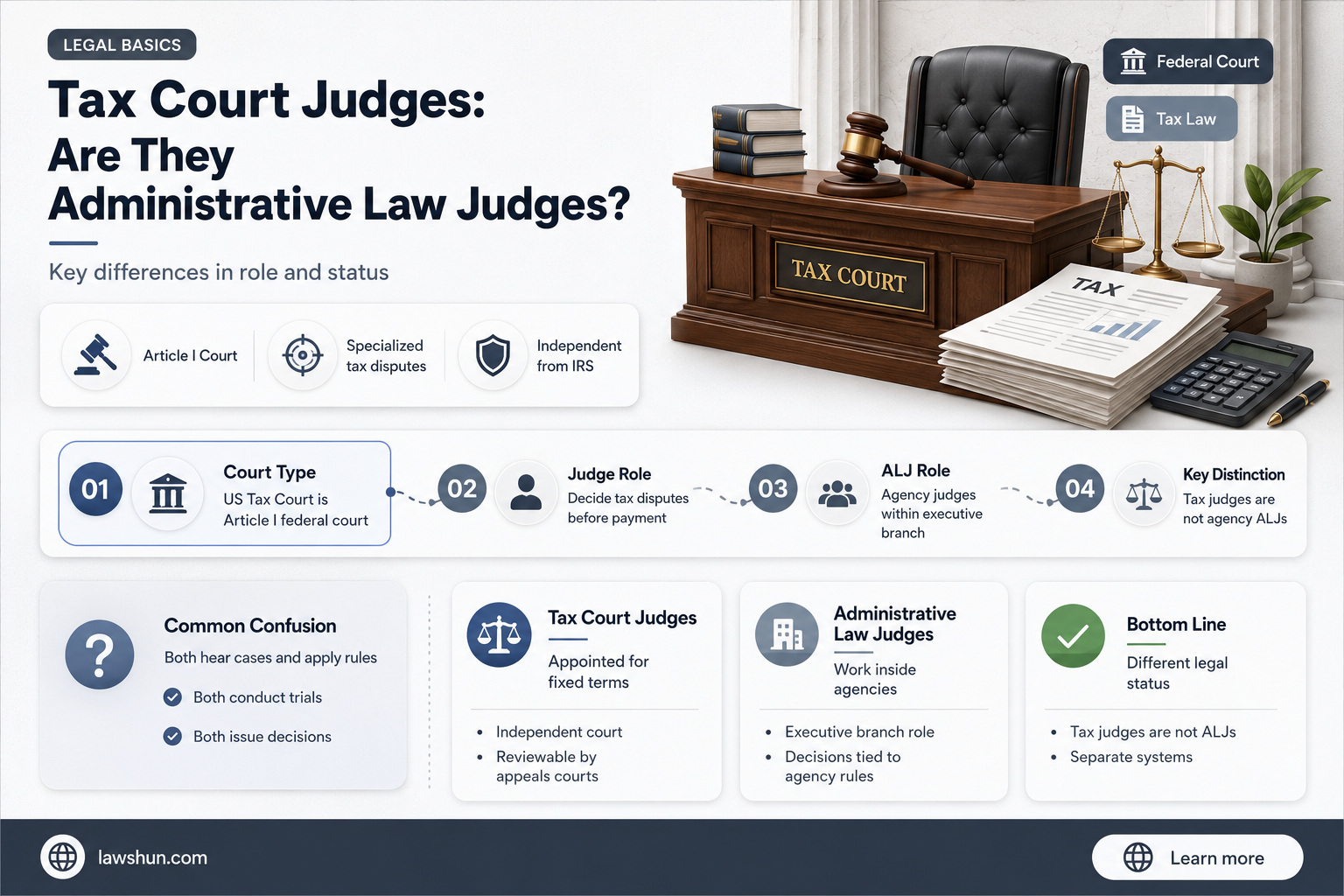

In the United States, tax court judges are appointed by the President and confirmed by the Senate. They are tasked with ensuring that taxpayers are assessed only what they owe and no more. On the other hand, administrative law judges (ALJs) are considered part of the executive branch and are appointed pursuant to the Administrative Procedure Act of 1946 (APA). ALJs have similar powers to trial judges and make both factual and legal determinations. While tax court judges are independent of the Executive and Legislative Branches, ALJs are generally regarded as members of the executive branch.

