It is not uncommon for people to be pursued by debt collectors for money they don't owe. This can happen due to accounting errors, identity theft, or the creditor finding the wrong person with a similar name. Scammers can pose as legitimate debt collectors, threatening people with fake debts and using intimidating tactics. Debt collectors are not allowed to lie about the debt they are collecting or use words or symbols that falsely make their letters seem like they're from an attorney, court, or government agency. They are also responsible for ensuring the accuracy of the information they put on credit reports. If you receive a collection notice, it is important to know your rights and the steps you can take to dispute the debt.

| Characteristics | Values |

|---|---|

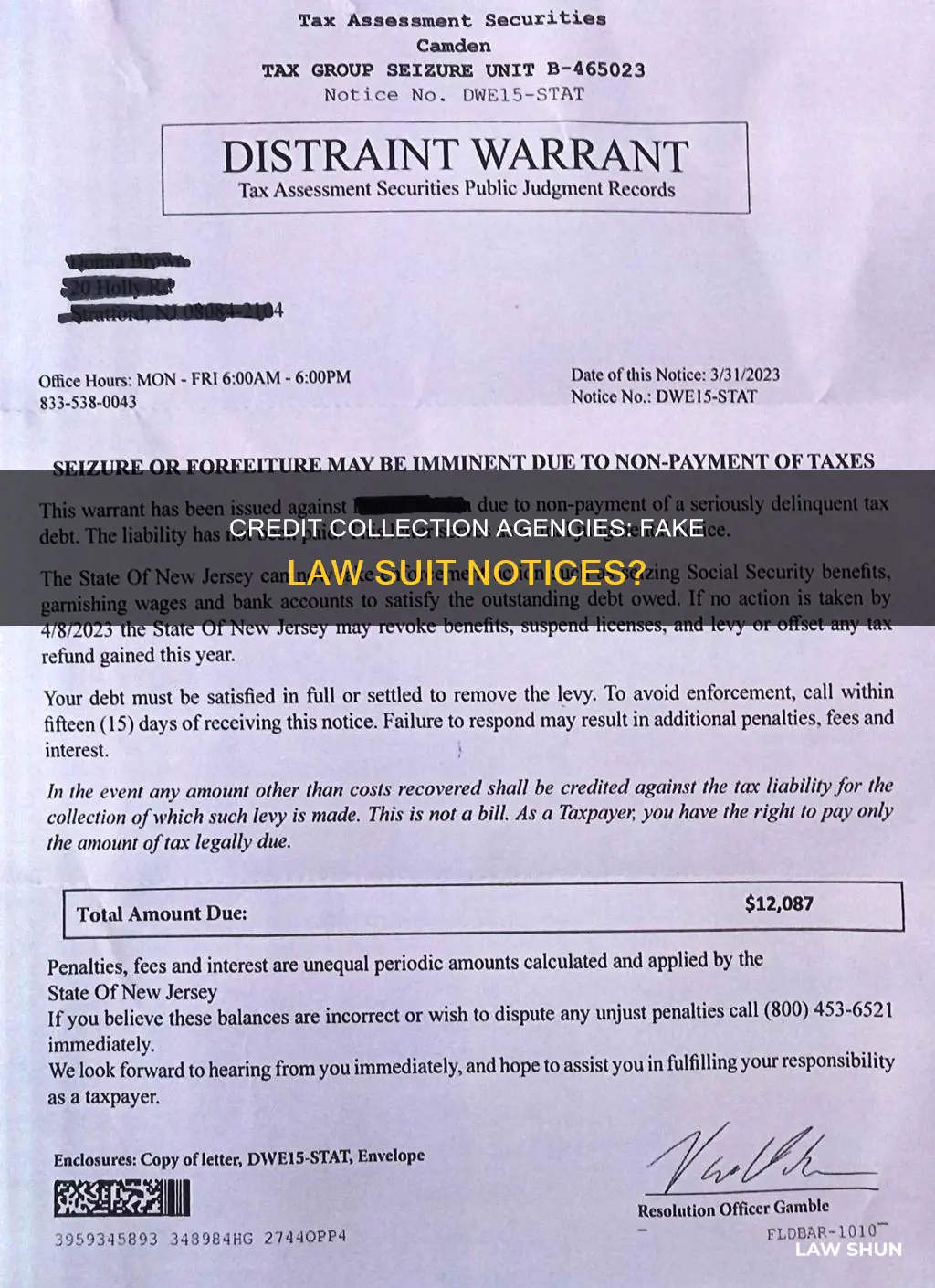

| Can credit collection agencies send fake lawsuit notices? | No, this is illegal under the Fair Debt Collection Practices Act. However, scammers can pose as legitimate debt collectors and send fake notices. |

