As of July 2025, the newest gas tax law is the One Big Beautiful Bill Act (OBBBA). This legislation includes several provisions that may benefit the oil and gas industry. For example, it restores the ability to deduct domestic research and experimental expenditures. Additionally, the OBBBA increases the first-year bonus depreciation allowance and makes it permanent. While the new law may have benefits, not everyone is happy about it, as it also includes certain tax and fee hikes.

| Characteristics | Values |

|---|---|

| Name of the Law | One Big Beautiful Bill Act (OBBBA) |

| Date of Enactment | July 4, 2025 |

| Key Provisions | Restores the ability to deduct domestic research and experimental expenditures, increases the first-year bonus depreciation allowance, provides retroactive relief for certain R&E costs, mandates expanded leasing on federal lands and waters, delays the Methane Waste Emission Charge |

| State-wise Gas Tax Changes | Washington, California, New York, Florida, Georgia, Maryland, Illinois, Connecticut, Alaska, Arkansas, Missouri |

| Impact | May benefit the oil and gas industry, mixed reactions from the public and politicians |

Explore related products

What You'll Learn

![]()

Gas tax increases in California, Connecticut, Illinois, Mississippi, Missouri, Nebraska, and Washington

Gas taxes in California, Connecticut, Illinois, Mississippi, Missouri, Nebraska, and Washington have all seen recent changes, with most states implementing increases.

California's gas tax stands at 68.1 cents per gallon, the highest in the country. While there is no recent news of an increase, California's gas tax is subject to cap-and-trade carbon policies and low-carbon fuel standards, which can drive prices higher.

Connecticut's 25-cent-per-gallon gas tax was suspended in March 2022 due to rising oil prices caused by the Russian invasion of Ukraine. The tax was restored incrementally from January 1, 2023, with the state also imposing an 8.1% wholesale tax on fuel sold to local gas stations.

Illinois has the second-highest gas tax rate in the nation at 66.5 cents per gallon. While there is no recent news of an increase, Illinois' gas tax is also subject to cap-and-trade policies, which can impact prices.

Mississippi recently approved a bill to increase its gas tax from 18 cents per gallon to 21 cents per gallon starting on July 1, 2025. The tax will increase by three cents per gallon each year until it reaches 27 cents per gallon on July 1, 2027.

Missouri's motor fuel tax rate has seen incremental increases over the past few years. As of July 1, 2023, the rate was $0.0035 per gallon, and it will increase to $0.0038 per gallon on July 1, 2024, and $0.0042 per gallon on July 1, 2025.

Nebraska's fuel tax rate was 29.6 cents per gallon from July 1, 2024, through December 31, 2024. As of January 1, 2025, the rate increased to 30.4 cents per gallon.

Washington's CO2 tax added about 43 cents per gallon of gas in 2023, and prices are expected to increase further in 2024. The state will need to reduce emissions at double the rate of the Great Recession, which may impact gas prices.

Justice and Law: A Complex Relationship

You may want to see also

Explore related products

![]()

The One Big Beautiful Bill Act (OBBBA)

The OBBBA contains hundreds of provisions, including the permanent extension of individual tax rates that were set to expire at the end of 2025. It raises the cap on the state and local tax deduction to $40,000 for taxpayers earning less than $500,000, with the cap reverting to $10,000 after five years. The Act also introduces a series of smaller changes to the tax code, including new tax-deferred savings accounts, changes to rules related to the child tax credit and earned income tax credit, and a redesign of the excise tax on university endowment income. It makes expensing for investment in short-lived assets and domestic research and development permanent, eliminating a tax penalty for capital investment.

The OBBBA also has a significant impact on federal credits and deductions. It introduces a new deduction for individuals who receive qualified overtime compensation, allowing them to deduct pay that exceeds their regular rate and is reported on a Form W-2 or Form 1099. Additionally, it provides a new deduction for individuals aged 65 and older, allowing an additional deduction of up to $6,000 per eligible individual.

In terms of spending, the OBBBA includes significant allocations for defence, border enforcement, and deportations, totalling $150 billion each. It also increases funding for Immigration and Customs Enforcement (ICE) to over $100 billion by 2029, making it the most-funded law enforcement agency within the federal government. The Act also increases spending on crop insurance programs and disaster relief programs at the USDA.

The OBBBA has been criticised for phasing out some clean energy tax credits and promoting fossil fuels. It also includes a 12% cut to Medicaid spending and expands work requirements for SNAP benefits recipients.

Laws vs Amendments: Understanding the Distinction

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

Benefits to the oil and gas industry

The One Big Beautiful Bill Act (OBBBA), enacted on July 4, 2025, includes several provisions that benefit the oil and gas industry.

Firstly, the OBBBA restores the ability to deduct domestic research and experimental expenditures, with Section 174A allowing taxpayers to elect to capitalize and amortize domestic R&E expenditures over a period of 60 months or more. This provision also offers two forms of retroactive relief for previously capitalized R&E costs incurred between December 31, 2021, and January 1, 2025.

Secondly, the OBBBA increases the first-year bonus depreciation allowance under Section 168(k) to 100% for property acquired after January 19, 2025, and makes this allowance permanent. This is beneficial to the oil and gas industry as it allows for faster depreciation of assets, resulting in lower taxable income.

Thirdly, the OBBBA provides tax credits for carbon capture and storage technologies. The Section 45Q credit incentivizes the capture and storage or utilization of carbon oxide, offering an equal credit of $17 per metric ton base credit and $85 per metric ton when labor requirements are met. This credit increases to $36 per metric ton base credit and $180 per metric ton when labor requirements are met for direct air capture facilities.