| Characteristics | Values |

|---|---|

| Nature of Power | Tax Court judges exercise judicial power, whereas ALJs are considered members of the executive branch and do not exercise full judicial power. |

| Appointment | Tax Court judges are appointed by the President, while ALJs are appointed through a merit-based process involving examinations. |

| Removal | Tax Court judges can be removed by the President for "inefficiency, neglect of duty, or malfeasance in office." ALJs can only be removed for cause, with complaints filed with the Merit Systems Protection Board. |

| Jurisdiction | Tax Court judges have exclusive jurisdiction over tax controversies and related matters. ALJs have limited jurisdiction conferred by their home agency's governing statutes. |

| Decision-Making | Tax Court judges ensure taxpayers are assessed accurately. ALJs make both factual and legal determinations, weighing evidence and making recommendations. |

| Nature of Proceedings | Tax Court proceedings can be appealed to higher courts. ALJ proceedings vary by agency, with some having internal appellate bodies or Cabinet secretaries for final appeals. |

| Dress and Address | Tax Court judges wear robes and are addressed formally. ALJs may dress like lawyers or judges, depending on the agency, and may be addressed as "Honorable" or "Your Honor." |

| Independence | Tax Court judges are independent of the Executive and Legislative Branches. ALJs have decisional independence guaranteed by the APA, operating independently from agencies involved in disputes. |

Explore related products

$32.3 $34

What You'll Learn

- Tax Court judges are independent of the Executive and Legislative Branches

- Tax Court judges are appointed by the President

- Tax Court judges can be removed by the President

- Administrative law judges are functionally comparable to Article III judges

- Administrative law judges are part of the executive branch

![]()

Tax Court judges are independent of the Executive and Legislative Branches

In the United States, Tax Court judges are independent of the Executive and Legislative Branches. This is because the Tax Court exercises ""judicial, rather than executive, legislative, or administrative, power". The Tax Court's decisions are not subject to appellate review by Congress, the President, or Article III district courts.

The United States Tax Court is a "court of record" under Article I of the Constitution. It is a specialised court that exclusively hears tax controversies. The Tax Court has jurisdiction to redetermine deficiencies and overpayments in income, gift or estate taxes, and certain excise taxes of private foundations and foundation managers.

Tax Court judges are appointed by the President and confirmed by the Senate, to renewable 15-year terms of office. They are tasked with applying their expertise in tax laws to ensure that taxpayers are assessed only what they owe and no more. Tax Court judges may sit anywhere within the United States, and they travel nationwide to conduct trials in various designated cities.

It is important to note that the President may remove Tax Court judges, after notice and opportunity for a public hearing, for "inefficiency," "neglect of duty," or "malfeasance in office." However, this does not negate the overall independence of the Tax Court from the Executive and Legislative Branches in terms of its decision-making authority and appellate review process.

Simple Prostatectomy Lawsuits: Understanding Your Legal Rights

You may want to see also

Explore related products

![]()

Tax Court judges are appointed by the President

The United States Tax Court was established in 1924 as the Board of Tax Appeals, an independent agency within the Executive Branch. In 1942, the Revenue Act renamed the Board the "Tax Court of the United States", and its members became judges. The Tax Reform Act of 1969 reconstituted the Tax Court as the United States Tax Court, repealing its designation as an Executive Branch agency.

The Tax Court is composed of 19 judges appointed by the President and confirmed by the Senate. Each active judge appointed by the President has two law clerks (attorney-advisers). Former judges whose terms have ended may become "senior judges", able to return and assist the court by hearing cases while serving on recall. Senior judges and special trial judges have one law clerk.

The President may remove Tax Court judges, after notice and opportunity for a public hearing, for "inefficiency, neglect of duty, or malfeasance in office". Reappointment is generally pro forma, regardless of the appointing President's political party.

Tax Court judges have expertise in tax laws and travel nationwide to conduct trials. They preside over cases in which affected persons dispute tax deficiencies determined by the Commissioner of Internal Revenue prior to payment of the disputed amounts.

Civil vs Military Law: What's the Distinction?

You may want to see also

Explore related products

![]()

Tax Court judges can be removed by the President

The United States Tax Court is a "court of record" under Article I of the Constitution, and it is a specialised court that exclusively hears tax controversies. The judges of the Tax Court are appointed by the President and confirmed by the Senate. They are tasked with applying their expertise in tax laws to ensure that taxpayers are assessed only what they owe and nothing more.

While the Tax Court remains independent of the Executive and Legislative Branches, the President may remove Tax Court judges for "inefficiency," "neglect of duty," or "malfeasance in office." This is in contrast to federal administrative law judges (ALJs), who are considered members of the executive branch and are not subject to the supervision or direction of federal agency employees or agents. ALJs are appointed pursuant to the Administrative Procedure Act of 1946 (APA) and can only be removed for cause, with complaints filed with the Merit Systems Protection Board.

The distinction between Tax Court judges and ALJs lies primarily in their independence and removal process. While both types of judges possess similar powers and make both factual and legal determinations, ALJs are generally regarded as part of the executive branch, while Tax Court judges exercise judicial power independently. The President's ability to remove Tax Court judges is a significant difference, as it provides a level of accountability and oversight that is not present with ALJs.

It is important to note that the process of removing a Tax Court judge by the President is not arbitrary or unilateral. Section 7443(f) of the Internal Revenue Code outlines that the President can remove a Tax Court judge after notice and an opportunity for a public hearing. This safeguard helps to ensure that the removal process is transparent and justified, requiring more than just the President's discretion.

