On December 22, 2017, President Donald Trump signed into law the biggest tax overhaul since the Tax Reform Act of 1986, amending the Internal Revenue Code of 1986. The Tax Cuts and Jobs Act TCJA made substantial changes to individual and corporate income tax rates, international tax rules, and deductions. The law was slated to be in effect from 2018 to 2025, with most changes taking effect in January 2018 for the 2018 tax year. While the Act simplified the tax code and lowered taxes for most taxpayers, it also increased federal debt and disproportionately benefited the wealthy, leading to concerns about economic inequality.

| Characteristics | Values |

|---|---|

| Name of the law | Tax Cuts and Jobs Act (TCJA) |

| Type of tax reform | Individual and corporate income tax |

| Major changes | Reduced tax rates for corporations and individuals, increased standard deduction and family tax credits, eliminated personal exemptions, reduced number of tax brackets |

| Effective dates | 2018 to 2025 |

| Impact | Increased federal debt, increased after-tax incomes disproportionately for the affluent, modest impact on economic growth and median wages |

| Other key provisions | Child tax credit, pass-through income deduction, expensing of equipment investment, increased health care premiums and reduced health insurance coverage |

| Subsequent updates | One Big Beautiful Bill Act (2025), Inflation Reduction Act (2022) |

Explore related products

$8.99 $8.99

What You'll Learn

![]()

The Tax Cuts and Jobs Act

One of the key features of the TCJA was the reduction in tax rates for both corporations and individuals. The corporate tax rate was cut to 21%, down from 48% in the 1970s, while the top individual rate was lowered to 37% from 70% in the 1970s. The Act also included an increase in the standard deduction and family tax credits, as well as the elimination of personal exemptions. Additionally, the Act provided a deduction for pass-through income, which was expected to benefit larger, more profitable firms and high-income households.

The TCJA also had an impact on international tax rules, with the introduction of a tax on people who do not obtain adequate health insurance coverage and changes to the corporate alternative minimum tax. The Act simplified the tax code for some taxpayers, but also created new complexities and compliance issues for others. It was estimated to reduce federal revenues by about 1% of GDP in 2018 and 2019, and its effects on economic growth and median wages were modest at best.

The TCJA was slated to be in effect from 2018 to 2025, with taxpayers expected to see an increase in their tax cuts during this period. However, by 2025, when the TCJA expired, all individual tax cuts also expired. There were concerns about the impact of the TCJA on federal debt and the distribution of after-tax income, with critics arguing that it would make the tax system more regressive and benefit high-income households disproportionately.

Creating Personal Laws: Is It Possible?

You may want to see also

Explore related products

![]()

Individual income tax rates

On December 22, 2017, President Donald Trump signed into law the most sweeping tax overhaul since the Tax Reform Act of 1986. The new tax law, known as the Tax Cuts and Jobs Act (TCJA), made substantial changes to individual income tax rates, simplifying the tax code for some.

Trump's tax reform plan cut individual income tax rates, doubled the standard deduction, and eliminated personal exemptions. The top individual rate was 70% in the 1970s and is now 37% under the TCJA. There are currently seven marginal tax rates in place, ranging from 10% to 37%. Marginal tax rates apply only to the portion of income that falls within each tax bracket, not to total income. These rates are adjusted annually for inflation.

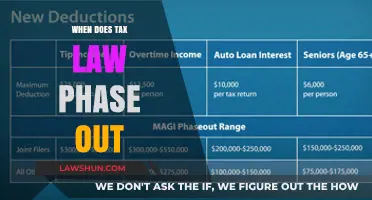

The TCJA also increased the Child Tax Credit, making a wider range of taxpayers eligible for qualification. The credit rose to $2,200 for 2025 and 2026, with indexing starting in 2026. Additionally, individuals aged 65 and older receive a $6,000 "senior bonus" deduction beginning in 2025, phasing out at a rate of 6% once modified adjusted gross income (MAGI) exceeds $75,000 for singles and $150,000 for joint filers.

While the TCJA lowered individual income taxes for approximately 65% of U.S. households, it also raised taxes for about 6%. By 2025, when the TCJA expired, all individual tax cuts expired as well. It is estimated that citizens earning less than $200,000 may see little change in their tax bill or may even face increases.

The First Woman Executed by Hanging

You may want to see also

Explore related products

![]()

Corporate tax rates

President Trump's Tax Cuts and Jobs Act (TCJA) was signed into law on December 22, 2017, and went into effect on January 1, 2018. The TCJA was the largest tax code overhaul in three decades, amending the Internal Revenue Code of 1986. The Act cut taxes for most U.S. taxpayers, with the Tax Policy Center stating in 2019 that it had lowered individual income taxes for approximately 65% of U.S. households. However, the Act was criticized for disproportionately benefiting the wealthy and increasing economic inequality.

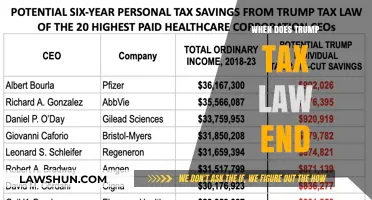

One of the key components of the TCJA was the reduction in corporate tax rates. The maximum corporate income tax rate was cut from 35% to 21%, with the Act creating a single flat corporate tax rate. This led to substantial tax reductions for many of the nation's largest corporations. The 296 largest and consistently profitable U.S. corporations paid $240 billion less in taxes from 2018 to 2021 than they would have under the previous tax rates. These corporations' profits grew by 44% while their federal tax bills dropped by 16%. The number of companies paying exceptionally low tax rates also increased, with the number of companies paying less than 10% in taxes jumping from 56 to 95.

