Marriage comes with a host of tax implications, and understanding the benefits of marriage and potential tax implications is key to choosing the best filing option. Married couples can choose to file their federal income taxes jointly or separately each year, with most couples benefiting from filing jointly. Marriage can offer notable tax advantages for estate planning and real estate transactions, and spouses can give unlimited gifts of cash or other property to one another without incurring gift taxes. Additionally, couples can combine benefits and credits to save on taxes, and certain benefits are more lenient for married couples. However, a marriage penalty can occur when two individuals filing jointly pay more tax than if they had filed as single taxpayers. Newlyweds should also be aware of the paperwork required after marriage, such as reporting name and address changes to the relevant authorities.

| Characteristics | Values |

|---|---|

| Filing options | Married couples can choose to file their federal income taxes jointly or separately each year. |

| Tax credits | Married couples are eligible for various tax credits, such as the Earned Income Tax Credit (EITC) and the Child and Dependent Care Credit (CDCC). |

| Tax liability | The above-mentioned tax credits directly diminish tax liability, providing substantial benefits. |

| Income threshold | The income threshold for the EITC is more lenient for married couples than for single filers. |

| Child tax credit | Married couples can earn up to twice as much as single filers before the child tax credit begins to phase out. |

| Medical expenses | If either spouse has incurred substantial medical expenses, filing separately may facilitate the meeting of the 7.5% Adjusted Gross Income (AGI) threshold for qualified medical expenses. |

| Tax advantages | Marriage can offer notable tax advantages for estate planning and real estate transactions. |

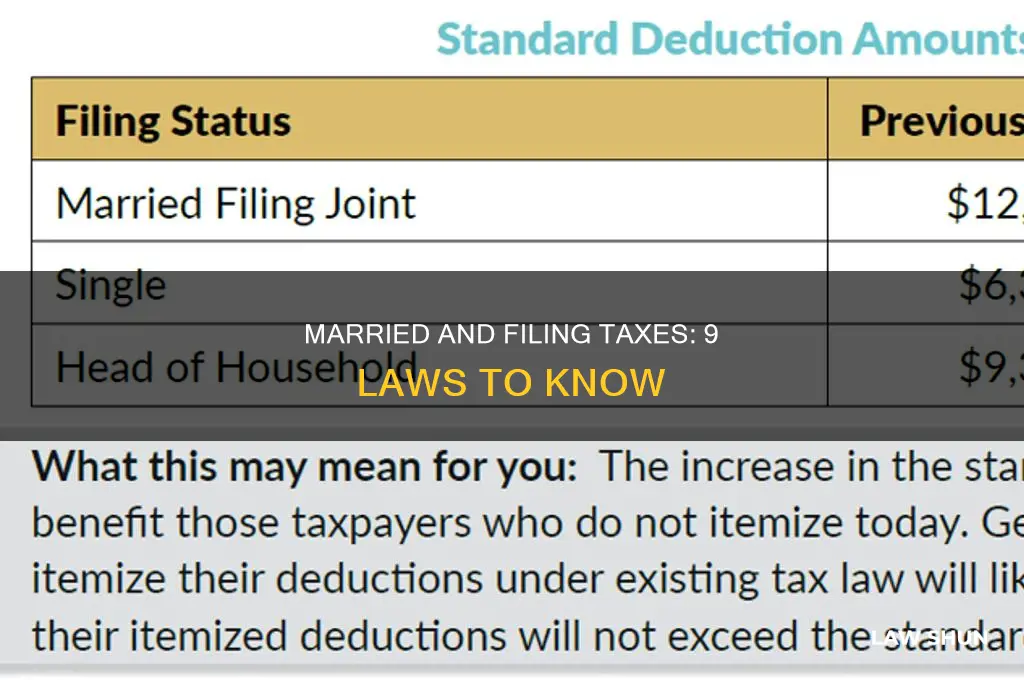

| Tax deductions | For the 2025 tax year, the standard deduction for married couples filing jointly is $30,000. |

| Tax penalties | The Tax Cuts and Jobs Act of 2017 eliminated the "marriage penalty" for most taxpayers by changing the income ranges for the tax brackets for married couples filing jointly. |

| Name changes | People who change their name after marriage should report it to the Social Security Administration as soon as possible. |

| Address changes | If marriage results in a change of address, the IRS and U.S. Postal Service must be notified. |

| Gift taxes | Spouses can give unlimited gifts of cash or other property to one another without incurring gift taxes. |

| Community property | Nine states (Wisconsin, Washington, Texas, New Mexico, Nevada, Louisiana, Idaho, California, and Arizona) have community property statutes that affect married couples. |

Explore related products

What You'll Learn

![]()

Married couples can file taxes jointly or separately

Marriage comes with a host of tax implications, and one of the most significant choices married couples face is whether to file their taxes jointly or separately. This decision can have a substantial impact on the tax credits and deductions they qualify for. While filing jointly is often more advantageous, there are exceptions, and it's essential for couples to review their specific situation.