| What can I do if I receive a fake notice? | Contact a credit reporting agency and ask them to place a fraud alert on your credit report. |

| What can I do to avoid being scammed? | Know all of your real or valid debt. If you owe money, act quickly and contact your creditor to create a payment plan. |

| What should I do if I receive a notice? | Within five days of first contact, debt collectors must send a validation notice with the amount owed, the name of the creditor, and how to dispute the debt. If you dispute the debt, you must give written notice. |

| What can debt collectors do? | Debt collectors can call between 8 am and 9 pm, send notices or letters, and report your debt to credit reporting companies. They can also sue you and get a court order to take money from your paycheck or bank account. |

Explore related products

What You'll Learn

- Debt collectors must send a validation notice within 5 days of first contact

- Collectors can be sued under the Fair Debt Collection Practices Act for false statements

- Scammers pose as legitimate collectors, threatening lawsuits for fake debts

- Collectors can still sue you if you ask them to stop contacting you

- Collectors can't call at unusual times or places, or use words implying they're from a court

![]()

Debt collectors must send a validation notice within 5 days of first contact

While it is unclear whether credit collection agencies can send fake lawsuit notices, it is important to know your rights when it comes to debt collection. Under the Fair Debt Collection Practices Act (FDCPA), debt collectors must send a validation notice within 5 days of their first contact with you. This validation notice should include the following information:

- The amount of debt they believe you owe

- The name of the creditor

- How to dispute the debt in writing within 30 days, after which the debt will be assumed valid

- Confirmation that if you dispute the debt within 30 days, they must provide written evidence of the debt within another 30 days

- A statement that, upon your written request within 30 days, they will provide the name and address of the original creditor if different from the current creditor

If you believe you are being targeted by fake debt collectors, you can contact a major credit reporting agency and ask them to place a fraud alert on your credit report. Additionally, you can request a debt validation letter from the collector to understand the details of the debt and whether it is legitimate. This letter should outline what you owe, who you owe it to, and the important next steps. If you still believe the debt isn't yours, you can send a debt verification letter to dispute it.

Laws Within Laws: Counties and States' Legal Differences

You may want to see also

Explore related products

![]()

Collectors can be sued under the Fair Debt Collection Practices Act for false statements

It is illegal for credit collection agencies to send fake lawsuit notices. Collectors can be sued under the Fair Debt Collection Practices Act for false statements. The Act prohibits debt collectors from making false statements and empowers consumers to act when debt collectors break the law. The Consumer Financial Protection Bureau (CFPB) is the administrator and a primary enforcer of the Fair Debt Collection Practices Act.

The CFPB has confirmed that it may violate the Fair Debt Collection Practices Act for collectors to tell consumers that they owe a debt or an amount of money that they do not actually owe. Debt collectors are responsible for ensuring the accuracy of the information they put on credit reports. For example, they cannot lie about the debt they are collecting or the fact that they are trying to collect debt, and they cannot use words or symbols that falsely make their letters seem like they are from an attorney, court, or government agency. Debt collectors may send notices or letters, but the envelopes cannot contain information about the debt or any information intended to embarrass the recipient.

Collectors must also disclose in the initial written communication with the consumer that the debt collector is attempting to collect a debt and that any information obtained will be used for that purpose. If the initial communication is oral, the collector must disclose this information in the first oral communication as well. In addition, collectors must disclose in subsequent communications that the communication is from a debt collector, except in the case of a formal pleading made in connection with a legal action.

If a collector breaks the law, consumers can submit a complaint with the CFPB. It is important to remember that a debt collector can be liable under the Fair Debt Collection Practices Act even if they claim that they did not know that their statement was false. However, a debt collector will not be held responsible in a lawsuit brought by an individual if they can show that they did not intend to make the false representation and that they had effective procedures in place designed to prevent the mistake.

Common-Law Marriage: Valid or Void?

You may want to see also

Explore related products

![]()

Scammers pose as legitimate collectors, threatening lawsuits for fake debts

It is illegal for credit collection agencies to send fake lawsuit notices. However, scammers do pose as legitimate collectors, threatening lawsuits for fake debts. These scammers can be very convincing, using intimidation, lies, and harassment to get people to pay debts that they do not owe. They often insist on immediate payment through untraceable methods such as gift cards or wire transfers.

