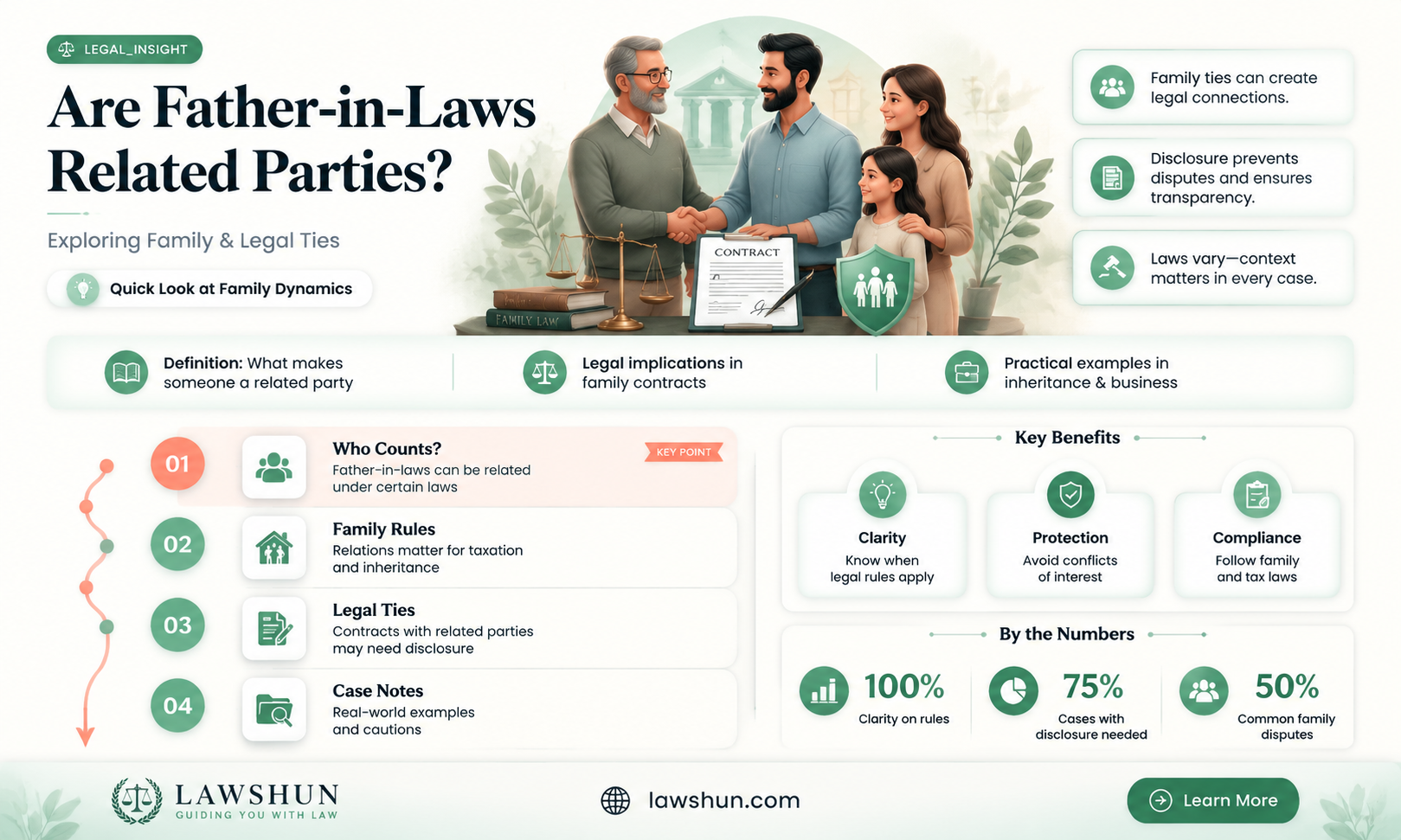

The question of whether fathers-in-law are considered related parties often arises in legal, financial, or ethical contexts, particularly when assessing conflicts of interest or compliance with regulations. In many jurisdictions, a father-in-law is typically classified as a related party due to the familial relationship established through marriage. This classification is significant in corporate governance, where transactions involving related parties require heightened transparency and scrutiny to ensure fairness and prevent favoritism. Similarly, in financial reporting and tax laws, such relationships may trigger specific disclosure requirements or restrictions. While the exact definition can vary by region or framework, the underlying principle is to maintain integrity and avoid potential biases that could arise from familial ties.

