The law regarding minimum distributions for Individual Retirement Accounts (IRAs) began with the passage of the Employee Retirement Income Security Act (ERISA) in 1974, but the specific rules for Required Minimum Distributions (RMDs) were formalized in the Tax Reform Act of 1986. This legislation mandated that IRA owners start taking withdrawals from their accounts by April 1 of the year following the year they reach age 70½, ensuring that tax-deferred retirement savings would eventually be taxed. The purpose was to prevent individuals from indefinitely deferring taxes on retirement savings. Over the years, the rules have evolved, with the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 raising the RMD age to 72 for those who turned 70½ after December 31, 2019, reflecting longer life expectancies and changing retirement patterns.

Explore related products

What You'll Learn

- Origins of RMD Rules: The IRS introduced Required Minimum Distributions (RMDs) in 1986 under the Tax Reform Act

- Initial Implementation: RMD rules for IRAs became effective starting in 1987, applying to account holders aged 70½

- Legislative Purpose: Aimed to ensure retirement savings were distributed and taxed during the holder’s lifetime

- Key Amendments: The SECURE Act in 2019 raised the RMD age to 72, updating the original law

- Enforcement Timeline: IRS began enforcing penalties for missed RMDs in 1988, with strict compliance requirements

![]()

Origins of RMD Rules: The IRS introduced Required Minimum Distributions (RMDs) in 1986 under the Tax Reform Act

The Tax Reform Act of 1986 marked a pivotal shift in retirement savings policy with the introduction of Required Minimum Distributions (RMDs) for IRAs. Prior to this legislation, individuals could defer taxes on IRA contributions indefinitely, effectively using these accounts as estate-planning tools rather than vehicles for retirement income. The IRS, recognizing the potential for tax-deferred growth to be exploited, implemented RMDs to ensure that these funds were distributed—and taxed—during the account owner’s lifetime. This change aligned IRAs more closely with their intended purpose: providing financial support in retirement.

The mechanics of RMDs are straightforward but require careful attention. Account owners must begin taking distributions by April 1 of the year following the year they turn 72 (as of the SECURE Act of 2019, which updated the previous age of 70½). The distribution amount is calculated using IRS life expectancy tables, ensuring a systematic drawdown of the account balance. For example, a 72-year-old with a $100,000 IRA balance would divide $100,000 by a life expectancy factor of 27.4, resulting in an RMD of approximately $3,650 for that year. Failure to take the full RMD results in a steep 25% penalty on the shortfall, though the IRS may waive this penalty if the taxpayer corrects the error promptly.

The introduction of RMDs in 1986 was not without controversy. Critics argued that the rules imposed unnecessary complexity on retirees, particularly those with multiple retirement accounts. Proponents, however, emphasized the fairness of taxing deferred income during the account owner’s lifetime rather than allowing it to pass tax-free to heirs. This tension highlights a broader debate in tax policy: balancing individual flexibility with the government’s need to ensure revenue collection. For retirees, understanding RMD rules is essential to avoid penalties and optimize tax efficiency.

Practical compliance with RMD rules involves more than just calculating the required amount. Account owners must also consider the tax implications of distributions, as RMDs are treated as ordinary income. Strategies such as charitable rollovers (Qualified Charitable Distributions) can help mitigate tax liability by directing RMDs to eligible charities. Additionally, retirees with multiple IRAs must calculate RMDs separately for each account but can withdraw the total amount from one or more accounts. This flexibility allows for strategic planning, such as liquidating accounts with lower growth potential first.

In retrospect, the 1986 introduction of RMDs reflects a broader trend in retirement policy: the government’s effort to balance incentives for saving with the need for timely revenue collection. While the rules add complexity, they also ensure that IRAs serve their intended purpose—supporting retirees during their golden years. For account owners, staying informed and proactive is key to navigating RMDs effectively, turning a regulatory requirement into an opportunity for strategic financial planning.

Understanding Eviction Courts: Landlord-Tenant Law and Jurisdiction Explained

You may want to see also

Explore related products

![]()

Initial Implementation: RMD rules for IRAs became effective starting in 1987, applying to account holders aged 70½

The Tax Reform Act of 1986 marked a pivotal shift in retirement planning by introducing Required Minimum Distributions (RMDs) for IRAs, effective in 1987. This change targeted account holders aged 70½, mandating they withdraw a calculated portion of their IRA savings annually. The IRS designed this rule to ensure that tax-deferred retirement funds were eventually taxed and not indefinitely sheltered from government revenue collection. For those reaching this age threshold, the first RMD had to be taken by April 1 following the year they turned 70½, with subsequent distributions required by December 31 each year thereafter.

