The Tax Cuts and Jobs Act (TCJA) was passed in 2017 and signed into law by President Donald Trump in 2018. It was the largest tax code overhaul in three decades, introducing significant changes to the tax code. The TCJA impacted individuals and businesses, particularly through tax cuts, and many of its provisions were set to expire in 2025. To address this, Congress passed the One Big Beautiful Bill in 2025, which extended most provisions of the TCJA and made some additional changes. This bill was touted as the largest tax cut in American history, providing tax relief to families, workers, small businesses, and manufacturers. However, critics argued that the TCJA was skewed towards the rich and failed to deliver promised economic benefits.

| Characteristics | Values |

|---|---|

| Name of the Tax Law | The Tax Cuts and Jobs Act (TCJA) |

| Year of Passing | 2017 |

| Type of Tax Law | Major overhaul of the tax code |

| Type of Reform | Tax cuts |

| Impact | Taxpayers and business owners |

| Corporate Tax Rate | 21% |

| Alternative Minimum Tax | Temporarily raised exemption amount and exemption phase-out threshold |

| Mortgage Interest Deduction | Lowered to $750,000 for married couples filing jointly |

| Pease Limitation | Repealed |

| Individual Tax Cuts | Expire after 2025 |

| Pass-Through Tax Cuts | Expire after 10 years |

| Corporate Tax Changes | Permanent |

| Estate Tax Exemption | Doubled to $22 million for wealthiest households |

| One Big Beautiful Bill (OBBB) | Passed in 2025 to extend TCJA provisions |

Explore related products

What You'll Learn

![]()

The 2017 Trump Tax Law

One of the key provisions of the TCJA was the reduction in the corporate tax rate from 35% to 21%, which was intended to give corporations financial relief, with the expectation that this would benefit employees and stimulate economic growth. This cut applied to all corporate income of at least $1 and was designed to benefit shareholders, who tend to be higher earners. Additionally, the TCJA introduced a 20% deduction for pass-through income, benefiting owners of pass-through businesses such as partnerships and sole proprietorships.

The TCJA also included changes to individual income taxes. It cut the top individual income tax rate from 39.6% to 37% for married couples with over $600,000 in taxable income. Initially, Trump's plan aimed to reduce the number of tax brackets from seven to four. However, the final version of the TCJA retained the seven brackets. Most of the individual tax cuts were set to expire in 2025, and there have been subsequent debates and efforts to extend them.

Another notable aspect of the 2017 Trump Tax Law was the elimination of the mandate requiring individuals to purchase health insurance. This change reversed a key provision of the Affordable Care Act. Additionally, the TCJA modified international tax provisions, increasing enforcement against foreign countries with discriminatory tax practices and adjusting how multinational corporations are taxed on base erosion payments.

Understanding the History of Payroll Taxes

You may want to see also

Explore related products

![]()

The One Big Beautiful Bill

The OBBB of 2025 includes legislation that prevents most of the tax laws from reverting to what they were in 2017, while also making some additional changes. These changes include no tax on tip or overtime income for certain workers, no tax on car loan interest, and tax relief for seniors. The bill also expands access to the child care credit, makes permanent the paid leave tax credit, and enhances the adoption tax credit. Additionally, it eliminates fraud and waste in Obamacare and blocks access to taxpayer-funded health benefits for illegal immigrants.

The bill is expected to have a significant impact on American families, workers, small businesses, and manufacturers. For example, the typical family will receive up to $10,900 in additional take-home pay, and workers will see increased wages of up to $7,200. It is estimated that up to 7.2 million jobs will be protected and created, with 1 million new jobs annually by small businesses.

However, there are concerns about the potential impact of the bill. Critics argue that the 2017 Trump tax law, which the OBBB extends, was skewed towards the rich and failed to deliver promised economic benefits. There are also worries that extending the expiring provisions of the TCJA will add $4.6 trillion in deficits over 10 years and boost inflationary pressures.

Overall, the One Big Beautiful Bill of 2025 is a significant piece of legislation that will have far-reaching effects on the American economy and its people.

Understanding Joint Venture Contracts: A Legal Guide

You may want to see also

Explore related products

$12.61 $25.99

$18.49 $19.95

![]()

The Tax Cuts and Jobs Act

The TCJA was expected to lower taxes by an average of $1,600 in 2018 and 2025, according to a 2017 report by the nonpartisan Tax Policy Center. However, the report also projected that the top 20% of Americans by income would receive about 65% of the tax savings. It was estimated that the bottom 80% of taxpayers (with incomes under $149,400) would receive 35% of the benefit in 2018, 34% in 2025, and none of the benefit in 2027. Additionally, 72% of taxpayers would be adversely impacted if the tax cuts were financed by spending cuts outside the legislation, as these cuts would predominantly affect lower- to middle-income earners.

