Full retirement age (FRA) is a critical concept in U.S. law, specifically within the Social Security system, as it determines the age at which individuals can receive their full, unreduced retirement benefits. Established by the Social Security Act, FRA varies depending on the year of birth, ranging from 65 for those born in 1937 or earlier to 67 for those born in 1960 or later. Claiming benefits before reaching FRA results in permanently reduced monthly payments, while delaying benefits beyond FRA can increase payments up to age 70. Understanding FRA is essential for financial planning, as it directly impacts the amount of Social Security income retirees can expect and influences decisions about when to retire and how to maximize benefits under the law.

| Characteristics | Values |

|---|---|

| Definition | The age at which an individual is eligible to receive full Social Security retirement benefits without any reduction. |

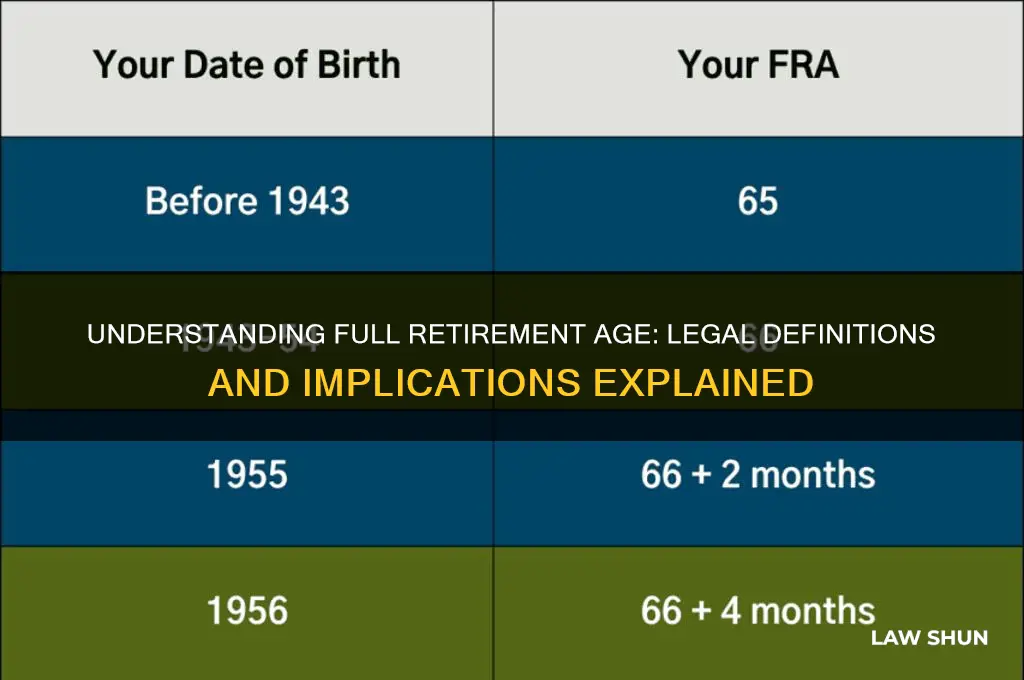

| Current Full Retirement Age (FRA) | 66 years and 2 months for individuals born in 1955. Increases gradually to 67 years for those born in 1960 or later. |

| Early Retirement | Can start receiving benefits as early as age 62, but benefits will be reduced permanently. |

| Delayed Retirement | Can delay receiving benefits until age 70, resulting in increased monthly benefits (up to 8% per year). |

| Benefit Calculation | Based on the highest 35 years of earnings, indexed for inflation. |

| Cost-of-Living Adjustments (COLAs) | Benefits are adjusted annually based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). |

| Taxation of Benefits | Up to 85% of Social Security benefits may be taxable, depending on provisional income. |

| Spousal Benefits | Spouses may be eligible for benefits based on their partner's work record, even if they have little or no earnings history. |

| Survivor Benefits | Surviving spouses may be eligible for benefits based on their deceased partner's work record. |

| Work and Benefits | Earnings above certain limits can reduce benefits if claimed before FRA. No reduction after FRA. |

| Medicare Eligibility | Automatically enrolled in Medicare Part A at age 65, regardless of whether Social Security benefits are claimed. |

| Source | Social Security Administration (SSA), Internal Revenue Service (IRS), and relevant federal laws. |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UY218_.jpg)

What You'll Learn

- Social Security Benefits: Full retirement age determines when to receive full Social Security benefits

- Legal Definitions: Laws define full retirement age for eligibility in various programs

- Age Variations: Full retirement age differs by birth year under federal law

- Early vs. Late: Legal implications of retiring before or after full retirement age

- Pension Plans: Full retirement age affects pension payouts and tax considerations

![]()

Social Security Benefits: Full retirement age determines when to receive full Social Security benefits

The full retirement age (FRA) is a pivotal concept in U.S. Social Security law, dictating when individuals can claim their full, unreduced retirement benefits. Currently, FRA ranges from 66 to 67 years old, depending on the year of birth. For example, if you were born in 1960 or later, your FRA is 67. Understanding this age is crucial because claiming benefits before reaching FRA results in permanently reduced monthly payments, while delaying benefits beyond FRA increases them, up to age 70.