Additionally, the OBBBA expands opportunities for the oil and gas industry to operate on federal lands and in federal waters, mandating quarterly onshore oil and gas lease sales in several states, including Wyoming, New Mexico, and Alaska. It also sets a primary term for deepwater leases and repeals royalties on methane produced on oil and gas leases on public lands and waters.

Furthermore, the OBBBA did not result in any changes to the favorable expensing provisions for intangible drilling costs (IDCs) and percentage depletion. IDCs, which typically represent 70-85% of the cost of a well, can be deducted 100% against taxable income in the first year, providing significant tax advantages for direct oil and gas investments. Percentage depletion, which is subject to certain limitations, allows a deduction of 15% of the well's annual production from income tax.

Overall, the OBBBA provides the oil and gas industry with expanded tax breaks, streamlined permitting, and increased predictability, which is expected to encourage development and investment in the sector.

How Coal Burning Confirms the First Law of Thermodynamics

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![]()

Tax relief for small businesses

While there doesn't appear to be one single new gas tax law that applies across the US, there are several new gas tax laws at the state level. For example, in Washington state, new laws have been introduced that raise the gas tax and hunting fees, while also providing immigrant workplace protections and tribal warrant frameworks for justice. In Minnesota, the Motor Fuel Tax increased on January 1, 2025, with a new combined rate of $0.318 per gallon, consisting of a $0.283 excise tax rate for gasoline and special fuel products, plus a $0.035 per gallon debt service surcharge.

In terms of tax relief for small businesses, the new tax law known as the One Big Beautiful Bill Act (OBBBA), enacted on July 4, 2025, offers some benefits. The OBBBA provides two forms of retroactive relief for previously capitalized R&E costs incurred after December 31, 2021, and before January 1, 2025. Small business taxpayers with average annual gross receipts not exceeding $31 million over the three years preceding the first tax year beginning after December 31, 2024, may apply the new expensing rules retroactively to those prior years.

Additionally, the OBBBA restores the ability to deduct domestic research and experimental expenditures. It also increases the first-year bonus depreciation allowance under Section 168(k) to 100% for property acquired after January 19, 2025, and makes the depreciation allowance permanent. Prior to the OBBBA, this allowance was scheduled to phase down to 40% in 2025, 20% in 2026, and disappear entirely by 2027.

Furthermore, the OBBBA provides that, for taxable years beginning after December 31, 2025, the computation of AFSI disregards the depletion expense related to intangible drilling and development costs (IDCs). This allows for the deduction of IDC costs under Section 263(c) to the extent deducted from taxable income. This change is favorable to the oil and gas industry, as it provides more opportunities for tax depreciation.

Administrative Law: How It's Created

You may want to see also

Explore related products

$13.9 $25

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)

![]()

Taxpayers' implementation issues

The newest gas tax law as of July 2025 is the One Big Beautiful Bill Act (OBBBA). While the OBBBA has provisions that may benefit the oil and gas industry, taxpayers face several implementation issues.

Firstly, taxpayers should begin modelling the effects of expensing versus continued capitalization and amortization. This will allow them to understand the impact of the new expensing rules, which small business taxpayers can apply retroactively for tax years beginning after December 31, 2024.

Secondly, with the OBBBA restoring the ability to deduct domestic research and experimental expenditures, taxpayers need to consider the timing of these deductions. They should assess whether it is more advantageous to deduct these costs immediately or amortize them over time.

Thirdly, the OBBBA's provision for computing the Alternative Minimum Tax (AMT) using the Adjusted Financial Statement Income (AFSI) will impact taxpayers with intangible drilling and development costs (IDCs). These taxpayers need to understand the interaction between the AFSI and IDC deductions to ensure accurate tax calculations.

Lastly, the delay in the Methane Waste Emission Charge until 2035 will provide temporary relief for oil and gas operators. However, taxpayers in this industry should start planning for the future impact of this charge on their operations and tax obligations.

Overall, while the OBBBA offers potential benefits to the oil and gas industry, taxpayers need to carefully navigate these implementation issues to ensure compliance and optimize their tax positions.

The Law-Making Power of Congress Explained

You may want to see also

Frequently asked questions

The One Big Beautiful Bill Act (OBBBA), enacted on July 4, 2025, is the newest gas tax law. It includes several provisions that benefit the oil and gas industry.

The OBBBA restores the ability to deduct domestic research and experimental expenditures. It also provides two forms of retroactive relief for certain R&E costs incurred between December 31, 2021, and January 1, 2025.

The OBBBA increases the first-year bonus depreciation allowance under Section 168(k) to 100% for property acquired after January 19, 2025, and makes this allowance permanent.

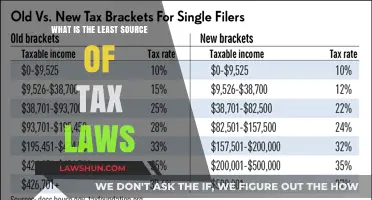

Yes, several states increased their fuel tax rates in 2023, including New York, Florida, Georgia, and Maryland. Additionally, Washington state recently raised its gas tax rates and diesel tax rates.

For taxable years starting after December 31, 2025, the OBBBA mandates that AFSI disregards the depletion expense related to intangible drilling and development costs (IDCs). These IDC costs can now be deducted under Section 263(c).