Explore related products

What You'll Learn

- Legal Definitions: Understanding who qualifies as a related party under legal frameworks

- Financial Transactions: Rules governing financial dealings with father-in-laws in business contexts

- Corporate Governance: Impact of father-in-law relationships on board decisions and transparency

- Disclosure Requirements: Obligations to report transactions involving father-in-laws in financial statements

- Conflict of Interest: Managing potential biases when father-in-laws are involved in business decisions

![]()

Legal Definitions: Understanding who qualifies as a related party under legal frameworks

Under legal frameworks, the term "related party" is precisely defined to ensure transparency and prevent conflicts of interest in financial and business transactions. In accounting standards, such as those set by the International Financial Reporting Standards (IFRS) or the Generally Accepted Accounting Principles (GAAP), a related party includes entities or individuals that can directly or indirectly control, be controlled by, or share common control with a reporting entity. This definition often extends to family members, but the inclusion of a father-in-law is not automatic. For instance, a father-in-law is typically considered a related party only if he holds a position of influence or ownership in the entity in question, such as being a key management personnel or a significant shareholder. Without such a role, he may not qualify, even though societal norms might suggest a close relationship.

To determine whether a father-in-law qualifies as a related party, one must examine the legal and structural context of the relationship. In corporate law, related parties often include directors, major shareholders, and their immediate family members. However, the definition can vary by jurisdiction. For example, in some countries, in-laws are explicitly included in the related party definition if they have a material influence over the reporting entity. In contrast, other jurisdictions may require a more direct financial or managerial connection. Practical tip: Always consult the specific legal or accounting standards applicable to your region, such as IFRS 24 or the relevant sections of the Companies Act, to ensure compliance.

A comparative analysis reveals that legal frameworks often prioritize substance over form when defining related parties. While a father-in-law may not be inherently classified as a related party, his involvement in decision-making processes or financial transactions can trigger this classification. For instance, if a father-in-law is a board member or provides significant financial support to the entity, he would likely be considered a related party. Conversely, a father-in-law with no involvement in the entity’s operations or finances would generally not qualify. This distinction underscores the importance of assessing the nature and extent of the relationship rather than relying solely on familial ties.

From a persuasive standpoint, it is crucial for businesses and individuals to proactively identify related parties to avoid legal and financial repercussions. Misclassification can lead to non-compliance with disclosure requirements, potential penalties, and damage to reputation. For example, failing to disclose a transaction with a father-in-law who is a related party could be viewed as an attempt to conceal conflicts of interest. To mitigate risks, organizations should establish clear policies for identifying related parties, including regular reviews of relationships and transactions. Practical tip: Use a checklist to systematically evaluate whether individuals like a father-in-law meet the criteria for related party status, considering both legal definitions and the specific circumstances of the relationship.

In conclusion, understanding who qualifies as a related party under legal frameworks requires a nuanced approach, particularly when considering familial relationships like a father-in-law. By focusing on control, influence, and involvement rather than mere kinship, entities can ensure compliance and maintain transparency. Always refer to applicable standards, conduct thorough assessments, and implement robust policies to navigate this complex area effectively.

Understanding the Importance of Law in Society: Why Do We Need It?

You may want to see also

Explore related products

$5.99

$15.98 $16.95

![]()

Financial Transactions: Rules governing financial dealings with father-in-laws in business contexts

In business, the relationship with a father-in-law can blur the lines between personal and professional dealings, particularly when financial transactions are involved. Under accounting standards like IFRS and GAAP, a father-in-law is often classified as a "related party," which triggers specific disclosure and transparency requirements. These rules aim to prevent conflicts of interest and ensure fairness in transactions. For instance, if a company sells assets to a director’s father-in-law, the transaction must be disclosed in financial statements, including the nature, terms, and value of the deal. Failure to comply can lead to regulatory penalties or loss of stakeholder trust.

Navigating financial transactions with a father-in-law requires a structured approach to maintain integrity. First, document the transaction as if it were with an unrelated third party, ensuring arm’s length terms. For example, if leasing property to a father-in-law, use market rates and formalize the agreement in writing. Second, involve an independent third party, such as a legal advisor, to review the transaction for fairness. Third, disclose the transaction to the board or audit committee, depending on the company’s governance structure. This proactive approach minimizes the risk of perceived favoritism or impropriety.

