Capital gains tax is a tax imposed on the profits from the sale of assets. The rate of tax varies depending on the type of asset, how long it was owned for, and the income of the person selling the asset. Tax lot accounting is a record-keeping technique that traces the dates of purchase and sale, cost basis, and transaction size for each security in an investor's portfolio. Tax lots are used to help investors make strategic decisions about which assets to sell and when, in order to minimize the taxes owed on capital gains.

| Characteristics | Values |

|---|---|

| Definition | A tax lot is a record of all transactions and their tax implications (dates of purchase and sale, cost basis, sale price) involving a particular security in a portfolio. |

| Purpose | Tax lots help investors make strategic decisions about which assets to sell and when, allowing them to minimize taxes owed on their gains. |

| Record-Keeping Technique | Tax lot accounting traces the dates of purchase and sale, cost basis, and transaction size for each security in a portfolio, even if multiple trades are made in the same security. |

| Securities/Shares | Securities or shares purchased in a single transaction are referred to as "a lot" for tax purposes. Each tax lot will have a different cost basis depending on its purchase date and price. |

| Cost Basis Methods | FIFO (First-In-First-Out), LIFO (Last-In-First-Out), average cost basis, highest cost, lowest cost, and tax-efficient harvester loss methods are some common approaches. |

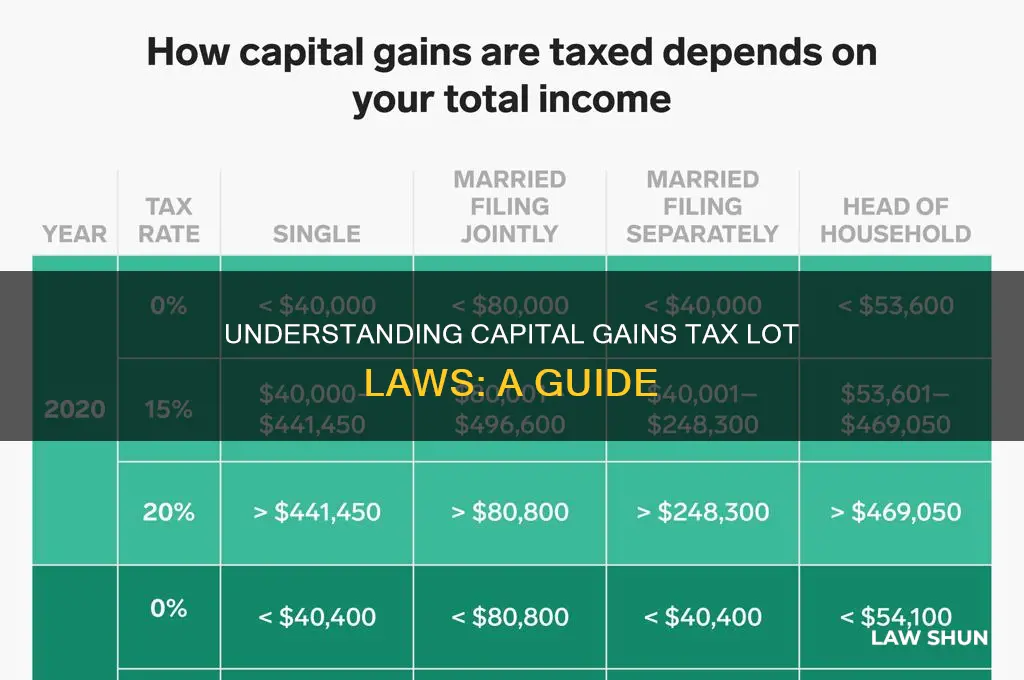

| Capital Gains Tax Rates | Long-term capital gains tax rates for 2024 and 2025 are 0%, 15%, or 20% of the profit, depending on the income and filing status of the taxpayer. Short-term capital gains are taxed at regular income tax rates, typically higher than long-term gains. |

| Capital Gains Tax Application | Capital gains taxes are owed on profits from the sale of assets, including stocks, bonds, investments, real estate, and personal items. It applies to assets held for more than a year, while short-term gains are taxed as ordinary income. |

Explore related products

What You'll Learn

![]()

Tax lot accounting methods

Tax lot accounting is a record-keeping technique that traces the dates of purchase and sale, cost basis, and transaction size of each security in a portfolio. It is a way of accounting for the purchase and sale of securities that allow investors to track the cost basis of individual lots of securities. It is simply a group of shares purchased at the same time and for the same price.

