The law of supply is a fundamental principle in economics that combines two key elements: price and quantity. It describes the direct relationship between the two, where an increase in price leads to an increase in the quantity supplied, assuming other factors remain constant. This law is derived from supply and demand equilibrium equations, reflecting the relationship between quantity demanded, quantity supplied, and price. The law of supply helps businesses understand the impact of price changes on their production and supply decisions, influencing their strategies to maximize profits. Factors such as production costs, market competition, government policies, and natural constraints can also influence supply decisions, showcasing the dynamic nature of the law of supply.

| Characteristics | Values |

|---|---|

| Relationship | Direct, positive relationship between price and quantity |

| Direction | As price increases, quantity supplied increases |

| Suppliers | Existing suppliers may increase production, new suppliers may enter the market |

| Profit | Higher prices incentivise suppliers to increase production to maximise profits |

| Competition | Competition between suppliers can influence supply |

| Technology | Investment in technology can increase quantity supplied |

| Government | Government policy and taxation can influence supply |

| Natural factors | Natural factors, such as weather, can influence supply |

Explore related products

What You'll Learn

![]()

The law of supply and demand

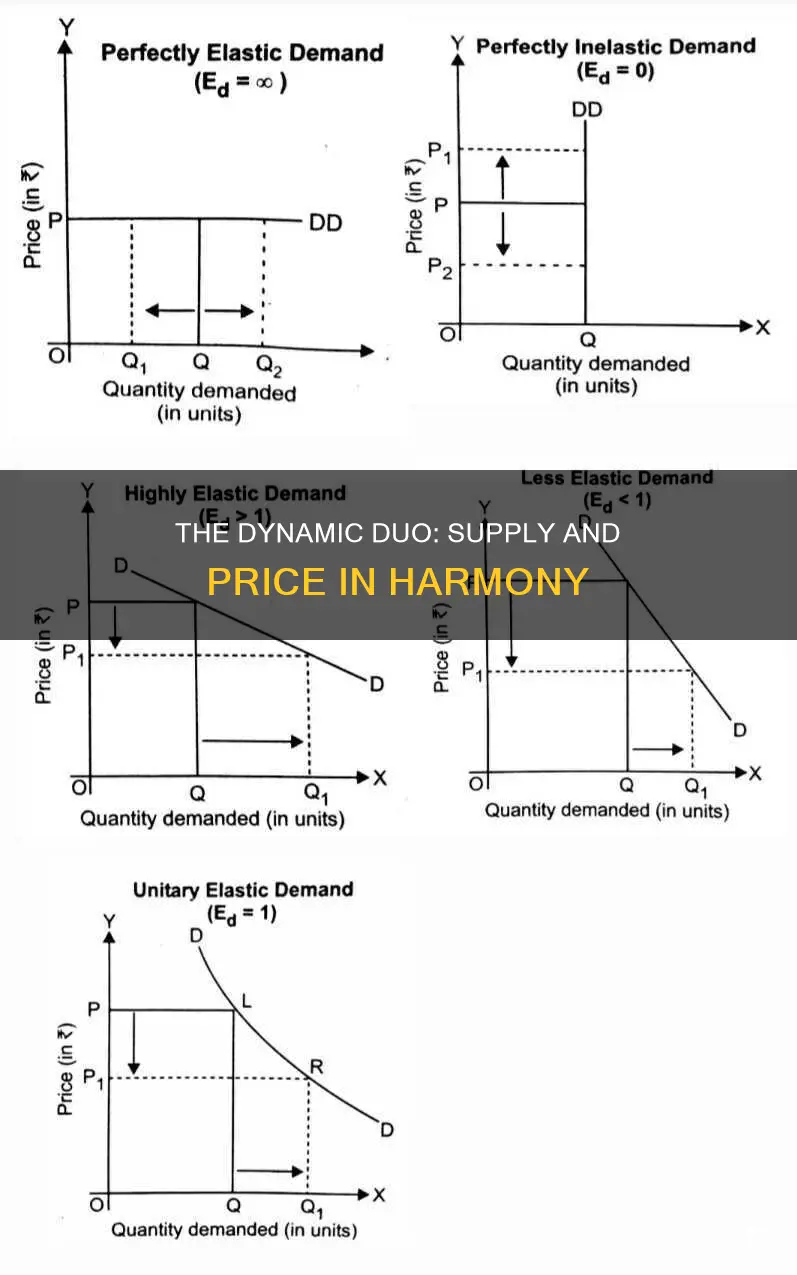

The law of supply is a fundamental principle of economic theory that states that, keeping other factors constant, an increase in sales price results in an increase in the quantity supplied. In other words, there is a direct relationship between price and quantity: quantities respond in the same direction as price changes. This means that producers and manufacturers are willing to offer more of a product for sale on the market at higher prices, as increasing production is a way of increasing profits. The law of supply is a positive relationship between quantity supplied and price, and is the reason for the upward slope of the supply curve.

