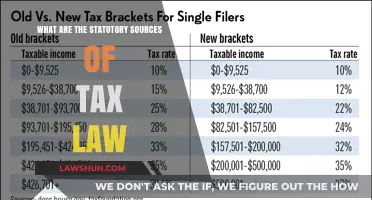

There are several administrative sources of tax law in the United States, including the Internal Revenue Code (IRC), Treasury regulations, case law, and agency guidance published by the Internal Revenue Service (IRS). The IRC is the foundation of federal tax authority and is interpreted by Treasury regulations, cases that interpret the laws, and IRS rulings. The Treasury Department has the authority to interpret and administer the IRC, and the IRS, as a division of the Treasury Department, is responsible for overseeing the implementation of the IRC. The IRS issues various pronouncements, including regulations, revenue rulings, revenue procedures, and letter rulings, to explain and enforce tax laws. These pronouncements are published in the Internal Revenue Bulletin (IRB) and provide guidance to taxpayers, firms, and charitable organizations. State tax laws also have their administrative sources, with each state having a regulatory tax agency that passes administrative regulations and rulings.

| Characteristics | Values |

|---|---|

| Authority | The Internal Revenue Code (IRC) is the foundation of federal tax authority in the US. The IRC is interpreted by Treasury regulations, cases that interpret the laws, and IRS rulings. |

| Administrative Bodies | The Treasury Department is charged with administering tax laws and has delegated authority to the Internal Revenue Service (IRS), a division of the Treasury Department, to oversee the implementation of the IRC. |

| Types of Pronouncements | Regulations, revenue rulings, revenue procedures, and letter rulings. |

| Official Publications | The IRS publishes its pronouncements in the Internal Revenue Bulletin (IRB), which includes new tax laws, procedural rules, treasury decisions, and other notices. |

| Binding Nature | Treasury regulations are binding on the IRS but not on the courts. IRS rulings have precedential value for taxpayers with similar fact patterns. |

| State Tax Law | Each state has a regulatory tax agency that passes state administrative regulations and rulings, similar to the federal system. State courts also generate judicial opinions, but most states lack an official tax court. |

Explore related products

$89 $99.99

What You'll Learn

![]()

The Internal Revenue Service (IRS)

The IRS was established in 1913 after the ratification of the Sixteenth Amendment, which authorized Congress to impose a tax on income. Originally called the Bureau of Internal Revenue, the agency was renamed the Internal Revenue Service in 1953 and has since undergone numerous reforms and reorganizations. One notable reorganization occurred in 1952 under a plan put forward by President Truman, which decentralized many functions to new district offices and replaced politically appointed collectors with civil service directors.

The IRS plays a crucial role in funding the federal government. For the 2023 fiscal year, the IRS collected approximately $4.7 trillion, which accounts for about 96% of the federal government's operational funding. The IRS collects taxes from various sources, including income tax, which has seen a significant increase in the number of taxpayers over the years, especially during World War II.

The IRS has the authority to issue binding rules and regulations concerning the IRC. There are four major types of pronouncements that the IRS may issue: regulations, revenue rulings, revenue procedures, and letter rulings. These pronouncements are published in the Internal Revenue Bulletin (IRB), which serves as the official publication for IRS pronouncements. The IRB includes new tax laws, committee reports, procedural rules, tax treaties, treasury decisions, and other notices.

In addition to its tax collection and enforcement responsibilities, the IRS also provides guidance to taxpayers, firms, and charitable organizations through the Office of Chief Counsel. This guidance helps translate the specifics of tax laws into detailed regulations, rules, and procedures that are more easily understandable and applicable.

Laws of Motion: Understanding the Core Principles

You may want to see also

Explore related products

![]()

The Internal Revenue Code (IRC)

The IRC covers income, estate and gift, employment, and excise taxes, as well as procedure and administration. It does not include all federal tax statutes, and there are tax laws found in other federal statutes, such as USC Title 11 (bankruptcy) and Title 28 (judiciary). The IRC is also supplemented by individual laws passed by Congress and signed into law by the President, which amend the IRC and include additional information such as effective dates, transitional rules, and special rules.

The IRC has had three major amendments: the 1939 Code, the 1954 Code, and the current 1986 Code. Federal tax laws were enacted in individual revenue acts prior to the 1939 Code. The IRC is complex, and its sections must be read in the context of the entire Code, the Treasury Regulations, and court decisions that interpret it.

Treasury regulations, also known as federal tax regulations, provide the official interpretation of the IRC by the U.S. Department of the Treasury. They give directions to taxpayers on how to comply with the IRC's requirements. Treasury regulation sections can be found in Title 26 of the Code of Federal Regulations (26 CFR). Regulations are the highest administrative authority issued by the Treasury Department. They are published in the Federal Register and are updated annually on April 1st.

The IRS's official publication for its pronouncements is the Internal Revenue Bulletin (IRB). It includes new tax laws, committee reports, procedural rules, new tax treaties, treasury decisions, and other notices.