The calculation of the initial RMD involved dividing the IRA’s year-end balance by a life expectancy factor from the IRS Uniform Lifetime Table. For a 70-year-old, this factor was 27.4, meaning the RMD was approximately 3.65% of the account balance. This percentage increased slightly each year as the life expectancy factor decreased, reflecting the IRS’s assumption of a shorter remaining lifespan. Account holders with multiple IRAs had to calculate RMDs separately for each account but could withdraw the total amount from one or more accounts, offering flexibility in managing distributions.

Non-compliance with RMD rules carried severe penalties—a 50% excise tax on the amount not withdrawn as required. For example, if an individual failed to take a $10,000 RMD, they would owe the IRS an additional $5,000. This harsh penalty underscored the government’s intent to enforce the rule rigorously. However, the IRS occasionally granted waivers for reasonable errors, such as miscalculations or administrative oversights, provided the account holder took corrective action promptly.

The 1987 implementation of RMDs also introduced strategic considerations for retirees. Some account holders chose to take distributions exceeding the minimum to manage tax brackets or fund specific expenses. Others coordinated RMDs with charitable donations via Qualified Charitable Distributions (QCDs), which became available later, to exclude the donated amount from taxable income. These strategies highlighted the importance of proactive planning to optimize both tax efficiency and retirement income.

In retrospect, the 1987 RMD rules for IRAs represented a balancing act between preserving tax revenue and providing retirees with structured access to their savings. For account holders aged 70½, this change necessitated a shift from accumulation to distribution planning, often requiring professional guidance to navigate the complexities. While the rules have evolved since 1987, their initial implementation set the foundation for how retirees interact with their IRA assets today, blending compliance with strategic financial management.

Understanding Intellectual Property Law in the Philippines: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Legislative Purpose: Aimed to ensure retirement savings were distributed and taxed during the holder’s lifetime

The Tax Reform Act of 1986 introduced the concept of Required Minimum Distributions (RMDs) for IRAs, marking a significant shift in retirement savings policy. This legislation mandated that account holders begin withdrawing a minimum amount from their tax-deferred retirement accounts by April 1 following the year they reach age 70½. The primary legislative purpose was twofold: to ensure that retirement savings, which had accumulated tax-free, were eventually distributed and taxed during the holder's lifetime, and to prevent these accounts from becoming perpetual, untaxed wealth transfer vehicles. By imposing RMDs, Congress aimed to align the tax benefits of retirement savings with the original intent of encouraging personal financial security, rather than allowing funds to grow indefinitely outside the tax system.

Consider the mechanics of RMDs to understand their impact. The IRS calculates the minimum distribution amount based on the account balance as of December 31 of the prior year and the life expectancy factor from the Uniform Lifetime Table. For example, a 72-year-old with a $100,000 IRA balance would divide $100,000 by a life expectancy factor of 27.4, resulting in an RMD of approximately $3,650. This formula ensures that larger account balances or older age result in higher distributions, reflecting the policy goal of gradual depletion. Failure to take the full RMD results in a 50% excise tax on the shortfall, a penalty designed to enforce compliance and ensure the intended tax revenue is realized.

From a comparative perspective, RMDs contrast with other retirement savings vehicles like Roth IRAs, which do not require lifetime distributions. Roth accounts are funded with after-tax dollars, eliminating the need for mandated withdrawals since the government has already collected taxes. Traditional IRAs, however, defer taxation on contributions and growth, creating a deferred tax liability. RMDs address this by forcing account holders to recognize taxable income in retirement, ensuring the government receives its share of the deferred taxes. This distinction highlights the legislative intent to balance tax incentives with eventual revenue collection.

Practically, retirees must plan carefully to manage RMDs effectively. For instance, consolidating multiple IRA accounts can simplify calculations, while delaying the first distribution until April 1 of the year following age 70½ allows for additional tax-deferred growth. However, taking the first RMD by December 31 of that same year avoids double RMDs in the following year, which can push retirees into higher tax brackets. Additionally, retirees can satisfy RMDs by making qualified charitable distributions (QCDs) directly from their IRA to a charity, up to $100,000 annually, which counts toward the RMD but is not included in taxable income. This strategy can reduce tax liability while supporting charitable causes.