Consider the financial implications of this timing. If your FRA is 67 and you claim benefits at 62, your monthly payment could be reduced by as much as 30%. Conversely, waiting until 70 could increase your benefit by up to 24% compared to your FRA amount. This decision should align with your health, savings, and employment status. For instance, if you’re in good health and have sufficient savings, delaying benefits could maximize your lifetime income.

The FRA also interacts with other Social Security rules, such as the earnings test. If you claim benefits before FRA and continue working, your benefits may be temporarily reduced if your earnings exceed certain limits ($21,240 in 2023). However, these withheld amounts are added back into your benefit once you reach FRA. This underscores the importance of coordinating your retirement plans with your FRA to avoid unintended penalties.

For married couples, FRA considerations extend to spousal and survivor benefits. A spouse can claim benefits based on the higher-earning partner’s record, but the amount received depends on when the lower-earning spouse files. If both spouses delay claiming until their respective FRAs or later, it can significantly enhance their combined lifetime benefits. Strategic planning around FRA can thus optimize Social Security income for both partners.

In summary, the full retirement age is not just a number but a critical factor in maximizing Social Security benefits. Whether you choose to claim early, at FRA, or later depends on your individual circumstances. By understanding how FRA impacts benefit amounts, interacts with other rules, and affects spousal benefits, you can make informed decisions that align with your long-term financial goals.

Unpopular Legal Realities: Laws That Divide Public Opinion

You may want to see also

Explore related products

![]()

Legal Definitions: Laws define full retirement age for eligibility in various programs

In the United States, the Social Security Act defines full retirement age (FRA) as the age at which individuals become eligible to receive full retirement benefits without any reductions. Currently, FRA ranges from 66 to 67 years, depending on the year of birth. For example, individuals born in 1960 or later must wait until age 67 to claim full benefits, while those born in 1954 can claim them at 66. This age threshold is not arbitrary; it is a legal benchmark that determines eligibility for Social Security benefits, ensuring that recipients receive the full amount they have earned through payroll taxes. Understanding FRA is crucial for financial planning, as claiming benefits before reaching this age results in permanently reduced monthly payments.

Beyond Social Security, FRA plays a pivotal role in other legal programs, such as Medicare eligibility. While Medicare eligibility begins at age 65, FRA influences the timing of enrollment in certain parts of the program, particularly for those who delay retirement. For instance, individuals who continue working past 65 and have employer-sponsored health insurance may delay enrolling in Medicare Part B without penalties until they retire or lose their employer coverage. This intersection of FRA and Medicare highlights how legal definitions of retirement age cascade into broader eligibility criteria for federal programs, impacting healthcare access and financial decisions.

Internationally, legal definitions of full retirement age vary widely, reflecting differing societal norms and economic conditions. In France, for example, the FRA is 62, though it is gradually increasing to 64 under recent reforms. In contrast, Japan has raised its FRA to 65, aligning with its aging population and labor market needs. These variations underscore the importance of understanding FRA within its specific legal and cultural context. For expatriates or individuals planning to retire abroad, knowing the FRA in their destination country is essential for accessing pensions, healthcare, and other benefits.

From a practical standpoint, individuals must strategically plan around FRA to maximize their retirement benefits. For example, delaying Social Security benefits beyond FRA can increase monthly payments by up to 8% per year until age 70, a strategy known as "delayed retirement credits." Conversely, claiming benefits early reduces them permanently. Legal definitions of FRA also impact spousal and survivor benefits, as eligibility rules differ based on the claimant’s age relative to FRA. Consulting with a financial advisor or using online calculators can help individuals navigate these complexities and make informed decisions aligned with their retirement goals.

In conclusion, the legal definition of full retirement age serves as a cornerstone for eligibility in programs like Social Security and Medicare, with far-reaching implications for financial and healthcare planning. Whether in the U.S. or abroad, understanding FRA is essential for optimizing retirement benefits and ensuring a secure post-work life. By staying informed about these legal benchmarks and their nuances, individuals can better prepare for the transition into retirement, avoiding pitfalls and capitalizing on opportunities to enhance their financial well-being.