To avoid falling victim to these scams, it is important to know all your valid debts. You can do this by requesting a free annual credit report. If you receive a call or message about a debt you don't recognize, ask for "validation information" in writing or over the phone. By law, debt collectors must provide you with information about their company, the amount they believe you owe, the name of the creditor, and how to dispute the debt in writing. They are also required to respect your privacy and cannot threaten you with things they cannot do or pose as government officials.

If you believe you are being scammed, break off contact with the suspected scammer and file a complaint with your local law enforcement and the Attorney General's office. Additionally, contact a major credit reporting agency and ask them to place a fraud alert on your credit report. Remember, if you are ever sued for a debt, do not ignore the lawsuit. Respond by the date specified in the court papers to preserve your rights.

Car Search Laws in Arizona: Know Your Rights

You may want to see also

Explore related products

![]()

Collectors can still sue you if you ask them to stop contacting you

While you can ask a debt collector to stop contacting you, it is important to remember that doing so does not make the debt disappear. Collectors can still sue you, and they may also report your debt to credit reporting companies, which will likely hurt your credit. If you are sued for a time-barred debt, do not ignore the lawsuit. You also can't be sued in a county other than the one you lived in when you signed the contract or when the lawsuit was filed.

If you are unsure about the validity of the debt, you can write to the collector to ask for their evidence. Once you notify the collector in writing that you dispute the debt, they must stop trying to collect the debt until they have provided verification. You can also request that they only contact your attorney. However, this only takes effect if the collector knows or can easily find your attorney's name and contact information.

To stop contact from a debt collector, you must send a written request. The Consumer Financial Protection Bureau (CFPB) offers sample letters for this purpose. Once the collector receives your letter, they are not allowed to communicate with you again except to confirm that they will stop contacting you or to notify you of any legal action they may take, such as filing a lawsuit.

If you believe you are being targeted by a fake debt collector, you can contact a major credit reporting agency and ask them to place a fraud alert on your credit report. It is also important to know all of your real or valid debt so that you can quickly identify whether a debt collector is legitimate.

Chiropractic Records: Lawsuits and Patient Privacy

You may want to see also

Explore related products

![]()

Collectors can't call at unusual times or places, or use words implying they're from a court

While debt collectors can be persistent in their collection efforts, there are laws in place that govern how they can go about doing so. Collectors cannot call at unusual or inconvenient times or places, and they cannot use words or symbols that imply they are from a court, attorney, or government agency.

Collectors are generally prohibited from contacting you before 8 a.m. or after 9 p.m., and they are required to follow your instructions about when and where you don't want to be contacted. For example, if you don't want to receive calls from a debt collector at work, you should inform them, and they are not allowed to contact you there. Additionally, debt collectors cannot make false or misleading statements. They cannot lie about the debt they are collecting or use words or symbols that falsely imply their letters are from an attorney, court, or government agency.

If you ask a debt collector to stop contacting you, they can only communicate with you to confirm that they will stop or to notify you of specific actions they plan to take, such as filing a lawsuit. While stopping a collector from contacting you doesn't make the debt disappear, it is important to know your rights and understand the tactics that collectors are prohibited from using.

To avoid debt collection scams, it is essential to be aware of your valid debt. If you are contacted about a debt you don't recognise, you can quickly identify whether it is real or fake. You can request a free annual credit report to learn more about your debts and ensure that you are not being scammed. Additionally, if you suspect a scam, you can contact a major credit reporting agency and ask them to place a fraud alert on your credit report.

How City Council Wields Power: Zoning Law Edition

You may want to see also

Frequently asked questions

No, credit collection agencies cannot send fake lawsuit notices. Debt collectors have to obey the law and can be held responsible for false statements. If you are unsure about the legitimacy of a debt collector's notice, you can contact your creditor to confirm the details of your debt.

If you receive a fake lawsuit notice, you can break off contact with the agency and file a complaint. You can also contact a major credit reporting agency and ask them to place a fraud alert on your credit report.

A few signs of a fake debt collection notice include:

- The collector is being very pushy about getting payment quickly.

- The notice includes threats or intimidating language.

- The notice includes information that is not accurate or that you know to be false.

If the debt is legitimate, you should act quickly and contact your creditor to try to create a payment plan. You can also ask the debt collector to stop contacting you, but be aware that they may still sue you or report your debt to credit reporting companies.

Within five days of first contacting you, a debt collector must send a written notice that includes the amount of money you owe, the name of the creditor, and instructions on how to dispute the debt in writing if you believe you do not owe the money.