In conclusion, the legislative purpose behind RMDs reflects a careful balance between encouraging retirement savings and ensuring the tax system remains equitable. By mandating distributions during the account holder's lifetime, Congress addressed the potential for tax-deferred accounts to become tools for intergenerational wealth transfer rather than retirement security. Understanding the rationale, mechanics, and practical implications of RMDs empowers retirees to navigate this requirement effectively, ensuring compliance while optimizing their financial strategies.

Selling Furniture Without a Law Label: Legal Risks and Consequences

You may want to see also

![]()

Key Amendments: The SECURE Act in 2019 raised the RMD age to 72, updating the original law

The SECURE Act of 2019 marked a significant shift in retirement planning by raising the age for Required Minimum Distributions (RMDs) from 70½ to 72. This change, while seemingly minor, reflects a broader acknowledgment of evolving retirement realities. Longer life expectancies and delayed retirements necessitated a reevaluation of the original RMD rules, which were established in 1986 under the Tax Reform Act. By extending the RMD age, the SECURE Act provided retirees with greater flexibility in managing their IRA assets, allowing funds to grow tax-deferred for an additional 18 months.

Analytically, this amendment addresses a critical gap in retirement planning. Prior to the SECURE Act, individuals were forced to begin withdrawals at 70½, often triggering higher tax liabilities during peak earning years. The new RMD age of 72 aligns more closely with modern retirement timelines, enabling retirees to better synchronize withdrawals with their financial needs. For example, a retiree turning 70 in 2020 could now delay distributions until 2022, potentially reducing their taxable income during the initial years of retirement.

Instructively, retirees should reassess their withdrawal strategies in light of this change. Those nearing 70½ should evaluate their cash flow needs, tax brackets, and investment horizons to determine whether delaying RMDs until 72 is advantageous. For instance, individuals in lower tax brackets might benefit from postponing distributions to allow their IRA balances to compound further. Conversely, those with substantial non-IRA assets may choose to take distributions earlier to manage their overall tax burden.

Persuasively, the SECURE Act’s RMD amendment underscores the importance of adaptability in retirement planning. As life expectancies continue to rise and retirement patterns shift, policymakers must periodically update laws to reflect these changes. The increase in the RMD age to 72 is a step in the right direction, but retirees should remain vigilant for future adjustments. Proactive planning, coupled with a clear understanding of these amendments, can help maximize the longevity and efficiency of retirement savings.

Comparatively, the SECURE Act’s RMD change stands out when contrasted with other retirement legislation. While the original 1986 rules were groundbreaking in establishing a framework for tax-deferred savings, they failed to account for the demographic and economic shifts of the subsequent decades. The 2019 amendment, however, demonstrates a more nuanced approach, balancing the need for tax revenue with the realities of modern retirement. This evolution highlights the importance of periodic legislative updates to ensure retirement laws remain relevant and effective.

Understanding the Role of Contract Law in Civil Society Regulation

You may want to see also

![]()

Enforcement Timeline: IRS began enforcing penalties for missed RMDs in 1988, with strict compliance requirements

The IRS's enforcement of penalties for missed Required Minimum Distributions (RMDs) from IRAs began in 1988, marking a significant shift in how retirement account holders were held accountable for tax compliance. This timeline is crucial for understanding the evolution of retirement savings regulations and the consequences of non-compliance. Before 1988, while RMD rules existed, enforcement was less stringent, allowing some account holders to overlook distributions without immediate repercussions. The introduction of penalties in 1988 underscored the IRS's commitment to ensuring that tax-deferred retirement funds were not indefinitely shielded from taxation.

To comply with RMD rules, account holders must withdraw a specific percentage of their IRA balance annually, starting at age 72 (previously 70½ before the SECURE Act of 2019). The IRS calculates this percentage based on life expectancy tables, ensuring a systematic distribution of funds. For example, a 72-year-old with a $100,000 IRA balance would need to withdraw approximately $3,906 in the first year (3.9% of the balance). Failure to take the full RMD by December 31 each year triggers a 50% excise tax on the undistributed amount—a penalty designed to deter procrastination and ensure timely taxation.

The enforcement timeline highlights the importance of proactive planning. Account holders must track their RMD deadlines, especially during life transitions such as retirement or inheritance of an IRA. For instance, beneficiaries of inherited IRAs face different RMD rules depending on their relationship to the original owner and the year of inheritance. Spousal beneficiaries can treat the IRA as their own, delaying RMDs until age 72, while non-spousal beneficiaries must empty the account within 10 years under the SECURE Act. Ignoring these rules can result in substantial penalties, making it essential to consult a financial advisor or tax professional.