In conclusion, while Tax Court judges can be removed by the President for specific reasons, they are not considered administrative law judges. The Tax Court's independence from the executive and legislative branches, combined with the judicial nature of its powers, sets it apart from the typical characteristics of administrative law judges.

Who Votes First on Laws in the US?

You may want to see also

Explore related products

![Administrative Law: Cases and Materials [Connected eBook with Study Center] (Aspen Casebook Series)](https://m.media-amazon.com/images/I/61wklwgRIGL._AC_UL320_.jpg)

![]()

Administrative law judges are functionally comparable to Article III judges

In the United States, the Supreme Court has recognised that the role of a federal administrative law judge is "functionally comparable" to that of an Article III judge. This is because an Administrative Law Judge (ALJ) has powers that are often, if not generally, comparable to those of a trial judge. ALJs may issue subpoenas, rule on proffers of evidence, regulate the course of the hearing, and make or recommend decisions.

However, ALJs are not considered "true" judges as they are always regarded as members of the executive branch, not the judicial branch. This is due to the strict separation of powers imposed by the federal Constitution. ALJs lack broad subject-matter jurisdiction and are limited to the jurisdiction conferred upon their home agency by its governing statutes. Depending on the agency's jurisdiction, proceedings may be complex and involve multiple parties, or they may be simplified and less formal.

ALJs are generally considered to be at the same level as Article I judges, who are also not considered part of the judicial branch. Article I judges may render advisory opinions on a prospective basis, whereas agency ALJs do not have this power as it would violate the Administrative Procedures Act (APA).

ALJs are appointed pursuant to the APA of 1946 and are afforded substantial decisional independence and protection from liability. They are exempt from performance ratings, evaluation, and bonuses, and they may only be removed or discharged for good cause.

In some states, such as New Jersey, state ALJs have varying power and prestige, and their decisions may be treated as recommendations. In certain agencies, ALJs dress like lawyers in business suits, while in other agencies, they wear robes, work in private chambers, and hold hearings in small courtrooms.

Prohibition Laws: The Temperance Movement's Legal Legacy

You may want to see also

Explore related products

![Administrative Law: A Casebook [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/61Vo05Jc1bL._AC_UL320_.jpg)

![]()

Administrative law judges are part of the executive branch

Administrative law judges (ALJs) are considered part of the executive branch of the government in the United States. ALJs are appointed pursuant to the Administrative Procedure Act of 1946 (APA). They are not considered part of the judicial branch due to the strict separation of powers imposed by the federal Constitution.

ALJs are quasi-judicial officials who decide claims or disputes under the formal provisions of the APA. They have similar powers to trial judges, such as issuing subpoenas, ruling on evidence, and making legal and factual determinations. However, they lack broad subject-matter jurisdiction and are limited to the jurisdiction of their home agency.

The constitutionality of ALJs has been challenged in judicial branch courts, as they are considered officers of the United States and are subject to the Appointments Clause of the Constitution. Despite being part of the executive branch, ALJs operate independently from the agencies involved in disputes and are guaranteed decisional independence by the APA.

While the United States Tax Court was previously considered an executive or administrative board, it is now recognized as having an "exclusively judicial role." It is independent of the executive branch, and its decisions are not subject to review by Congress or the President. Therefore, tax court judges are not considered administrative law judges and are separate from the executive branch.

Understanding Crime: Legal Definition and Application

You may want to see also

Frequently asked questions

Tax court judges are part of the judicial branch and are independent of the executive and legislative branches. They are appointed by the President and confirmed by the Senate. On the other hand, administrative law judges (ALJs) are considered part of the executive branch and are appointed pursuant to the Administrative Procedure Act of 1946 (APA). ALJs are not subject to supervision or direction from federal agencies and are afforded immunity from liability stemming from their judicial acts.

Tax court judges preside over cases involving tax controversies, including disputes over tax deficiencies and overpayments. They also handle matters such as redetermining transferee liability, making certain declaratory judgments, adjusting partnership items, and reviewing whistleblower awards. Tax court judges travel nationwide to conduct trials in various designated cities.

Administrative law judges (ALJs) serve as both the judge and trier of fact in administrative hearings. They have the power to administer oaths, rule on evidentiary objections, and make legal and factual determinations. ALJs may issue subpoenas, regulate hearings, and make or recommend decisions. They are often appointed by agencies or the U.S. Office of Personnel Management and are generally considered to have the same scope of authority as traditional courtroom judges.

![Administrative Law: A Lifecycle Approach [Connected eBook with Study Center] (Aspen Casebook) (Aspen Casebook Series)](https://m.media-amazon.com/images/I/61CsI27y1OL._AC_UL320_.jpg)

![Administrative Law: Cases and Materials [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/61uHBdS1IBL._AC_UL320_.jpg)