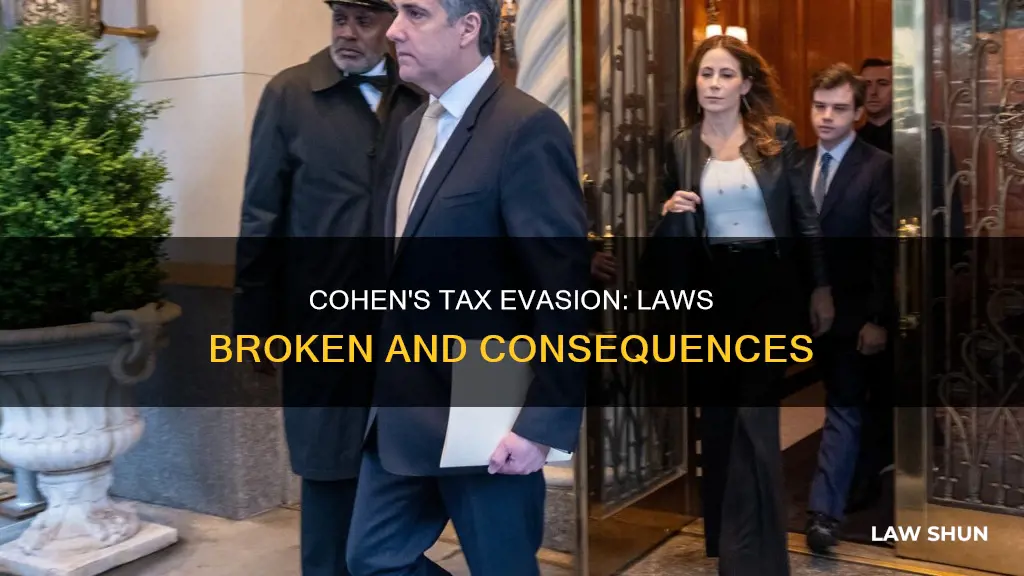

Michael Cohen, a lawyer and former right-hand man to Donald Trump, pleaded guilty in 2018 to eight counts of criminal activity, including tax evasion, making false statements to a federally-insured bank, and campaign finance violations. Cohen concealed more than $4 million in personal income from the IRS, made false statements to a federally-insured financial institution in connection with a $500,000 home equity loan, and, in 2016, caused $280,000 in payments to be made to silence two women who otherwise planned to speak publicly about their alleged affairs with a presidential candidate.

| Characteristics | Values |

|---|---|

| Tax evasion | Concealed more than $4 million in personal income from the IRS |

| Campaign finance violations | Made illegal payments to two women to keep them quiet about alleged affairs with a presidential candidate |

| Lying to a bank | Made false statements to a federally-insured financial institution in connection with a $500,000 home equity loan |

Explore related products

What You'll Learn

![]()

Tax evasion

To determine tax evasion, the agency must be able to show that the avoidance of taxes was willful on the part of the taxpayer. Tax evasion often entails the deliberate misrepresentation of the taxpayer's affairs to the tax authorities to reduce the taxpayer's tax liability. This includes dishonest tax reporting, declaring less income, profits or gains than the amounts actually earned, overstating deductions, bribing authorities and hiding money in secret locations.

Joe Arpaio's Legal Troubles: Broken Laws and Consequences

You may want to see also

Explore related products

![Historic Framed Print, Wanted for violation of federal income tax law [...], 17-7/8" x 21-7/8"](https://m.media-amazon.com/images/I/517JfmctvzL._AC_UY218_.jpg)

![]()

Making false statements to a federally-insured bank

Michael Cohen pleaded guilty to eight counts, including tax evasion, making false statements to a federally-insured bank, and campaign finance violations.

Cohen made false statements to a federally-insured financial institution in connection with a $500,000 home equity loan. He also concealed more than $4 million in personal income from the IRS.

Cohen's guilty plea was the result of an investigation by the FBI and IRS that uncovered crimes of fraud, deception, and evasion. The investigation found that Cohen had engaged in a string of financial transactions that were carefully constructed and concealed to protect a variety of interests.

Cohen's actions violated the tax laws that apply to everybody.

Trump's Legal Woes: What Laws Did He Break?

You may want to see also

Explore related products

![]()

Campaign finance violations

Michael Cohen pleaded guilty to eight counts, including tax evasion, making false statements to a federally-insured bank, and campaign finance violations.

Cohen caused $280,000 in payments to be made to silence two women who planned to speak publicly about their alleged affairs with a presidential candidate. Cohen, who spent years as one of Trump's right-hand men, said he acted "in coordination and at the direction of" Trump and in order to influence the 2016 presidential election in Trump's favour.

Trump has denied directing Cohen to break the law, claiming that Cohen was a lawyer and should have known the law. Trump has also claimed that he did nothing wrong and that the charges were cooked up to embarrass him.

Israeli Settlements: Breaking International Law?

You may want to see also

Explore related products

![]()

Lying to a bank

In 2018, Michael Cohen pleaded guilty in Manhattan Federal Court to eight counts, including criminal tax evasion, making false statements to a federally-insured bank, and campaign finance violations. Cohen concealed more than $4 million in personal income from the IRS, made false statements to a federally-insured financial institution in connection with a $500,000 home equity loan, and, in 2016, caused $280,000 in payments to be made to silence two women who otherwise planned to speak publicly about their alleged affairs with a presidential candidate. Cohen said he acted out of "blind loyalty to Donald Trump" and "felt it was my duty to cover up his dirty deeds".

Turkey's Spy Law Breach: Saudi Consulate Scandal

You may want to see also

Explore related products

![]()

Making illegal payments

Michael Cohen pleaded guilty to eight counts, including tax evasion, making false statements to a federally-insured bank, and campaign finance violations. He concealed more than $4 million in personal income from the IRS, made false statements to a federally-insured financial institution in connection with a $500,000 home equity loan, and, in 2016, caused payments to be made to silence two women who otherwise planned to speak publicly about their alleged affairs with a presidential candidate. Cohen said he acted out of "blind loyalty to Donald Trump" and "felt it was my duty to cover up his dirty deeds".

Cohen pleaded guilty to making illegal payments to two women who say they had sexual encounters with Trump, in order to keep them quiet about the alleged affairs. Cohen said he acted "in coordination and at the direction of" Trump and in order to influence the 2016 presidential election in Trump's favour.

Understanding North Carolina's Break Laws

You may want to see also

Frequently asked questions

Cohen broke tax evasion laws.

Cohen concealed more than $4 million in personal income from the IRS.

Cohen also made false statements to a federally-insured bank, and committed campaign finance violations.