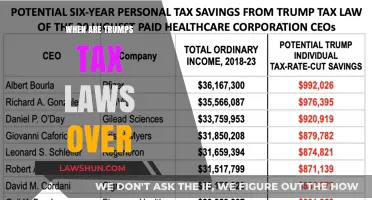

The TCJA simplified the tax code for some but not all, lowered corporate debt, and led to a temporary increase in investment before a decline. It also brought money back from overseas without stimulating business activity. In 2018, more than 90 Fortune 500 companies paid an effective federal tax rate of 0% or less, and major firms did not alter their hiring practices or investment strategies significantly in response to the tax cuts. Instead, they directed most of the savings to shareholders and debt repayment rather than new capital expenditures or research and development.

The 2017 Act was criticised as being skewed towards the rich, expensive, and failing to deliver promised economic benefits. It doubled the estate tax exemption, allowing the wealthiest households to pass on more wealth tax-free to their heirs. It also included expiring provisions that affected families with low and moderate incomes. However, the TCJA's provisions were temporary and set to expire at the end of 2025, with tax laws reverting to those from 2017. The One Big Beautiful Bill of 2025 aimed to prevent this reversion and make some additional changes, with most taking effect on January 1, 2026.

Trump's Tax Legacy: What's Next?

You may want to see also

![]()

Corporate Tax Rate

The corporate income tax was first enacted in the United States in 1894, but a key aspect of it was soon deemed unconstitutional. In 1909, Congress passed an excise tax on corporations based on income, which, after the ratification of the Sixteenth Amendment to the U.S. Constitution, became the corporate provisions of the federal income tax. The current rate of corporate tax was adopted in the Tax Reform Act of 1986.

In 2017, the Trump administration passed tax reform legislation that changed the law of 'worldwide' to 'territorial' taxation. This imposed a tax only on income derived within US borders, regardless of the taxpayer's residence. The legislation also permanently reduced the 35% corporate income tax (CIT) rate on resident corporations to a flat 21% rate for tax years starting after December 31, 2017.

The 2017 Trump tax law has been criticised for favouring the wealthy, being expensive, and eroding the US revenue base. For example, the law doubled the amount that the wealthiest households could pass on tax-free to their heirs from $11 million to $22 million. It also included provisions that affected families with low and moderate incomes. According to the Tax Policy Center, households in the top 1% will receive an average tax cut of over $60,000 in 2025, compared to less than $500 for households in the bottom 60%.

The Tax Cut and Jobs Act (TCJA) of 2017 included significant changes to the tax code, but its provisions were temporary and set to expire at the end of 2025. The One Big Beautiful Bill (OBBB) of 2025 aims to prevent most of the tax laws from reverting to those from 2017, while also making some additional changes. These changes include adjustments to income tax brackets, eligibility for tax deductions and credits, and the Standard Deduction to reflect inflation.

Juris vs PC Law: What's the Difference?

You may want to see also

![]()

Alternative Minimum Tax

The Alternative Minimum Tax (AMT) is a separate tax system that requires some taxpayers to calculate their tax liability twice: first under ordinary income tax rules, then under the AMT and pay whichever amount is highest. The AMT was enacted in 1969 to prevent wealthy taxpayers from using too many tax preferences.

AMT exemptions and rates are set by law. Taxpayers can use the special capital gain rates in effect for the regular tax if they are lower than the AMT tax rates that would otherwise apply. Some tax credits that reduce regular tax liability do not reduce AMT tax liability. To find out if you may be subject to the AMT, refer to the Alternative Minimum Tax (AMT) line instructions in the Instructions for Form 1040 (and Form 1040-SR). If subject to the AMT, you may be required to complete and attach Form 6251, Alternative Minimum Tax – Individuals.

The American Taxpayer Relief Act of 2012 set the 2012 exemption amounts to $78,750 for Married Filing Jointly and $50,600 for Single, and made future exemption amounts indexed for inflation. The AMT is imposed on a more comprehensive measure of income than regular federal income tax. It is imposed instead of, rather than in addition to, regular tax. AMT is imposed if the tentative minimum tax exceeds the regular tax. Tentative minimum tax is the AMT rate of tax times alternative minimum taxable income (AMTI) less the AMT foreign tax credit.

The AMT taxable income is calculated by taking the taxpayer's regular income and adding disallowed credits and deductions such as the bargain element from incentive stock options, state and local tax deductions, foreign tax credits, and passive activity losses. The amount of AMTI then determines how much of the exemption can be taken, which is subtracted from the AMTI. Finally, the AMTI minus the exemption is taxed at 26% or 28% depending on the level of income.

Understanding Causal vs. Statistical Laws

You may want to see also

Frequently asked questions

The Tax Cuts and Jobs Act (TCJA) was passed by the Senate on December 2, 2017, and was signed into law by President Donald Trump on January 1, 2018.

The 2017 Trump Tax Law included several changes, such as doubling the estate tax exemption, creating a single flat corporate tax rate of 21%, and removing the mandate requiring individuals to purchase health insurance.

The 2017 Trump Tax Law was criticized for being skewed towards the rich, with households in the top 1% receiving an average tax cut of more than $60,000 in 2025, while households in the bottom 60% received less than $500.

The One Big Beautiful Bill, which extended many of the provisions of the TCJA, passed the House of Representatives in 2025.

The One Big Beautiful Bill made changes such as providing tax relief for seniors, enhancing the Adoption tax credit, and eliminating taxes on tips and overtime pay.