Tax law is a complex area with a variety of sources of authority. The US Constitution is the highest law in the land, followed by the Internal Revenue Code (IRC) for tax authority. The IRC is the foundation of all federal tax authority in the US and is interpreted by Treasury regulations, cases that interpret the laws, and IRS rulings. The IRC is supplemented by individual laws passed by Congress and signed into law by the President. At the state level, each state has its own tax laws, which may resemble federal taxation but also include a variety of taxes unrelated to income, such as property and sales taxes. In terms of judicial authority, the weight of a court decision depends on the level of the court, with the US Supreme Court having the highest authority.

| Characteristics | Values |

|---|---|

| Legislative authority | The Constitution of the United States |

| Internal Revenue Code (IRC) | |

| Tax treaties | |

| Administrative authority | Tax authority created by the Treasury Department and the Internal Revenue Service (IRS) |

| Treasury regulations | |

| Revenue rulings | |

| Private letter rulings | |

| Judicial authority | Court decisions |

| Tax Court | |

| Supreme Court | |

| Courts of Appeals | |

| District Courts |

Explore related products

What You'll Learn

![]()

Legislative authority

The IRC is supplemented by individual laws passed by Congress and signed into law by the President or enacted by Congress with a two-thirds majority to override a Presidential veto. These individual laws amend the IRC and include additional information such as effective dates, transitional rules, and special rules. The IRC grants the Treasury Department, through the Internal Revenue Service (IRS), the authority to interpret and administer the IRC. Treasury regulations are published in the Federal Register and provide official interpretations of the IRC, giving directions to taxpayers on how to comply with its requirements.

Treasury regulations can be either legislative or interpretative. Legislative treasury regulations have almost as much weight as the IRC, while interpretative regulations provide guidance on how to comply with the IRC. Revenue rulings issued by the IRS represent agency policy and are binding until revoked, modified, superseded, or withdrawn. They deal with specific issues and are limited to a given set of facts.

In addition to the IRC and Treasury regulations, federal tax research involves other primary sources of law, including case law and agency guidance published by the IRS. The Tax Court provides a national forum for resolving disputes between taxpayers and the IRS, and its decisions can be influential depending on the court's technical expertise and the consistency of its rulings with those of other courts.

Pioneering Female Lawyer in Milwaukee: Who Was She?

You may want to see also

Explore related products

![]()

Administrative authority

One of the key tools at the disposal of the IRS is the issuance of regulations. These regulations are created in collaboration with the Treasury Department to provide guidance on new legislation or address issues pertaining to the Internal Revenue Code. They interpret the law and outline directions on how taxpayers, firms, and charitable groups can adhere to the legal requirements. Regulations are published in the Federal Register and hold significant weight, often being referred to as having "'the force and effect of the law.'"

Another important mechanism utilised by the IRS is revenue rulings. These are official interpretations of the Internal Revenue Code, related statutes, tax treaties, and regulations. Revenue rulings signify the IRS's stance on how the law should be applied to specific scenarios. They are published in the Internal Revenue Bulletin to offer guidance to taxpayers, IRS personnel, and tax professionals. Revenue procedures are also employed, outlining internal IRS practices and procedures that may impact taxpayers' rights and duties.

In addition to the federal level, each state has its own regulatory tax agency that mirrors the role of the IRS. These agencies formulate state administrative regulations and rulings, adapting federal tax laws to fit the specific needs of their state. State courts also contribute to the administrative authority by generating judicial opinions, although many states lack a dedicated tax court. This multi-layered system ensures that tax laws are implemented and interpreted consistently across the nation.

The administrative authority in tax law is a dynamic field, with various guides and tools available to help taxpayers navigate their obligations. The interplay between federal and state authorities ensures that tax laws are effectively administered and enforced, contributing to the overall stability and fairness of the tax system in the United States.

Noah Feldman: Scholar of Constitutional Law

You may want to see also

Explore related products

![]()

