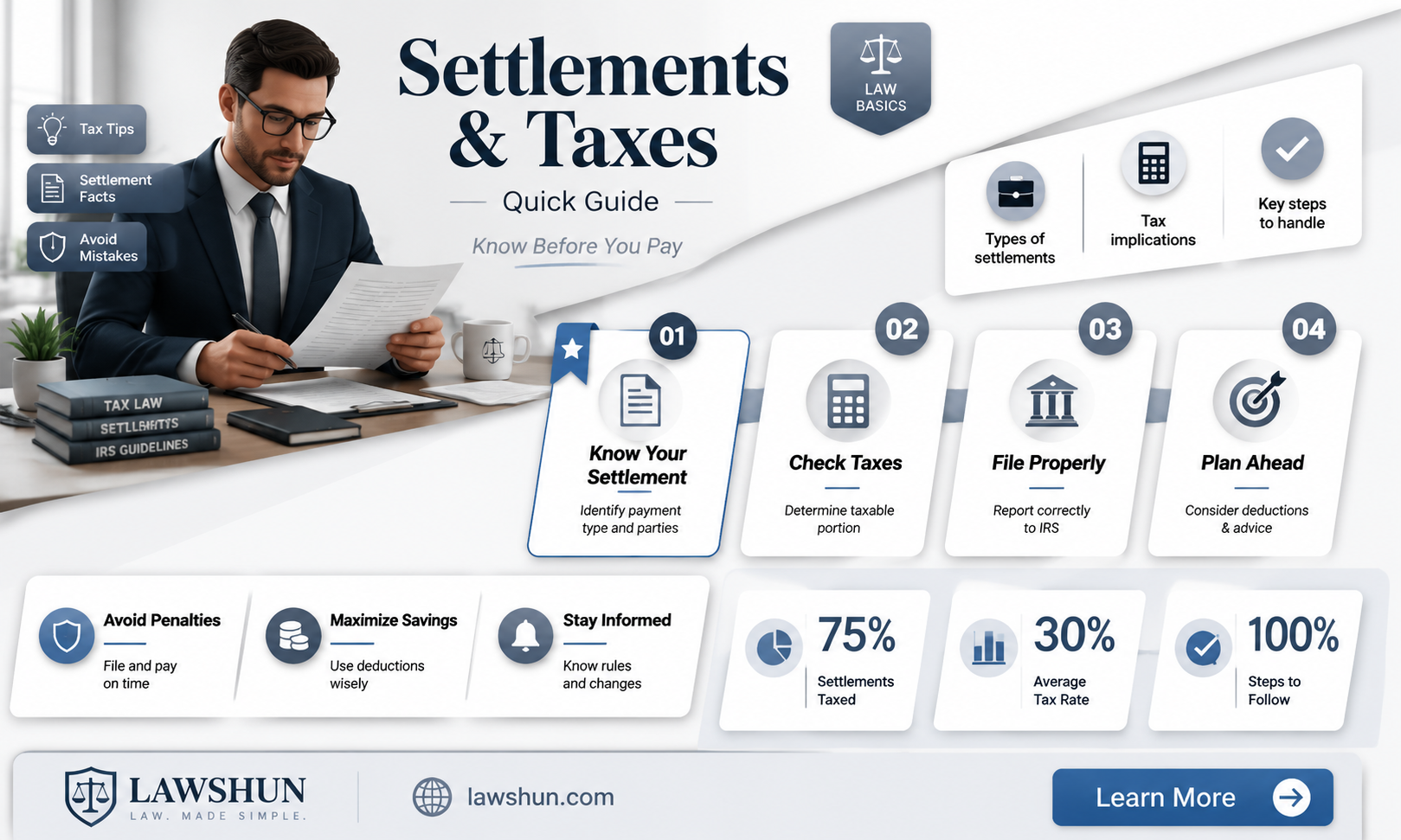

Whether or not law settlements are taxable depends on the type of settlement and the nature of the claims involved. The IRS considers some settlement payments taxable and others non-taxable. Settlements for physical injuries or illnesses are generally not taxable, while settlements for lost wages, emotional distress, punitive damages, and other non-physical claims are taxable. The 'origin of the claim' rule determines how taxes on settlements are applied, based on the initial reason for the lawsuit. For example, if you get laid off and sue seeking wages, you'll be taxed as if you earned those wages. However, if you sue for damage to property, your damages may not be considered income.

