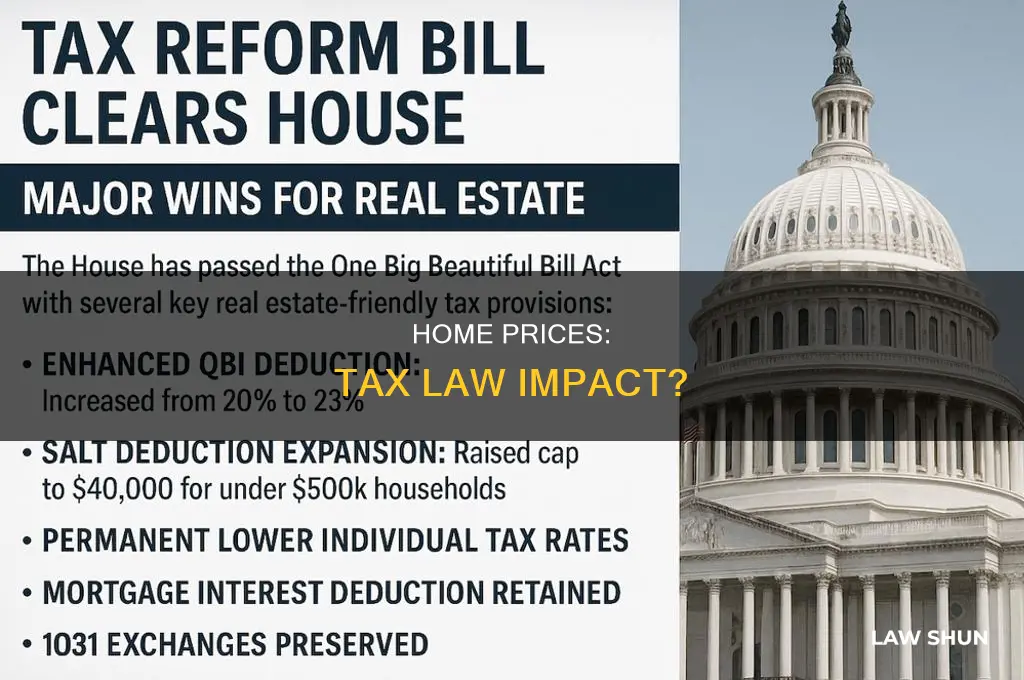

The new tax law will likely slow the rise of home values, creating winners and losers in the housing market. The $10,000 limitation on SALT deductions, the lower deduction cap on mortgages, and the higher standard deduction are expected to negatively impact real estate prices. While economists predict a slowdown in price increases rather than a decline in housing values, the impact will vary depending on location and home value. States with higher property taxes and home values, such as New York, California, and New Jersey, may experience more significant price adjustments, especially for higher-valued homes. Homeowners in these areas may see a decrease in their property values, while buyers may benefit from reduced competition and increased negotiating power. The tax law changes will primarily affect high-income individuals and families living in houses valued at $1 million or above.

| Characteristics | Values |

|---|---|

| Impact on house prices | House prices will be impacted by the new tax law, with some areas experiencing a decrease in value and others seeing slower price increases. |

| Factors influencing impact | The effect on house prices will depend on factors such as location, state and local tax rates, income taxes, property taxes, mortgage interest deductions, and the value of the house. |

| Predicted price changes | Some areas may see a decline in house prices, with projections ranging from a 0.8% decline in the median U.S. county to a 2.6% decline in Loudoun County. |

| High-value houses | Houses valued at $1M+ may experience a negative impact on their prices, especially in states with high property taxes and home values, such as New York, California, and New Jersey. |

| Tax deductions and caps | The new tax law includes a $10,000 cap on state and local tax (SALT) deductions, a lower $750,000 deduction cap on mortgages, and a higher standard deduction. |

| Homeowners' response | Homeowners can get their property taxes reduced through a property tax reassessment if the current market value is lower than the assessed value. |

| Overall market impact | The new tax law is expected to slow the rise of home values, creating winners and losers in the housing market. |

Explore related products

What You'll Learn

- Home prices may drop more in states with higher property taxes and home values

- The new tax law may slow the rise of home values

- Homeowners in certain states will be looking at a larger decrease in home values

- The new tax law will negatively impact very high-income earners

- The new tax law will impact homeowners with big mortgages and property tax bills

![]()

Home prices may drop more in states with higher property taxes and home values

The new tax law is expected to slow the rise of home values, with some economists predicting a decline in house prices. The impact of the tax changes on house prices will depend on the location and value of the house. States with higher property taxes and home values will be the most vulnerable to price adjustments.