The goal of tax lot accounting is to minimize the net present value of current taxes by deferring the realization of capital gains and recognizing losses sooner. It allows investors to make strategic decisions about which assets to sell and when, making a big difference in the taxes owed on those investments.

The tax lot method is a crucial aspect of investment accounting, especially for those with complex and diverse portfolios. It provides investors with valuable insights into their cost basis, capital gains, and tax liabilities, enabling them to make informed decisions, optimize their investment strategies, and maintain compliance with tax regulations.

There are several tax lot accounting methods:

- First-In First-Out (FIFO): This is the default method for positions that aren't composed of many tax lots with varying acquisition dates or significant price discrepancies. It assumes that the first shares purchased are the first shares sold.

- Last-In First-Out (LIFO): When shares sold are chosen from the most recent lot, the LIFO method is used, and the realized gains are taxed as ordinary income.

- Average cost basis

- Highest cost

- Lowest cost

- Tax-efficient harvester loss methods

- Specific-shares method: This method helps investors minimize their gains by allowing them to choose specific tax lots.

Mr. Bennet's Brother-in-Law: Unveiling the Mystery Relative

You may want to see also

Explore related products

![]()

Capital gains tax rates

Short-term capital gains tax is a tax on profits from the sale of an asset held for one year or less. Short-term capital gains are treated as regular income and taxed according to ordinary income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, or 37%.

Long-term capital gains tax rates are 0%, 15%, or 20%, depending on taxable income and filing status. For example, for taxable years beginning in 2024, the tax rate on most net capital gains is no higher than 15% for most individuals. A capital gains rate of 0% applies if your taxable income is less than or equal to $94,050 for single filers or $63,000 for heads of households. A capital gains rate of 20% applies if your taxable income exceeds the thresholds set for the 15% capital gain rate.

There are a few other exceptions where capital gains may be taxed at rates greater than 20%. For instance, the taxable part of a gain from selling section 1202 qualified small business stock is taxed at a maximum rate of 28%. Net capital gains from selling collectibles such as coins, precious metals, antiques, or fine art are also taxed at a maximum rate of 28%. The portion of any unrecaptured section 1250 gain from selling section 1250 real property is taxed at a maximum rate of 25%.

High-earning individuals may also need to account for the net investment income tax (NIIT), an additional 3.8% tax that can be triggered if your income exceeds a certain limit.

The Evolution of Hate Crime Laws in the US

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

Capital gains and losses

Capital gains refer to the profits from the sale of assets. Most items that people own are considered capital assets, including investments such as stocks, bonds, cryptocurrency, or real estate, as well as personal items such as cars or boats. When you sell a capital asset for a higher price than its original value, the money you make is a capital gain. Conversely, when you sell an asset for less than its original value, the money you lose is a capital loss. The difference between your capital gains and losses is your net profit.

Capital gains taxes are owed on the profits made from selling assets. The amount of tax you pay depends on what you sold, how long you owned it before selling, your taxable income, and your filing status. Capital gains can be subject to either short-term or long-term tax rates. Short-term capital gains refer to profits from assets held for one year or less, and they are taxed at the same rate as your ordinary income. Long-term capital gains refer to profits from assets held for more than a year, and they are typically taxed at lower rates than short-term gains.

The long-term capital gains tax rates are 0%, 15%, or 20%, depending on the taxpayer's income and filing status. For instance, in 2024, the tax rate on most net capital gains is no higher than 15% for most individuals. However, if your taxable income exceeds certain thresholds, a capital gains rate of 20% may apply. Additionally, some assets, such as collectibles, may be subject to higher maximum tax rates of up to 28%.

To minimize taxes on capital gains, investors can use tax lots to manage their investment purchases and sales. Tax lot accounting is a record-keeping technique that traces the dates of purchase and sale, cost basis, and transaction size for each security in an investor's portfolio. Securities purchased in a single transaction are referred to as "a lot" for tax purposes. By thinking in terms of tax lots, investors can make strategic decisions about which assets to sell and when, thereby reducing the taxes owed on their investments.

Love Canal's Legacy: The Birth of Comprehensive Environmental Response

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)

$78.99 $84.99

![]()

Cost-basis methods

Cost basis is a key factor in determining capital gains and losses. It is the original value of a security, usually the purchase price plus any fees and commissions, adjusted for stock splits, non-dividend distributions, and other corporate actions. When you sell a security, your tax liability is determined by how much you spent to buy the security (cost basis) and the sale price.