Explore related products

What You'll Learn

![]()

Personal injury settlements are tax-free if they compensate for physical injuries or sickness

In the United States, the Internal Revenue Service (IRS) typically does not tax settlement awards from personal injury lawsuits if the cases demonstrate "observable bodily harm". This means that if the injuries are visible, the compensation awarded for those injuries is generally considered tax-free. This is in line with IRS Code § 104(a)(2), which excludes damages received for personal physical injuries or illness from taxable income.

However, it is important to note that there are exceptions and unique circumstances to each lawsuit claim. For example, certain parts of a lawsuit settlement can be taxable under federal law, such as lost wages, punitive damages, or interest on the settlement. Punitive damages, which are awarded to victims for the at-fault party's willful recklessness, are generally subject to taxation. Additionally, if you have already deducted your medical costs as a loss, any subsequent compensation received for those payments will be taxed as income.

On the other hand, compensatory damages, which are awarded to reimburse victims for medical treatment, property damage, pain and suffering, etc., are typically not taxed. This includes damages for medical expenses and property damage, which are not considered part of the taxpayer's income but rather as compensation for financial losses. It is also important to note that emotional distress recovery must be attributed to personal physical injuries or sickness unless the amount is for reimbursement of actual medical expenses related to emotional distress.

Overall, while personal injury settlements that compensate for physical injuries or sickness are generally tax-free, it is always a good idea to seek guidance from a licensed accountant or tax professional to determine your specific tax liability.

Creating Laws: Brands as Legislators

You may want to see also

Explore related products

![]()

Punitive damages are taxable, except in wrongful death claims

Generally, the Internal Revenue Service (IRS) considers settlement awards from personal injury lawsuits as tax-free if the plaintiff demonstrates "observable bodily harm". This is because the IRS does not deem the compensation money awarded for such injuries as a source of income. However, punitive damages are taxable income, as they are not intended to restore the victim's financial status but to penalize the defendant. Punitive damages are awarded when a defendant's actions are deemed willful, malicious, fraudulent, or grossly negligent, with the goal of punishing the defendant and deterring similar behaviour in the future.

Despite this general rule, there is an exception to punitive damages being taxable. In certain US states, such as Alabama, punitive damages awarded for wrongful death are not subject to taxation. This is because, in these states, the state statute provides only for punitive damages in wrongful death claims. As a result, the IRS allows the exclusion of punitive damages from gross income in these specific cases, as outlined in IRC Section 104(c).

It is worth noting that compensatory damages in wrongful death lawsuits are not taxable by the IRS, as they are considered reimbursement for economic or emotional loss rather than a source of income. These damages cover lost wages, property damage, medical bills, medicine, pain and suffering, and other expenses incurred as a result of the wrongful death.

While punitive damages are typically taxable, the taxability of any settlement or award can vary depending on the specific circumstances of each case and the state in which it is awarded. It is always advisable to seek guidance from a licensed accountant or attorney to understand the tax implications of any settlement or award.

In summary, punitive damages are generally taxable, reflecting their punitive nature rather than compensation for losses. However, in the context of wrongful death claims where only punitive damages are permitted by state law, these damages are exempt from taxation. This exception underscores the unique nature of wrongful death cases and the associated compensation.

Exploring the Universe's Law Variations

You may want to see also

Explore related products

![]()

Lost wages are taxable

The IRS generally considers settlement money and damages collected from a lawsuit as taxable income "from whatever source derived". However, there are some exceptions to this rule. For instance, personal injury and physical injury settlements are often exempt from taxation, especially in cases involving "observable bodily harm". This is in line with IRS Code § 104(a)(2), which excludes damages received for personal physical injuries or illness from taxable income.

However, certain parts of a lawsuit settlement can be taxable under federal law, such as lost wages, punitive damages, or interest on the settlement. The IRS might tax the portion of your injury settlement that repays you for lost wages and income. This is because the IRS aims to tax every form of income earned by taxpayers, including compensation that replaces income that would have been earned if an accident or injury had not occurred.

Lost wages are generally taxable, and anyone paying compensation for lost wages should account for the income tax, withhold it, and provide the recipient with a specific IRS form. It is then the recipient's responsibility to report that income when filing their taxes for the year. Lost wages are considered taxable gross income by the IRS if they are meant to cover wages lost or never earned due to an employment law violation.