The law of demand holds that demand for a product changes inversely to its price when all else is equal. The higher the price, the lower the level of demand. Buyers have finite resources, so their spending on a given product or commodity is limited as well. Demand rises as the product becomes more affordable.

Judicial Law-Making in Nazi Germany: A Historical Analysis

You may want to see also

Explore related products

![]()

The direct relationship between price and quantity

The law of supply is a fundamental principle of economic theory that describes the direct relationship between price and quantity. It states that, all other factors being equal, an increase in the sales price of a good or service will result in an increase in the quantity supplied, and vice versa. This relationship is often depicted using a supply curve, which slopes upward to reflect the direct correlation between quantity supplied (Q) and price (P).

The law of supply is based on the assumption that businesses seek to maximise their profits. When prices rise, businesses have an incentive to increase production to take advantage of the higher prices. This is because, with higher prices, businesses can make more money for each unit sold, even if it means selling a smaller total number of units. Therefore, they will try to sell a larger quantity of the product to maximise their profits.

On the other hand, when prices fall, businesses are disincentivised from producing as much. Lower prices result in a cost squeeze that curbs supply. This is because businesses will make less money for each unit sold, even if they can sell a larger total number of units. Therefore, they may choose to reduce production to cut their losses.

The law of supply also takes into account the number of suppliers in the market. As prices rise, new suppliers may enter the market, further increasing the overall supply. Similarly, if prices fall and profits decrease, some suppliers may leave the market, reducing the overall supply.

It's important to note that the law of supply assumes that all other factors remain constant. In reality, many other factors can impact supply decisions, including production costs, market competition, government policies, and technological advancements. These factors can influence the quantity supplied and cause deviations from the direct relationship between price and quantity predicted by the law of supply.

Overall, the law of supply is a useful concept for understanding how changes in price can affect the quantity supplied in a market. By recognising the direct relationship between price and quantity, businesses can make informed decisions about pricing and supply to maximise their profits.

The Law of Conservation: Who Established Momentum's Rule?

You may want to see also

Explore related products

![]()

The role of competition and market equilibrium

The law of supply and demand is a fundamental principle of economic theory that combines two central economic principles: the law of supply and the law of demand. These laws describe the relationship between price, supply, and demand. The law of supply states that as prices increase, so does the quantity supplied, assuming other factors such as production costs remain constant. This is because higher prices incentivize suppliers to increase production to maximize profits. Conversely, lower prices result in a cost squeeze that curbs supply.

The law of demand states that demand for a product changes inversely with price when all else is equal. In other words, the higher the price, the lower the level of demand, as buyers have finite resources.

Together, these laws interact to determine market equilibrium. Market equilibrium is the point at which the quantity supplied is equal to the quantity demanded. At this point, the market clears, and the price and quantity of the supply exactly match the demand. This can be visualized as the intersection of the supply and demand curves on a graph.

Competition plays a significant role in the law of supply. The number of competitors in a market can impact the quantity supplied and, consequently, market equilibrium. When there are more competitors in a market, the overall supply may increase. Additionally, competition can influence pricing decisions, as companies may be forced to cut prices to maintain their market share in the face of comparable alternatives.

Other factors that can influence the law of supply and market equilibrium include government policies, production costs, technological advancements, and, in certain industries such as agriculture, external factors like weather conditions.

In summary, the law of supply and demand, along with the role of competition and market equilibrium, are fundamental concepts in economics that govern the relationship between price, supply, and demand. These laws help market players understand and forecast future conditions, make business decisions, and determine pricing and supply strategies to maximize profits.

The US Lawmakers: Who Writes the Rules?

You may want to see also

Explore related products

![]()

The impact of production costs and government policy

The law of supply is a fundamental principle of economic theory that states that, assuming all other factors remain constant, an increase in sales price will result in an increase in the quantity supplied. This means that as prices rise, businesses will increase production to maximise profits.