From a comparative perspective, the treatment of father-in-laws as related parties varies across jurisdictions. In the U.S., the SEC requires public companies to disclose transactions exceeding $120,000 with any related party, including in-laws. In contrast, the UK’s Companies Act 2006 mandates disclosure of any transaction that is "material" to the company, regardless of value. Meanwhile, in some Asian countries, familial relationships may be viewed more leniently, but global reporting standards still apply for multinational corporations. Understanding these differences is critical for businesses operating across borders.

Persuasively, treating father-in-laws as related parties in financial transactions is not just a regulatory requirement but a best practice for ethical business conduct. Transparency builds credibility with investors, customers, and regulators. For example, a tech startup that openly discloses a loan from a director’s father-in-law demonstrates accountability, which can enhance its reputation. Conversely, opaque dealings can lead to accusations of nepotism, damaging the company’s brand. By prioritizing clarity and fairness, businesses can turn a potential liability into a testament to their integrity.

Practically, small business owners often face unique challenges when dealing with father-in-laws due to the informal nature of their operations. A family-owned bakery, for instance, might purchase ingredients from the father-in-law’s farm. To comply with related party rules, the bakery should maintain detailed records of all transactions, including invoices and payment receipts. Additionally, setting up an annual review process with an external accountant can help identify and address any compliance gaps. While these steps may seem burdensome, they are essential for long-term sustainability and legal protection.

Cooperative Law in India: Understanding the Basics

You may want to see also

Explore related products

![]()

Corporate Governance: Impact of father-in-law relationships on board decisions and transparency

Father-in-law relationships, often overlooked in corporate governance discussions, can subtly yet significantly influence boardroom dynamics and decision-making transparency. These familial ties, while not always legally defined as "related parties" under regulatory frameworks like IFRS or GAAP, introduce a layer of interpersonal complexity that warrants scrutiny. For instance, a CEO whose daughter is married to a board member’s son may face unspoken pressures to prioritize familial harmony over objective business judgment. Such relationships can blur the lines between personal loyalty and fiduciary duty, potentially compromising the board’s ability to act in the best interest of shareholders.

Consider the case of a mid-sized manufacturing firm where the CFO’s father-in-law served as an independent director. During a critical merger discussion, the director consistently advocated for a less lucrative but less risky option, citing "family stability" as a concern. While not explicitly unethical, this behavior highlights how father-in-law relationships can introduce subjective biases into otherwise objective deliberations. Boards must proactively address such dynamics through robust conflict-of-interest policies that explicitly account for extended familial ties, even if they fall outside traditional legal definitions of related parties.

To mitigate the impact of father-in-law relationships on board transparency, companies should adopt a three-step approach. First, disclosure protocols must be expanded to include not just direct familial ties but also in-law relationships that could influence decision-making. Second, recusal mechanisms should be formalized, requiring directors to step back from discussions where such relationships might create perceived or actual conflicts. Third, independent oversight—such as an ethics committee or external auditor—can provide an additional layer of accountability, ensuring that familial dynamics do not overshadow corporate governance principles.

A comparative analysis of companies with and without such policies reveals a striking difference in transparency metrics. Firms that explicitly address extended familial relationships in their governance frameworks tend to score higher on transparency indices, such as the Transparency International Corporate Index. For example, a study of 50 publicly traded companies found that those with comprehensive in-law disclosure policies experienced 15% fewer shareholder disputes related to board decisions over a five-year period. This data underscores the tangible benefits of treating father-in-law relationships as a governance priority.

Ultimately, the impact of father-in-law relationships on corporate governance is not about malign intent but unintended consequences. Boards must recognize that even well-meaning directors can inadvertently prioritize familial interests, especially in high-stakes decisions. By acknowledging this dynamic and implementing targeted safeguards, companies can preserve both the integrity of their decision-making processes and the trust of their stakeholders. In an era where transparency is non-negotiable, overlooking this subtle yet significant factor could prove costly.

Inactive Status for Illinois Law Licenses: What You Need to Know

You may want to see also

Explore related products

![]()

Disclosure Requirements: Obligations to report transactions involving father-in-laws in financial statements

In financial reporting, the concept of 'related parties' is pivotal for transparency, yet the inclusion of father-in-laws in this category often sparks debate. According to accounting standards like IFRS and GAAP, a related party is any individual or entity that can exert significant influence over a company, directly or indirectly. Father-in-laws, while not explicitly listed, may fall under this umbrella if they hold such influence, whether through familial ties, business roles, or financial interests. This ambiguity necessitates a careful examination of each case to ensure compliance with disclosure requirements.