The new tax law includes a $10,000 limitation on state and local tax (SALT) deductions, which includes property taxes. This will particularly affect states with high property taxes and high income taxes, such as New York, New Jersey, and California. Homeowners in these states may see a larger decrease in the value of their homes compared to states with lower property taxes and no state income taxes, such as Florida.

The impact of the tax changes on house prices will also depend on the value of the house. Higher-priced homes are expected to be impacted more by the tax changes, especially in areas where there are a disproportionate number of itemizers and where homeowners have big mortgages and property tax bills. For example, a $500,000 home in the District that would have increased to $525,000 by the summer of 2019 may only go up to $515,000 under the new tax law, assuming a 3 percent increase instead of 5 percent.

Additionally, the new tax law lowers the deduction cap on mortgages, only allowing interest to be deducted on mortgages worth up to $750,000. This will impact homeowners with larger mortgages, particularly those in states with higher property values, such as New York, California, and New Jersey.

While the tax changes may lead to a decrease in house prices in some areas, it's important to note that the overall strength of the economy and the limited supply of houses in top markets may prevent a significant decline in housing values. However, the tax changes are expected to slow the rise of home values, creating winners and losers in the housing market.

Signs Your Brother-in-Law is Jealous

You may want to see also

Explore related products

![]()

The new tax law may slow the rise of home values

The new tax law is expected to slow the rise of home values, with realtors predicting a drop in housing prices across the United States. This is due to several factors, including the new tax law's impact on mortgage interest deductions, state and local tax (SALT) deductions, and capital gains exclusions.

Firstly, the new tax law introduces limitations on mortgage interest deductions. Under the previous law, homeowners could deduct qualifying mortgage interest for purchases of up to $1,000,000 plus an additional $100,000 for equity debt. However, the new law caps deductions at $750,000 for married taxpayers and $375,000 for single filers. This reduction in the amount of deductible mortgage debt may slow down the rise of home values, as buyers will now have a lower incentive to purchase more expensive properties.

Secondly, the new tax law caps SALT deductions at $10,000 for all filers, which includes property taxes and state and local income taxes. This change will particularly affect states with high property taxes and income taxes, such as New York, New Jersey, and California. Homeowners in these states may see a larger decrease in the value of their homes compared to states with lower taxes.

Additionally, the new tax law includes changes to capital gains exclusions. Under the previous law, homeowners could exclude up to $250,000 ($500,000 for married couples) in capital gains from the sale of their primary residence if they had owned and resided in the house for at least two of the last five years. The new law extends this timeframe to five of the last eight years, reducing the frequency of exclusions to once every five years. This change may discourage older homeowners from selling their properties, leading to a potential slowdown in the rise of home values.

While the new tax law may slow the rise of home values, it is important to note that the impact will vary depending on location and individual circumstances. Some states with high-priced markets, such as California, Massachusetts, and Colorado, may be more affected by these changes. Additionally, the impact on homeowners with lower-valued properties may be less significant compared to those with million-dollar homes.

Overall, the new tax law is expected to have a notable impact on the housing market, with a potential slowdown in the rise of home values. However, it is difficult to predict the exact outcome, and further analysis is needed to understand the full extent of the law's effects on the complex dynamics of the housing market.

California's Gas Tax: Governor Brown's Signature Move

You may want to see also

Explore related products

![]()

Homeowners in certain states will be looking at a larger decrease in home values

The new tax law is expected to slow the rise of home values, creating winners and losers. The new law's effect on property taxes will impact over 90,000 homeowners in the Washington region alone, according to ATTOM.

The new tax law has made three significant changes that will impact housing prices:

- Capped state and local tax ("SALT") deductions at $10,000 (includes property taxes)

- Lowered the deduction cap on the first $750,000 of a mortgage (down from $1 million)

- Higher standard deduction

Homeowners in states with high property taxes and high income taxes, such as New York, New Jersey, and California, will likely see a larger decrease in home values. This is because the new tax law limits taxpayers to a $10,000 deduction for a combination of their property taxes, school taxes, and state and local income taxes.