Production costs are a key factor that can affect supply. If production costs, such as wages, decrease, manufacturers can produce more goods for the same price, so the quantity supplied will increase. Conversely, if production costs rise, this can cause a decrease in supply. For example, if a business faces rising costs for raw materials, it may not be able to afford to produce the same quantity of goods and may therefore reduce its output.

Government policy can also have a significant impact on production costs and, by extension, supply. Government subsidies, for instance, can encourage certain products by decreasing the overall cost of production. On the other hand, government taxation can cause the cost of production to rise, leading to a potential decrease in supply.

In addition to production costs and government policy, other factors that can influence supply include the number of suppliers, the level of competition, technology, and the presence of government support or restrictions. For example, investing in cutting-edge technology can enable businesses to produce goods or services more effectively, potentially resulting in an increase in the quantity supplied. Similarly, the availability of viable replacement items can impact the law of supply. If there are comparable alternatives to a product, companies may be forced to cut their prices to maintain their market share, which could result in an increase in the quantity supplied.

The EEOC's Founding Law Explained

You may want to see also

Explore related products

![]()

Exceptions to the law, including external factors

The law of supply is a fundamental economic theory that describes the positive relationship between price and quantity supplied of a commodity. It assumes that all other factors remain constant and that an increase in the price of a good or service will lead to an increase in the quantity of that good or service supplied by the market.

However, there are several exceptions to the law of supply, including various external factors that can influence supply decisions:

- Production costs: While the law of supply suggests that an increase in price will lead to an increase in supply, this relationship can be disrupted if production costs are also increasing. In this case, suppliers may be disincentivized to produce more, as their profits may be reduced due to higher costs.

- Market competition: In highly competitive markets, suppliers may not be able to increase their supply in response to higher prices, as they may not have the necessary resources or market power to do so.

- Availability of raw materials: If there is a shortage of raw materials or inputs, suppliers may not be able to increase their supply, even if prices rise.

- Government policies and regulations: Taxes, subsidies, and other government interventions can impact supply decisions. For example, changes in taxation laws can affect the profitability of supplying certain goods or services.

- Technology: Advancements in technology can impact the ability of suppliers to increase or decrease their supply. For example, investing in new technology can increase production efficiency and potentially increase the quantity supplied.

- Natural disasters: Unforeseen events, such as natural disasters, can disrupt supply chains and reduce the ability of suppliers to meet demand, regardless of price changes.

- Changes in resource availability: Scarcity of resources can limit output and supply, especially in economically underdeveloped countries.

- Precious, rare, or artistic items: The law of supply does not apply to items that are unique or in very limited supply, such as rare artwork or antiques. In these cases, an increase in price may not lead to an increase in supply, as the quantity of these items is fixed.

- Single supplier: When there is only one supplier of a good or service, they may have the market power to increase or decrease supply or pricing irrespective of external factors.

- Economies of scale: Large producers may be able to reduce production costs through economies of scale, allowing them to increase supply while keeping prices stable or even reducing them.

- Market focus and stock clearance: Businesses may temporarily increase the supply of certain products at low prices to eliminate remaining stock or raw materials when shifting their market focus.

These exceptions to the law of supply highlight the complexity of market dynamics and the importance of considering external factors when making business decisions. While the law of supply can be a useful guide, it is important to recognize that supply decisions are influenced by a multitude of factors that can vary across industries, markets, and specific business contexts.

The Judicial Branch: Law Creators or Interpreters?

You may want to see also

Frequently asked questions

The law of supply is a fundamental principle of economic theory that states that there is a direct relationship between price and quantity: quantities respond in the same direction as price changes.

The law of supply and the law of demand are two sides of the same coin, together forming the law of supply and demand. The law of demand states that demand for a product decreases as its price increases.

The supply curve is a graphical representation of the law of supply, showing the direct correlation between quantity supplied and price.

The number of suppliers, the level of competition, technology, government support or restrictions, and production costs can all influence the law of supply.

The law of supply can impact employment decisions, such as the number of hours an employee is willing to work, as well as the supply of qualified job applicants in a particular field.

![(Scarcity: The New Science of Having Less and How It Defines Our Lives) [By: Mullainathan, Sendhi] [Nov, 2014]](https://m.media-amazon.com/images/I/41yQA+6sSPL._AC_UY218_.jpg)