When a couple files taxes jointly, they report all income from all assets. This includes income from separate property, such as dividends on stock owned prior to the marriage, which some states consider to be separate income reported only by the individual spouse. However, states like Wisconsin, Louisiana, Idaho, and Texas consider income earned from separate property to be shared equally by both spouses. Filing jointly offers a higher standard deduction, which, for the 2025 tax year, is $30,000 for married couples. Additionally, certain tax credits, such as the Earned Income Tax Credit (EITC) and the Child and Dependent Care Credit (CDCC), have more lenient income thresholds for married couples filing jointly.

On the other hand, filing taxes separately may be more beneficial in certain situations. For example, if either spouse has incurred substantial medical expenses in a tax year, filing separately may make it easier to meet the 7.5% Adjusted Gross Income (AGI) threshold for qualified medical expenses. Additionally, in the case of high earners, filing separately may allow for a lower tax bill by maximizing potential tax deductions and credits available to each individual.

The decision to file jointly or separately also depends on other factors, such as whether the couple lives in a community property state. In these states, income and assets are generally considered shared equally between spouses. However, it's important to note that each state has its own specific laws regarding the distinction between shared and separate income and assets, and these laws should be understood when preparing tax returns.

To make an informed decision, couples should prepare their tax returns both ways, carefully reviewing the calculations and considering their unique circumstances. This will help them determine which filing status results in the greatest tax savings for their particular situation.

Antitrust Laws: Sherman's Legacy

You may want to see also

Explore related products

![]()

Marriage can reduce tax liability

Marriage can bring about significant changes in one's tax filing options and liability. While the tax benefits of marriage vary depending on individual circumstances, there are some ways in which tying the knot can reduce tax liability.

Firstly, married couples have the option to file their federal income taxes jointly or separately each year. While filing jointly is usually more advantageous, there are exceptions. For instance, if either spouse incurs substantial medical expenses in a tax year, filing separately may allow them to meet the 7.5% Adjusted Gross Income (AGI) threshold for qualified medical expenses.

Married couples can also combine benefits and credits to save on taxes. They are eligible for various tax credits, such as the Earned Income Tax Credit (EITC) and the Child and Dependent Care Credit (CDCC), which directly reduce tax liability. The income threshold for the EITC is more lenient for married couples, and in the case of the child tax credit, married couples can earn up to twice as much as single filers before the credit starts to phase out.

Marriage can also offer notable tax advantages for estate planning and real estate transactions. Spouses can give unlimited gifts of cash or other property to each other without incurring gift taxes, which has important implications for estate planning. Additionally, when it comes to inheriting an IRA, spouses have a special rule that may allow them to defer distributions and pay less tax on the distribution if they are in a lower-income tax bracket at the time.

Furthermore, as a married couple, contributions to a Health Savings Account (HSA) can be doubled if one spouse has a high-deductible health plan (HDHP). This effectively doubles the tax savings compared to single filers.

It is important to note that while marriage can provide tax advantages, there is also a potential ""marriage penalty"" where a couple filing jointly may pay more tax than they would have as single filers. This occurs because the income tax brackets and standard deductions for married couples filing jointly are not always double that of single filers. However, under current law, this penalty has been partly alleviated in the lower income tax brackets.

Laws vs Regulations: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Tax benefits of marriage

Marriage can bring about a change in your tax situation. There are several tax benefits to being married, which can result in notable tax savings.

Firstly, married couples can choose to file their federal income taxes jointly or separately. In most cases, filing jointly is more beneficial, as it can reduce the overall tax bill. For the 2025 tax year, the standard deduction for married couples filing jointly is $30,000. However, each couple should review their own situation, as there are exceptions. For instance, if either spouse has incurred substantial medical expenses, filing separately may facilitate meeting the 7.5% Adjusted Gross Income (AGI) threshold for qualified medical expenses.

Married couples are also eligible for various tax credits, such as the Earned Income Tax Credit (EITC) and the Child and Dependent Care Credit (CDCC). These credits directly reduce tax liability, providing substantial benefits. The income threshold for the EITC is more lenient for married couples, and in the case of the child tax credit, married couples can earn up to twice as much as single filers before the credit starts to phase out.

Additionally, marriage offers tax advantages for estate planning and real estate transactions. Spouses can give unlimited gifts of cash or other property to each other without incurring gift taxes. Furthermore, any property that passes to a spouse when their partner dies is exempt from federal estate tax.

Marriage can also provide retirement savings advantages. A non-working spouse can contribute to an Individual Retirement Account (IRA) using joint income, which is not an option for single non-working individuals.

While there are many tax benefits to marriage, it is important to note that there can also be drawbacks, such as the "marriage penalty," where a married couple may fall into a higher tax bracket than when they were single, resulting in a higher tax rate.