There are several cost-basis methods that can be used to determine which lots of a security are liquidated first in a given sales transaction. This, in turn, helps identify the cost basis and holding period of the asset sold. The choice of cost-basis method can significantly impact the computation of capital gains and losses and the taxes owed on those investments.

One common method is the First In, First Out (FIFO) method, where the first shares purchased are the first sold. This is the default method for many brokers and is convenient for tracking cost basis. However, in some cases, it may be more beneficial to sell shares bought last, first. Another method is the low-cost lot method, where shares with the lowest cost basis are sold first. This method will generally result in the highest capital gain or lowest capital loss, which may lead to a higher current tax burden. The high-cost lot method is the opposite, where shares with the highest cost basis are sold first. This method results in the lowest capital gains or the greatest amount of realized losses for a sale, which may be useful for those interested in reducing taxable capital gains or tax-loss harvesting.

The specified lot method allows investors to target the exact shares to sell, offering flexibility and control over taxes. This method can be used to avoid realizing short-term capital gains or specifically target a certain amount of capital gains to fill up a tax bracket. However, it requires manual selection of each share to be sold and cannot be set as an account default. The average cost method calculates the cost basis by taking the total cost of the shares and dividing it by the number of shares in the fund.

The choice of cost-basis method depends on the investor's goals and circumstances. It is important to understand the tax implications of each method to make strategic decisions about which assets to sell and when.

Who Makes the Rules for Apartment Rentals?

You may want to see also

Explore related products

![]()

Tax implications

Capital gains taxes are owed on profits made from the sale of assets. The amount of tax owed depends on the asset sold, the duration of ownership, the owner's taxable income, and their filing status. Capital gains can be subject to either short-term or long-term tax rates.

Short-term capital gains refer to profits from the sale of assets held for a year or less. These gains are treated as regular income and taxed according to ordinary income tax brackets, typically ranging from 10% to 37%. Short-term gains on certain assets, such as collectibles, may be taxed at graduated tax rates.

Long-term capital gains refer to profits from the sale of assets held for more than a year. The tax rates for long-term capital gains are 0%, 15%, or 20%, depending on the taxpayer's income and filing status. For single filers, a 20% tax rate applies to those with an income of $518,900 or higher in 2024. For married couples filing jointly, the 20% rate applies to incomes above $583,750. The rate drops to 15% for incomes between $47,025 and $518,900 for single filers ($94,050 to $583,750 for married couples filing jointly) and 0% for those below these thresholds.

High-earning individuals may also be subject to the net investment income tax (NIIT), an additional 3.8% tax triggered if their income exceeds a certain limit. Long-term capital gains on "collectible assets," such as coins, precious metals, antiques, and fine art, are taxed at a maximum rate of 28%.

To minimize taxes on capital gains, investors can utilize tax lot accounting. This record-keeping technique involves tracking the dates of purchase and sale, cost basis, and transaction size for each security in a portfolio. By considering each purchase or sale as a separate tax lot, investors can make strategic decisions about which assets to sell and when. For example, an investor can choose to sell assets with higher cost bases first to reduce their capital gains. Additionally, the choice of cost-basis method, such as FIFO or LIFO, can significantly impact the computation of capital gains and, consequently, the taxes owed.

Parol Evidence Rule: What It Is and Why It Matters

You may want to see also

Frequently asked questions

A capital gains tax lot law is a record-keeping technique that traces the dates of purchase and sale, cost basis, and transaction size for each security in an investor's portfolio. Securities purchased in a single transaction are referred to as "a lot" for tax purposes.

The tax lot law helps investors make strategic decisions about which assets to sell and when to sell them. It also helps them minimize the taxes they owe on their gains.

The choice of cost-basis method can significantly impact the computation of capital gains and losses. For instance, the First-In-First-Out (FIFO) method is the default in most software packages and is convenient for tracking the cost basis.

Some general rules of thumb for minimizing capital gains taxes include:

- Avoid short-term gains by always selling your highest-cost positions first.

- Avoid high-turnover funds and stocks as they generate commissions, transaction costs, and higher tax liabilities.

- Use tax-managed funds to minimize year-end distributions of capital gains.

- Harvest your losses and use them to offset gains.