Southern Laws: Empowering or Failing Freedmen Post-Emancipation?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

![]()

Age Variations: Full retirement age differs by birth year under federal law

The concept of full retirement age (FRA) is not a one-size-fits-all figure but a dynamic threshold that shifts based on the year of your birth. This variation is a critical aspect of federal law, particularly within the Social Security system, designed to adapt to changing demographics and economic conditions. For instance, individuals born in 1937 or earlier reach full retirement age at 65, while those born in 1960 or later must wait until 67. This gradual increase reflects longer life expectancies and aims to sustain the solvency of Social Security funds. Understanding these age variations is essential for anyone planning their retirement, as it directly impacts benefit amounts and eligibility for other programs like Medicare.

To illustrate, consider two individuals: one born in 1955 and another in 1965. The former reaches FRA at 66 and 2 months, while the latter must wait until 67. If both claim Social Security benefits before their respective FRAs, they face permanent reductions in monthly payments. For example, starting benefits at age 62—the earliest eligibility age—can reduce payments by up to 30% for the 1965-born individual. Conversely, delaying benefits past FRA increases payments by 8% per year up to age 70, a strategy that can significantly enhance financial security in retirement. These calculations underscore the importance of aligning retirement plans with your specific FRA.

From a practical standpoint, knowing your FRA allows you to optimize Social Security benefits and coordinate other retirement income sources. For instance, if your FRA is 67 but you plan to retire at 65, you might need to rely more heavily on personal savings or pensions during the interim. Additionally, FRA affects Medicare enrollment, as most people become eligible for Medicare at age 65, regardless of their FRA. Failing to enroll in Medicare Part B at 65, unless covered by an employer’s group health plan, can result in late enrollment penalties. Thus, FRA is not just about Social Security—it’s a cornerstone of comprehensive retirement planning.

A comparative analysis reveals the policy rationale behind FRA variations. When Social Security was established in 1935, FRA was set at 65, reflecting average life expectancies of around 60 years. As life expectancies rose and the workforce aged, Congress incrementally raised FRA to ensure the program’s sustainability. This approach balances the need to provide adequate retirement income with the fiscal constraints of a growing beneficiary population. Critics argue that the increase disproportionately affects lower-income workers with physically demanding jobs, who may struggle to work longer. Proponents counter that the change is necessary to prevent benefit cuts or tax increases for future generations.

In conclusion, FRA is a personalized milestone that demands careful consideration in retirement planning. By understanding how your birth year determines this age, you can make informed decisions about when to claim benefits, how to structure your finances, and how to navigate related programs like Medicare. Tools such as the Social Security Administration’s online calculator can help you determine your FRA and estimate benefits based on your earnings history. Ultimately, recognizing the significance of FRA variations empowers you to retire on your terms, with financial security and peace of mind.

Landlord-Tenant Disputes: Understanding the Legal Category of Rental Law

You may want to see also

Explore related products

![]()

Early vs. Late: Legal implications of retiring before or after full retirement age

Retiring before or after full retirement age (FRA) carries distinct legal implications that affect Social Security benefits, healthcare coverage, and tax obligations. FRA, currently set between 66 and 67 depending on birth year, is the age at which individuals can claim full, unreduced Social Security retirement benefits. Retiring before FRA reduces monthly benefits permanently, while delaying retirement beyond FRA increases them, up to age 70. For example, retiring at 62—the earliest eligibility age—can reduce benefits by up to 30%, whereas waiting until 70 can increase them by up to 24% compared to FRA. Understanding these trade-offs is critical for financial planning.

One key legal consideration is the impact on Medicare eligibility. While Medicare coverage begins at age 65, retiring before this age can create a gap in healthcare coverage if employer-sponsored insurance ends. Early retirees must either purchase private insurance or pay penalties for delayed Medicare enrollment. Conversely, delaying retirement beyond 65 allows individuals to continue employer-sponsored coverage, potentially deferring Medicare Part B enrollment without penalty. This decision requires careful evaluation of costs and coverage needs.

Tax implications also differ based on retirement timing. Early retirees may face higher taxes on Social Security benefits if they have substantial income from other sources, such as investments or part-time work. The IRS uses a formula to determine how much of Social Security is taxable, with up to 85% subject to tax for higher earners. Delaying retirement can reduce taxable income in early years, as individuals may rely more on tax-advantaged retirement accounts like 401(k)s or IRAs, which offer controlled tax exposure through required minimum distributions (RMDs) starting at age 73.