In addition, the new tax law's reduction in mortgage interest deductions will also impact homeowners with large mortgages. This change will primarily impact very high-income individuals and families living in houses valued at $1 million or more.

It's important to note that the impact on home values will vary depending on the specific location and the value of the house. For example, within Virginia, the impact will vary between jurisdictions, with Falls Church and Arlington having a higher percentage of homes sold for more than $750,000.

While the new tax law may cause a decrease in home values in certain states, it's difficult to predict the exact impact on the housing market.

Immigration Laws: Pre and Post 1880s

You may want to see also

Explore related products

![]()

The new tax law will negatively impact very high-income earners

Additionally, the new tax law reduces subsidies for homeownership, which were once considered untouchable. This could further contribute to a slowdown in the rise of home values. While economists don't expect housing values to decline due to the overall strength of the economy and the limited supply of houses in top markets, the changes will likely result in slower price increases in expensive housing markets.

Furthermore, the 2017 tax law heavily favoured high-income households, costing $1.9 trillion over ten years, according to the Congressional Budget Office. Despite this, it failed to deliver significant economic gains, and the benefits did not trickle down to most workers. The law included tax cuts for corporations, wealthy shareholders, and large estates, with households in the top 1% (earning over $743,000 per year) receiving substantial benefits. Extending these expiring tax cuts would provide additional advantages to high-income households, exacerbating income inequality.

To address these issues, Congress should take several steps. Firstly, they should allow the 2017 tax cuts for high-income households to expire as scheduled and focus on expanding tax credits for low-income families and workers without dependents. Secondly, they should scale back corporate tax breaks and reduce special tax breaks for wealthy households, ensuring they pay their fair share of taxes. By doing so, Congress can create a more equitable tax system that benefits a broader range of income levels.

Real Estate Law: A Unique Legal Practice?

You may want to see also

Explore related products

$309.99 $380

![]()

The new tax law will impact homeowners with big mortgages and property tax bills

The new tax law will have a significant impact on homeowners with large mortgages and property tax bills. The law includes several changes that will affect the finances of these homeowners, including:

Capping Deductions on Mortgage Interest

The new law introduces a $750,000 cap on the mortgage interest deduction, a decrease from the previous $1 million limit. This change will increase the tax burden on homeowners with large mortgages, as they will no longer be able to deduct as much interest from their taxable income. This may also slow down price increases in expensive housing markets, as the tax breaks previously made it cheaper to afford a bigger mortgage and a bigger house.

Limiting State and Local Tax (SALT) Deductions

The tax law also imposes a $10,000 cap on the amount of state and local taxes, including property taxes, that can be deducted from federal returns. This change will impact homeowners in high-tax states like New York, New Jersey, and California, where state and local taxes often exceed the new cap.

Impact on Home Prices

The combination of these changes is expected to slow the rise of home values, particularly in high-priced homes and areas with higher incomes and a disproportionate number of itemizers. Homeowners in these areas tend to have larger mortgages and property tax bills, and the new tax law will likely result in a larger decrease in the value of their homes compared to other regions.

However, it's important to note that the impact on home prices may vary depending on location and other economic factors. While some areas may experience a decrease in home values, others may see a slower rate of increase or stabilization of prices. Additionally, the overall strength of the economy and the limited supply of houses for sale in top markets may prevent a significant decline in housing values.

Joint Resolutions: How Are They Different From Laws?

You may want to see also

Frequently asked questions

Economists and housing experts predict that the new tax law will slow price increases in expensive housing markets, but they don't expect housing values to decline. However, homeowners in states with high property taxes and high home values, such as New York, California, and New Jersey, may see a larger decrease in the value of their homes compared to states with lower property taxes and no state income taxes, like Florida.

The impact of the new tax law on home prices will vary depending on location and the value of the house. While it's challenging to predict exact figures, some analysts estimate that home prices could deflate by 2% in certain counties.

The new tax law introduces a $10,000 limitation on state and local tax (SALT) deductions, including property taxes. This change may put price pressure on homeowners trying to sell houses above the new $750,000 mortgage interest deduction threshold.

The new tax law may make it more challenging for homebuyers to afford more expensive properties. The reduction in tax breaks means that it will be less advantageous for buyers to take on bigger mortgages and purchase higher-priced homes.