes taxpayers into higher income tax brackets, leaving them with less money and increasing government spending.

The Tax Cuts and Jobs Act (TCJA) of 2017 included several provisions related to tax brackets, some of which were made permanent in 2025. These include lower tax brackets, increased standard deductions, and a higher lifetime estate tax exemption amount. Additionally, the TCJA eliminated the limitation on itemized deductions for tax years 2018 and beyond.

It's important to note that tax planning strategies may be impacted by changes in tax laws and brackets. Taxpayers should consult with tax professionals to understand how these changes affect their financial plans and to make informed decisions.

Explore Law Specializations with These Courses

You may want to see also

Explore related products

$14.83 $15.95

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![]()

Tax Treaties

The United States has income tax treaties with several foreign countries. These treaties allow residents of foreign countries to be taxed at a reduced rate or exempt them from US income taxes on certain income, profit, or gain from sources within the US. These reduced rates and exemptions vary among countries and specific items of income. For instance, if a US citizen or resident receives income from a treaty country, they may be entitled to certain credits, deductions, exemptions, or reduced tax rates in that foreign country.

The US income tax treaties are reciprocal, meaning they apply to both treaty countries. These treaties also contain a “saving clause” that prevents US citizens or residents from using the provisions of a tax treaty to avoid taxation on US source income. If there is no applicable treaty, individuals must pay tax on the income at the standard rates.

It is important to note that some US states honor the provisions of these tax treaties, while others do not. Therefore, individuals should consult the tax authorities of their specific state to determine if their income is subject to state taxation and whether any applicable tax treaties are recognized.

To claim benefits under an income tax treaty, dual resident taxpayers must file a return using Form 1040-NR or Form 1040-NR-EZ and compute their tax as a nonresident alien. They must also attach a completed Form 8833, Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b). Additionally, the income tax treaty between the two countries must include a provision to resolve conflicting claims of residence.

The full text of these treaties, along with related documents such as Tax Information Exchange Agreements (TIEAs) and the Foreign Account Tax Compliance Act (FATCA), can be found on the US Department of the Treasury website. The Office of Tax Policy within the department is responsible for negotiating these tax treaties and providing economic and legal policy analysis for domestic and international tax policy decisions.

The First Immigration Law: A Historical Perspective

You may want to see also

Frequently asked questions

For the 2025 tax year, the standard deduction for single taxpayers is $15,000, while for married couples filing jointly, it is $30,000. The tax rates also differ depending on the income and filing status. For example, for 2025, the 37% tax rate applies to individual single taxpayers with incomes greater than $626,350, while for married couples filing jointly, this rate applies to incomes greater than $751,600.

Tax laws can affect retirement plans in various ways. For example, the 2025 tax year adjustments included changes to retirement contributions. While the 2017 Tax Cuts and Jobs Act (TCJA) did not impact retirement plan contribution limits, the 2025 tax laws may influence tax planning strategies for retirement contributions.

The Senate Budget Bill proposes revisions to the Global Intangible Low-Taxed Income (GILTI) provision of the TCJA. The revised GILTI would tax all net income of foreign subsidiaries at 12.6%, up from the current 10.5%. This aims to curb profit shifting by US multinationals, who often hold intangible assets in low-tax jurisdictions.

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)

![H&R Block Tax Software Basic 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/5181AWwUanL._AC_UL320_.jpg)

![[Old Version] TurboTax Home & Business 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71K4wikrrkL._AC_UL320_.jpg)