Another legal consideration is the impact on spousal and survivor benefits. Retiring early reduces not only individual benefits but also those available to spouses or survivors. For example, a spouse’s benefit is based on the higher-earning partner’s record, and retiring early lowers this amount permanently. Delaying retirement, however, maximizes these benefits, providing greater financial security for surviving spouses. This is particularly important for households relying on a single earner’s record.

Finally, early retirement can trigger penalties for accessing retirement savings before age 59½. Withdrawals from tax-deferred accounts like 401(k)s or traditional IRAs before this age typically incur a 10% early withdrawal penalty, in addition to income tax. Retiring after FRA allows individuals to delay tapping into these accounts, preserving their value and avoiding penalties. Strategic planning, such as using Health Savings Accounts (HSAs) or Roth IRAs, can mitigate these risks for early retirees.

In summary, retiring before or after FRA involves navigating a complex web of legal and financial consequences. Early retirement offers immediate freedom but reduces benefits and increases costs, while delaying retirement maximizes benefits and minimizes penalties. Careful consideration of these factors is essential to ensure a secure and sustainable retirement.

Understanding Legal Definitions: What Constitutes a Seizure Under the Law?

You may want to see also

Explore related products

![]()

Pension Plans: Full retirement age affects pension payouts and tax considerations

Full retirement age (FRA) is a pivotal concept in pension planning, dictating when individuals can claim their full Social Security benefits without penalties. Currently, FRA ranges from 66 to 67 years, depending on birth year. For instance, those born in 1960 or later must wait until 67 to receive their full benefit amount. This age threshold directly impacts pension payouts, as claiming benefits before FRA reduces monthly payments, while delaying claims beyond FRA increases them, up to age 70. Understanding this timeline is crucial for maximizing retirement income.

Pension plans often intertwine with Social Security benefits, creating a complex web of financial decisions. For example, if you retire early at 62, your Social Security benefit could be permanently reduced by up to 30%, depending on your FRA. Conversely, delaying retirement benefits by four years beyond FRA can increase payouts by 8% annually, a strategy particularly beneficial for those with longevity in their family history. Employers’ pension plans may also offer different payout structures based on retirement age, further complicating the decision-making process.

Tax considerations add another layer of complexity to retirement planning. Withdrawing from pension plans before age 59½ typically incurs a 10% early withdrawal penalty, in addition to regular income tax. However, once you reach FRA, required minimum distributions (RMDs) from tax-deferred retirement accounts like 401(k)s and traditional IRAs kick in, usually by age 73. These distributions are taxed as ordinary income, potentially pushing retirees into higher tax brackets. Strategically timing pension withdrawals and Social Security claims can mitigate tax liabilities and preserve more of your hard-earned savings.

A practical tip for retirees is to coordinate pension plan distributions with other income sources to stay within lower tax brackets. For example, if you’re 66 with an FRA of 66, consider claiming Social Security while delaying pension withdrawals until the following year to avoid a spike in taxable income. Additionally, Roth IRA conversions before FRA can reduce future RMDs and tax burdens, as Roth accounts are not subject to RMDs during the owner’s lifetime. Consulting a financial advisor to model these scenarios can provide clarity and optimize your retirement strategy.

In conclusion, full retirement age is not just a milestone but a critical factor in pension planning. It influences the size of your Social Security checks, the timing of pension withdrawals, and your overall tax obligations. By aligning your retirement age with FRA and strategically managing distributions, you can enhance your financial security and enjoy a more comfortable retirement. Ignoring these nuances could result in reduced benefits and higher taxes, underscoring the importance of informed decision-making in this phase of life.

Understanding the Essential Sections of a Legal Memo of Law

You may want to see also

Frequently asked questions

Full Retirement Age (FRA) is the age at which individuals are eligible to receive full Social Security retirement benefits, as defined by the Social Security Act. It varies based on the year of birth, ranging from 66 to 67 years old.

Full Retirement Age is determined by the year of birth, as outlined in the Social Security Act. For example, individuals born in 1960 or later have an FRA of 67, while those born in 1954 have an FRA of 66 years and 2 months.

Yes, benefits can be claimed as early as age 62, but they will be permanently reduced. Claiming before FRA results in lower monthly payments compared to waiting until FRA or later.

Delaying benefits beyond FRA increases monthly payments through delayed retirement credits, up to age 70. This results in higher lifetime benefits for those who live longer.

Yes, FRA also applies to spousal and survivor benefits. Claiming these benefits before FRA reduces the amount received, while delaying can increase payments, similar to individual retirement benefits.