The impact of the TCJA on corporate investment and economic growth was mixed. While the Act led to an estimated 11% increase in corporate investment, its effects on economic growth and median wages were smaller than expected. The TCJA also contributed to an increase in the federal debt. The Congressional Budget Office (CBO) estimated in 2018 that the law would cost $1.9 trillion over ten years, and making the temporary individual tax cuts permanent would cost an additional $400 billion a year beginning in 2027.

The TCJA also made several other changes to corporate taxes. It expanded tax breaks for corporate expenses characterized as capital investment and provided a deduction for pass-through income. It also introduced a territorial tax system, under which only domestic earnings are subject to tax, and certain foreign income of multinational corporations is exempt. Additionally, the Act eliminated the corporate alternative minimum tax and reduced some tax avoidance mechanisms.

Overall, the corporate tax cuts under the TCJA led to significant reductions in tax liabilities for many large corporations, with mixed effects on economic growth and federal revenues. The Act's impact on individuals and households is also varied, with critics arguing that it disproportionately benefited the top 1% and failed to deliver on promises of higher growth, higher wages, and more jobs.

Natural Law's Ancient Roots: When Did It Begin?

You may want to see also

Explore related products

![]()

Federal debt

The Tax Cuts and Jobs Act (TCJA), also known as Trump's Tax Cuts, was signed into law by President Trump on December 22, 2017, and went into effect on January 1, 2018. The Act made significant changes to the rates and bases of both individual and corporate income taxes, including cutting the maximum corporate income tax rate to 21%.

The TCJA has been criticized for increasing federal debt and imposing a burden on future generations. It is estimated that the legislation and executive actions signed into law by President Trump resulted in a $7.8 trillion increase in gross federal debt, with a ten-year cost of about $8.4 trillion, including interest. The increase in the federal debt is attributed to a combination of factors, including $3.6 trillion from COVID relief laws and executive orders, $2.5 trillion from tax cut laws, and $2.3 trillion from spending increases.

The TCJA has also been criticized for its impact on economic inequality, with the share of income going to the top 1% doubling since the pre-1980 period, while the share of wealth owned by the top 1% has risen from around 25% to 42%. In 2019, a person in the bottom 10% would average a $50 tax cut, while a person in the top 1% would receive a $34,000 tax cut. Additionally, the TCJA has been criticized for reducing health insurance coverage and increasing healthcare premiums.

While the TCJA has provided tax cuts for most U.S. taxpayers, it is important to note that it will expire in 2025, and by 2027, citizens earning less than $200,000 may see little change in their tax bills or even face increases. The long-term impact of the TCJA on federal debt and economic inequality remains to be seen, and it is a topic of ongoing debate among economists and policymakers.

Challenging Blue Laws: Constitutionality in Question

You may want to see also

Explore related products

![]()

Tax credits

On December 22, 2017, President Donald Trump signed into law the Tax Cuts and Jobs Act (TCJA), which came into effect in January 2018. The Act was the biggest tax overhaul since the Tax Reform Act of 1986, amending the Internal Revenue Code of 1986. The TCJA was slated to be in effect from 2018 to 2025, with all individual tax cuts expiring in 2025.

The TCJA included several changes to tax credits, which are designed to reduce the tax liability of individuals and corporations. One notable change was the increase in the standard deduction, which was nearly doubled from $13,000 to $24,000 for a married couple in 2018. This meant that more taxpayers would benefit from the standard deduction, simplifying their tax filings.

The TCJA also included an augmented revisitation of the child tax credit, which made a wider range of taxpayers eligible for qualification. The income threshold for families was raised, effectively phasing out the previous restriction that barred families with incomes above $110,000 from eligibility. The child tax credit was also doubled for many families, providing additional tax relief to those with children.

In addition to the changes to the child tax credit, the TCJA also included the Earned Income Tax Credit (EITC) for adults not raising children. This credit provided tax relief to individuals with low wages who were not claiming dependents. The EITC was expanded in 2021 under the American Rescue Plan, providing assistance to approximately 16 million people.

Another tax credit included in the TCJA was the premium tax credit for Affordable Care Act (ACA) marketplace coverage. This credit helped to offset the cost of health insurance for individuals and families purchasing coverage through the ACA marketplaces. During the 2024 open enrollment season, most enrollees were able to find coverage for less than $10 per month, demonstrating the impact of the premium tax credit.

While the TCJA provided tax relief to many Americans, it also increased the federal debt and made the distribution of after-tax income more unequal. The corporate tax cuts benefited wealthy executives and shareholders, while the individual tax cuts were modest for most families and pale in comparison to the large net tax cuts for the wealthy.

Unjust Laws: A Product of Ignorance and Inequality

You may want to see also

Frequently asked questions

Trump's Tax Cuts and Jobs Act (TCJA) came into effect in January 2018.

The TCJA will be in effect from 2018 to 2025.

The TCJA includes several key changes such as cutting tax rates for corporations and individuals, increasing the standard deduction and family tax credits, eliminating personal exemptions, and making it less beneficial to itemize deductions.