There are some nuances to the taxability of lost wages. For example, unemployment benefits are taxable, while compensation for property damage is not. This is because property damage compensation does not constitute a profit, as taxes have already been paid on the property, and the claimant is unlikely to recover the property's full value.

Support Your Grieving Brother-in-Law: Practical Tips

You may want to see also

Explore related products

![]()

Damages for emotional distress are taxable

The taxability of damages for emotional distress depends on several factors. While emotional distress damages are generally considered taxable, there are exceptions.

Firstly, it is important to understand the nature of the emotional distress. Emotional distress damages that arise from non-physical injuries, such as mental anguish, defamation, humiliation, depression, or anxiety, are typically considered taxable. On the other hand, if the emotional distress arises directly from a physical injury or sickness, these damages may be excluded from taxation. For example, if a plaintiff experiences emotional distress due to a car accident, the damages for emotional distress would be considered taxable as they arise from a physical injury. However, if the emotional distress leads to physical symptoms, such as insomnia, headaches, or stomach disorders, these physical symptoms may be considered separate physical injuries, and the associated damages may be non-taxable.

Secondly, the purpose of the settlement payment must be considered. The key question to ask is: "What was the settlement (and its corresponding payments) intended to replace?"?. If the settlement payment is intended to compensate for emotional distress specifically, it is more likely to be considered taxable income. However, if the payment is intended to compensate for physical injuries or sickness that led to emotional distress, it may be exempt from taxes.

Additionally, it is worth noting that punitive damages for emotional distress are typically not excludable from gross income, with a few exceptions, such as wrongful death claims.

To ensure that settlement agreements are properly structured for tax purposes, it is advisable to consult with a licensed accountant or tax attorney. They can provide guidance on how to allocate payments to maximize tax benefits and ensure compliance with tax laws.

Animal Welfare: The Laws That Protect Them

You may want to see also

Explore related products

![]()

Consult a tax expert to maximise non-taxable portions

The taxability of lawsuit settlements and other legal remedies is governed by Internal Revenue Code (IRC) Section 61, which states that all income is taxable, regardless of its source, unless a specific exemption applies. This means that settlement money and damages collected from a lawsuit are generally considered taxable income by the IRS. However, there are exceptions to this rule, and not all amounts received from a settlement are necessarily subject to taxation.

To maximise the non-taxable portions of a settlement, it is essential to consult a tax expert or a knowledgeable attorney who can provide clear guidance on how lawsuit settlements are taxed. They can help determine the nature of the claim and the character of the payment, including whether the payment constitutes income or wages. A tax expert can also advise on any tax provisions within the settlement agreement that may result in the exclusion of the settlement from taxable income.

In the context of personal injury and physical injury settlements, it is crucial to understand that these are often considered non-taxable, particularly when they compensate for observable bodily harm or sickness. This is in accordance with IRC Section 104(a)(2), which specifically excludes damages received for personal physical injuries or illness from taxable income. However, there are nuances to this exemption, and consulting a tax expert can help clarify whether your specific circumstances qualify for this exclusion.

Additionally, certain types of discrimination claims may also be exempt from taxation. For example, damages received for emotional distress arising from disparate treatment employment discrimination under Title VII of the 1964 Civil Rights Act are not subject to taxation, as per IRC Section 104(a)(2). On the other hand, punitive damages are typically considered taxable income, unless they are awarded for wrongful death, where only punitive damages are permitted by state statute.

By consulting a tax expert, you can gain a comprehensive understanding of the tax implications of your settlement and receive guidance on maximising the non-taxable portions. They can help you navigate the complexities of the tax code and ensure that you are compliant with any reporting requirements, such as the need for a Form 1099 or W-2, depending on the nature of the settlement.

Trump's Constitutional Threats: A Comprehensive Count

You may want to see also

Frequently asked questions

No, not all law settlements are tax-free. The IRS considers some settlement payments taxable and others non-taxable.

Settlements for lost wages, emotional distress, punitive damages, and other non-physical claims are taxable.

Recoveries for physical injuries and physical sickness are tax-free. Most personal injury settlements are not taxed if they compensate for physical injuries or illnesses.

Here are a few strategies to reduce your tax liability:

- Spread payments over time instead of receiving a lump sum.

- Work with a tax expert to maximize non-taxable portions.