A comparative analysis of pre- and post-1988 enforcement reveals the IRS's increasing rigor in tax collection. Before 1988, missed RMDs often went unnoticed or were resolved with minimal penalties. Post-1988, the 50% excise tax became a powerful deterrent, encouraging strict compliance. This shift reflects broader trends in tax policy, where the IRS has prioritized closing loopholes and ensuring fairness in the tax system. For retirees, this means treating RMDs as non-negotiable obligations, akin to filing annual tax returns.

In practical terms, account holders can avoid penalties by setting up automatic distributions, using IRS life expectancy tables to calculate RMDs, and staying informed about legislative changes. For example, the SECURE Act of 2019 raised the RMD age from 70½ to 72, providing a slight reprieve for some retirees. However, this change also underscores the dynamic nature of retirement laws, requiring vigilance to remain compliant. Ultimately, the 1988 enforcement timeline serves as a reminder that retirement planning is not just about saving—it’s about understanding and adhering to the rules that govern those savings.

The Sudden Closure of Northwest Law: Unraveling the Mystery

You may want to see also

Frequently asked questions

The law requiring minimum distributions from IRAs, known as Required Minimum Distributions (RMDs), began with the passage of the Employee Retirement Income Security Act (ERISA) in 1974, but the specific rules were formalized in the Tax Reform Act of 1986.

The purpose of minimum distributions for IRAs is to ensure that taxpayers begin withdrawing and paying taxes on retirement savings at a certain age, preventing the indefinite tax-deferred growth of these accounts.

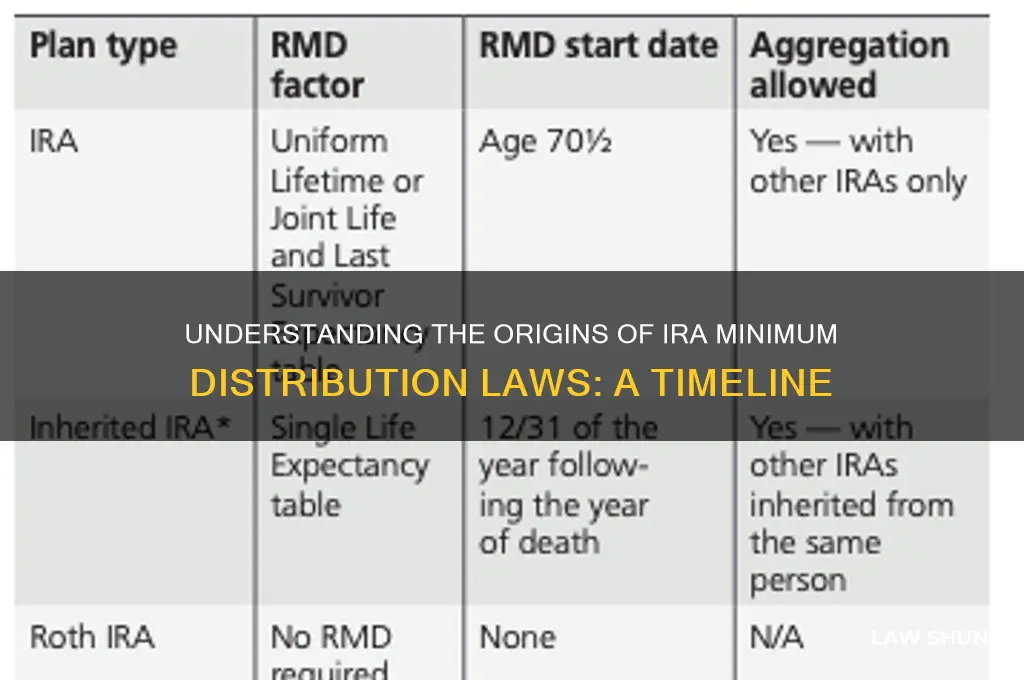

Originally, minimum distributions for IRAs were required to begin by April 1 of the year following the year the account holder turned 70½.

Yes, the SECURE Act of 2019 raised the age for starting RMDs from 70½ to 72 for individuals who turn 70½ after December 31, 2019.

Yes, failing to take the required minimum distribution can result in a 50% excise tax on the amount not distributed as required, in addition to regular income tax on the distribution.