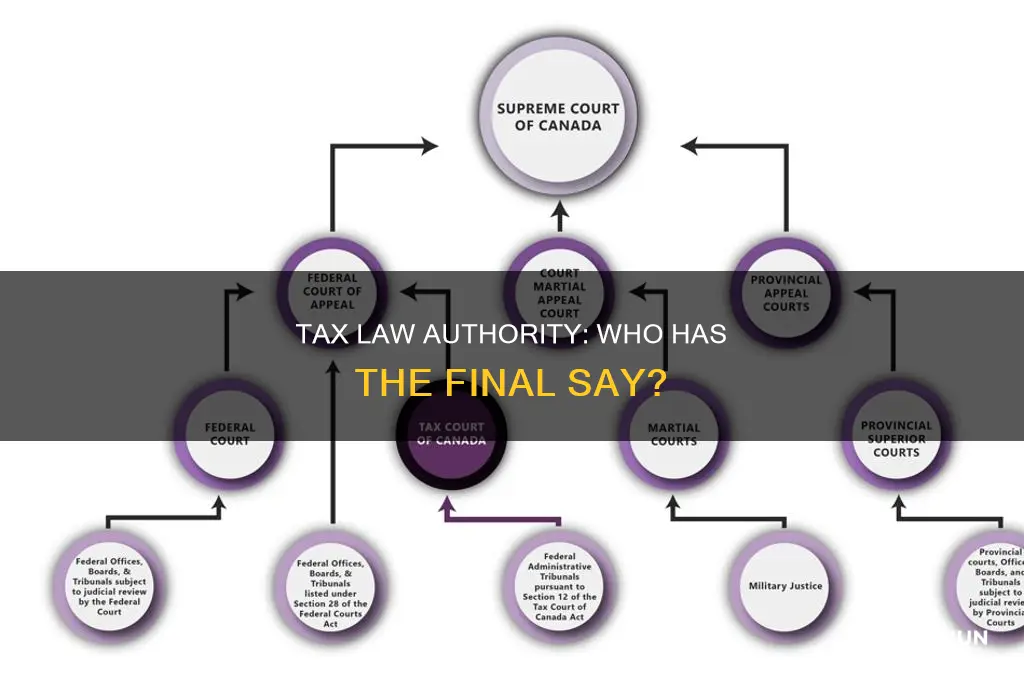

Judicial authority

In the United States, the judicial authority for tax law is primarily exercised by the United States Tax Court, which is a federal trial court of record established by Congress under Article I of the US Constitution. The Tax Court has nationwide jurisdiction and specialises in adjudicating disputes over federal income tax, generally before formal tax assessments are made by the Internal Revenue Service (IRS). The Tax Court is considered to have more technical expertise on tax matters than other trial courts, and its nineteen judges are appointed by the President and have special expertise in federal tax laws.

The US Tax Court is distinct from other courts in that it exercises judicial power exclusively, rather than executive, legislative, or administrative power. Its decisions are not subject to appellate review by Congress, the President, or Article III district courts. However, Tax Court cases can be appealed to the appropriate US Court of Appeals based on the taxpayer's residence. For example, a case decided against a taxpayer in Texas would be appealed to the US Court of Appeals for the Fifth Circuit.

In addition to the Tax Court, federal tax matters can be heard and decided in three other courts: US District Courts, the Court of Federal Claims, and the Bankruptcy Court. The Court of Federal Claims, for instance, has nationwide jurisdiction over claims for money damages against the US, and approximately one-fourth of the cases involve tax refund suits by national and multinational companies.

At the state level, each state has a regulatory tax agency that passes administrative regulations and rulings. State courts also generate judicial opinions on tax matters, although most states do not have an official tax court. State personal and corporate income tax issues often mirror federal income tax, but states also impose various other taxes unrelated to income, such as property taxes, sales taxes, excise taxes, and liquor taxes.

The Amber Alert Law: A Mother's Legacy

You may want to see also

Explore related products

![]()

State tax law

State tax issues can often be researched in a similar way to federal tax issues. Many states' personal income tax, for example, is based on federal income tax. However, states also levy a wide variety of different taxes unrelated to income, such as property taxes, sales taxes, excise taxes, estate taxes, and liquor taxes.

Law vs. Jurisprudence: Understanding Legal Theory and Practice

You may want to see also

Explore related products

$31.99 $35.48

![]()

Tax treaties

The Internal Revenue Code (IRC) is the foundation of all federal tax authority in the United States and is the ultimate authority when researching federal tax law issues. The IRC is interpreted by Treasury regulations, cases that interpret the laws, and IRS rulings.

The IRC is supplemented by individual laws passed by Congress and signed into law by the President. These individual laws amend the IRC, but include extra information such as effective dates, transitional rules, and special rules that are not formally included in the codified IRC. Regulations are the highest administrative authority issued by the Treasury Department. Treasury regulations are published in the Federal Register and codified in Title 26 of the Code of Federal Regulations (CFR).

The Tax Court is generally considered to have more technical expertise on tax matters than other trial courts. The courts can invalidate a section of the IRC or a treaty if it violates the U.S. Constitution.

The United States has income tax treaties with several foreign countries. Under these treaties, residents (not necessarily citizens) of foreign countries are taxed at a reduced rate or are exempt from U.S. income taxes on certain items of income they receive from sources within the United States. These reduced rates and exemptions vary among countries and specific items of income.

If there is no treaty between a country and the United States, or if the treaty does not cover a particular kind of income, you must pay tax on the income in the same way and at the same rates shown in the instructions for Form 1040-NR, U.S. Nonresident Alien Income Tax Return. You should also consult the tax authorities of the state in which you live to find out if that state taxes the income of individuals, and if so, whether the tax applies to your income, or whether your income tax treaty applies in that state.

Texts of US income tax treaties and related documents are available on the website of the U.S. Department of the Treasury. Revenue Procedures are official statements of procedures that affect the rights or duties of taxpayers or other members of the public under the IRC, related statutes, tax treaties, and regulations.

How to Determine if a Law is Constitutional

You may want to see also

Frequently asked questions

The US Constitution is the highest law in the land, followed by the Internal Revenue Code (IRC) for tax authority.

The IRC is the codification of tax laws passed by Congress, also known as Title 26 of the United States Code. It is the foundation of all federal tax authority in the US.

Administrative authority is created by the Treasury Department and the Internal Revenue Service (IRS). Treasury Regulations, published in the Federal Register, are often referred to as having "'the force and effect of the law".

The US Supreme Court is the highest judicial authority. The US Tax Court is a specialised national forum for resolving disputes between taxpayers and the IRS.