Spherical Law of Sines: Who First Presented It?

You may want to see also

Explore related products

![]()

Treasury Department regulations

The Treasury Department is responsible for administering US tax laws and is tasked with interpreting and enforcing the Internal Revenue Code (IRC). The Internal Revenue Service (IRS) is a division of the Treasury Department and is responsible for the day-to-day operations associated with the administration of the IRC.

Treasury regulations are the official interpretations of the IRC and are a source of federal income tax law. They are issued by the IRS and constitute one of the major categories of primary tax authority. These regulations are located in Title 26 of the Code of Federal Regulations (CFR) and are updated annually on April 1.

The Treasury Department has the authority to promulgate final regulations, which are published in the Federal Register. Before issuing final regulations, the department must first publish proposed regulations and allow the public time to comment on them. Proposed regulations may offer guidance for a specific section of the Code and can be useful in determining a taxpayer's liability for a given year. However, they generally do not have the force of law and are not considered precedent.

Temporary regulations, on the other hand, go into effect immediately upon publication in the Federal Register and are effective for three years. They are initially published as Treasury Decisions (TDs) and include an explanatory preamble that can be helpful for legal research. Temporary regulations are often issued to address urgent matters or to fill gaps in the tax law until final regulations can be issued.

Final regulations are published in the Federal Register and codified in Title 26 of the CFR. They have the full force of law and are the highest administrative authority issued by the Treasury Department. These regulations are binding and must be followed by taxpayers and the IRS alike.

Treasury regulations play a crucial role in interpreting and enforcing the IRC, ensuring that tax laws are applied consistently and fairly. They provide clarity and guidance to taxpayers and tax professionals, helping them understand their rights and obligations under the tax law.

Explore the Diverse Branches of IP Law

You may want to see also

Explore related products

![]()

IRS rulings and procedures

The Internal Revenue Service (IRS) is a division of the US Treasury Department. The IRS plays a crucial role in administering the tax laws enacted by Congress, and it must translate these laws into detailed regulations, rules, and procedures. The Office of Chief Counsel produces several different kinds of documents and publications that provide guidance to taxpayers, firms, and charitable groups.

Revenue rulings are an official interpretation by the IRS of the Internal Revenue Code (IRC), related statutes, tax treaties, and regulations. They are the conclusion of the IRS on how the law is applied to a specific set of facts. Revenue rulings are published in the Internal Revenue Bulletin (IRB) for the information of and guidance to taxpayers, IRS personnel, and tax professionals. For example, a revenue ruling may hold that taxpayers can deduct certain automobile expenses.

Revenue procedures are official statements of a procedure that affect the rights or duties of taxpayers or other members of the public under the IRC, related statutes, tax treaties, and regulations. They are also published in the IRB and provide return filing or other instructions concerning an IRS position. For example, a revenue procedure might specify how those entitled to deduct certain automobile expenses should compute them by applying a certain mileage rate instead of calculating actual operating expenses.

A private letter ruling (PLR) is a written statement issued to a taxpayer that interprets and applies tax laws to the taxpayer's specific set of facts. A PLR establishes the federal tax consequences of a particular transaction before it is consummated or before the taxpayer's return is filed. It is issued in response to a written request submitted by a taxpayer and is binding on the IRS if the taxpayer fully and accurately described the proposed transaction. PLRs are generally made public after all information has been removed that could identify the taxpayer.

Civil vs Military Law: What's the Distinction?

You may want to see also

Explore related products

$200 $359

![Administrative Law: Cases and Materials [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/61uHBdS1IBL._AC_UY218_.jpg)

$34.66 $345

![]()

State tax laws

State tax statutes are found with the state code compilation for its respective state. Each state code compilation has a different name, and the easiest way to determine the name of a state code compilation is to use Jurisdiction Table 1 in the Bluebook. State tax laws can be researched using databases such as Westlaw, Lexis, and Tax Notes.

State courts generate judicial opinions, although most states do not have an official tax court. Some states have special tax tribunals that hear tax disputes before they enter the court system. At the state level, there are no state tax case reporters, and researchers must use the designated state digest and reporter system for their jurisdiction.

State personal and corporate income tax issues can be researched largely in the same way as federal tax research. Many states' personal income tax "piggybacks" on federal income tax. However, states also engage in a wide variety of different taxes unrelated to income, such as property taxes, sales and use taxes, excise taxes, estate and inheritance taxes, and liquor taxes.

The First Universal Law: Law of Attraction

You may want to see also

Frequently asked questions

Administrative sources of tax law include the Internal Revenue Code, Treasury regulations, case law, and several types of agency guidance published by the Internal Revenue Service (IRS).

The four key pronouncements are regulations, revenue rulings, revenue procedures, and letter rulings.

Revenue rulings are official declarations made by the IRS, stating how tax law applies to a specific set of facts. They have precedential value for taxpayers with similar fact patterns.