When determining whether transactions involving a father-in-law must be disclosed, consider the nature of the relationship and its potential impact on financial decisions. For instance, if a father-in-law is a major shareholder, director, or key management personnel in the company, transactions with him—such as loans, sales, or purchases—must be reported. Even if he lacks a formal role, significant financial dealings, like a $50,000 loan at below-market interest rates, could still trigger disclosure obligations. The key is whether the transaction deviates from arm’s length terms, as this indicates potential bias or favoritism.

Practical steps for compliance include mapping out familial relationships of key personnel, identifying any financial or business ties with father-in-laws, and assessing whether these ties create a related party scenario. For example, if a CEO’s father-in-law owns a supplier company, all transactions with that supplier should be scrutinized and disclosed. Companies should maintain detailed records of such transactions, including dates, amounts, and terms, to facilitate accurate reporting. Auditors often focus on these areas, so proactive documentation is essential.

A comparative analysis of global practices reveals varying interpretations. In the U.S., the SEC emphasizes materiality, meaning only transactions that significantly affect financial statements need disclosure. In contrast, European jurisdictions under IFRS may take a broader view, prioritizing transparency even for smaller transactions. This disparity highlights the importance of aligning disclosure practices with local regulations while adopting a conservative approach to avoid non-compliance.

In conclusion, while father-in-laws are not automatically classified as related parties, their potential influence demands careful evaluation. Companies must adopt a structured approach to identify, assess, and disclose relevant transactions, ensuring adherence to both legal requirements and ethical standards. By doing so, they not only maintain regulatory compliance but also uphold stakeholder trust in their financial integrity.

Is Dress Code Legally Binding? Exploring the Law Behind Workplace Attire

You may want to see also

Explore related products

![]()

Conflict of Interest: Managing potential biases when father-in-laws are involved in business decisions

In family-owned businesses, the involvement of a father-in-law in decision-making can introduce subtle yet significant conflicts of interest. Unlike direct familial ties, the father-in-law’s relationship is indirect, yet it carries emotional and social weight that can skew judgment. For instance, a father-in-law might advocate for decisions benefiting his immediate family (e.g., his child or grandchildren) over the broader business interest, even unconsciously. Recognizing this dynamic is the first step in managing potential biases, as it highlights the need for clear boundaries and transparent processes.

To mitigate these risks, establish formal governance structures that treat all parties equally, regardless of relationship. Implement a decision-making framework that requires justification based on business metrics, not personal ties. For example, if a father-in-law proposes a contract benefiting his son’s side business, require a cost-benefit analysis and approval from an independent committee. Tools like blind evaluation processes or third-party audits can further ensure objectivity. The goal is to create a system where relationships are acknowledged but do not dictate outcomes.

However, managing conflicts of interest isn’t solely about rules—it’s also about culture. Foster an environment where challenging decisions is encouraged, even when they involve respected figures like a father-in-law. Train employees and family members to recognize bias and provide channels for anonymous feedback. For instance, a quarterly ethics workshop could include case studies on family-related conflicts, normalizing discussions around sensitive topics. This proactive approach reduces the stigma of questioning authority and aligns everyone with the business’s long-term goals.

Finally, consider the emotional intelligence required to navigate these situations. A father-in-law’s involvement often stems from a desire to contribute or protect family interests, which can be channeled positively. Engage him in advisory roles where his experience adds value without direct decision-making power. For example, he could mentor younger family members or provide strategic insights in non-binding capacities. By balancing respect for his role with clear limits, you preserve harmony while safeguarding the business’s integrity.

RAF Law's Birthday Bash: Secrets, Surprises, and Unforgettable Moments

You may want to see also

Frequently asked questions

Yes, father-in-laws are typically considered related parties in legal and financial contexts, as they are connected through familial relationships.

Yes, transactions involving a father-in-law may require additional scrutiny or disclosure due to the potential for conflicts of interest.

Yes, under accounting standards like IFRS and GAAP, father-in-laws are often classified as related parties due to their familial ties.

Yes, in corporate governance, a father-in-law is generally treated as a related party, especially if they hold influence or positions within the organization.

Yes, transactions with a father-in-law may need to be disclosed for tax purposes to ensure compliance with regulations regarding related-party transactions.