Contract Breach: Law or Fact?

You may want to see also

Explore related products

![]()

Tax implications of marriage

Marriage has a significant impact on a couple's finances, particularly when it comes to filing taxes. There are several tax implications that newlyweds should be aware of and consider when planning their financial future.

Firstly, it is important to understand the difference between filing taxes jointly and separately. Married couples have the option to file their federal income taxes jointly or separately each year. For most couples, filing jointly is more advantageous as it often results in a lower overall tax bill. This is because, when filing jointly, married couples can combine benefits and credits to save on taxes. Additionally, the standard deduction for married couples filing jointly is typically double that of single individuals, which can further reduce their taxable income. However, there are exceptions to this rule. For example, if one spouse incurs substantial medical expenses in a tax year, filing separately may make it easier to meet the 7.5% Adjusted Gross Income (AGI) threshold for qualified medical expenses. To make an informed decision, couples should prepare their tax returns both ways and choose the option that results in the greatest tax savings.

Another important consideration is the impact of marriage on tax credits and deductions. Married couples become eligible for various tax credits, such as the Earned Income Tax Credit (EITC) and the Child and Dependent Care Credit (CDCC). These credits directly reduce tax liability and provide substantial financial benefits. Additionally, the income threshold for certain credits, such as the EITC, is more lenient for married couples than for single filers. Furthermore, marriage can offer notable tax advantages for estate planning and real estate transactions. Spouses can make unlimited gifts of cash or other property to each other without incurring gift taxes, and they may benefit from extended capital gains provisions when inheriting an IRA or other assets.

It is worth noting that while marriage often results in tax savings for couples, there is a phenomenon known as the "marriage penalty" where high-income earners may face a higher tax burden after getting married. This occurs when the tax liability of a married couple filing jointly is greater than the sum of their individual tax liabilities as if they were single. However, the Tax Cuts and Jobs Act of 2017 alleviated this penalty for most taxpayers by adjusting the income ranges for the tax brackets for married couples filing jointly.

Lastly, marriage also brings about some administrative changes related to taxes. Newlyweds should ensure that any name changes are reported to the Social Security Administration (SSA) and that their employers are notified of their new marital status. Additionally, if the marriage results in a change of address, the Internal Revenue Service (IRS) and the postal service should be informed to avoid delays in receiving any tax-related correspondence.

Laws of the 1920s: A Decade of Change

You may want to see also

Explore related products

![]()

Community property laws and marriage

Marriage has a significant impact on taxes, with various tax credits and benefits available to married couples. In the United States, there are nine community property law states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. Four other states have optional community property systems. These laws define how property and assets are owned and divided between spouses during marriage and in the event of divorce or death.

Community property laws consider any income, real estate, or personal property acquired by either spouse during the marriage to be jointly owned by both partners. This means that spouses own and owe everything equally, regardless of who earns or spends the income. For example, an Individual Retirement Account (IRA) in the name of one spouse, accumulated during the marriage, would typically be considered community property. Similarly, debts incurred during the marriage are generally the responsibility of both spouses.

In community property states, spouses have equal power to manage the estate independently. However, certain major transactions or decisions may require the consent of both spouses. Additionally, in the case of divorce, property acquired during the marriage is subject to division between the spouses. This division may be a 50/50 split, as mandated by statute in states like California, or an "equitable distribution," which may result in an unequal division, as seen in Texas.

It is important to note that property owned by one spouse before the marriage, as well as gifts and inheritances received during the marriage, are generally treated as separate property and are not subject to division in the same way as community property. In some cases, separate property can be voluntarily transformed into community property or included in the marital estate for reasons of equity. Additionally, if there are children from a prior marriage, the property associated with that marriage may be segregated from the community property of the subsequent marriage to ensure the children's inheritance rights.

Community property laws also have implications for estate planning and beneficiary designations. For example, in community property states, the spouse of the owner of a retirement account is typically the primary beneficiary unless they provide written consent for someone else to be named. Understanding these laws can help spouses make informed decisions about their finances and estate planning.

The First Legal Mind: Who Wrote the First Laws?

You may want to see also

Frequently asked questions

Marriage can offer notable tax advantages for estate planning and real estate transactions. Spouses can give unlimited gifts of cash or other property to one another without gift taxes. Married couples can also combine benefits and credits to save on taxes.

Married couples can choose to file their federal income taxes jointly or separately each year. If you were married on December 31, you are considered married for tax purposes for the whole year. Filing jointly is typically more advantageous, but there are exceptions.

If you change your name after marriage, you must report it to the Social Security Administration as soon as possible. The name on your tax return must match what is on file at the SSA.

In California, Nevada, and Washington, community property law extends to same-sex registered domestic partners (RDPs). However, they must file separate federal income tax returns as "Head of Household" or "Single" and include their separate and community income.

Couples in a legally-recognized common-law marriage in the state where it began can choose a married filing status.