Tax law is an important aspect of the legal system, with economic consequences for individuals, businesses, and investments. It covers a wide range of topics, including income tax, tax credits, corporate tax rates, and tax provisions. Understanding tax law is essential for anyone looking to start a business, buy property, or make significant financial decisions. Additionally, tax law plays a crucial role in shaping public policy and has even influenced the development of common law and democracy. For example, the Magna Carta, a foundational document for Anglo-American democracy, was originally a tax cap agreement. Considering the far-reaching implications of tax law, it is worth considering taking a course in this area to gain a deeper understanding of its impact on economic growth, stability, and individual financial decisions.

| Characteristics | Values |

|---|---|

| Tax law's relevance | There are tax considerations for almost every aspect of life, including marriage, divorce, childbirth, home purchases, and more. |

| Origin of important laws | Many important laws, such as the Rule in Shelley's Case, the Doctrine of Worthier Title, and the Magna Carta, had their origins in tax law. |

| Death tax | People in the United States pay taxes throughout their lives, so paying additional taxes after death seems unreasonable. |

| Fraud in earned income tax credit | Fraudulent refunds have cost the IRS over $125 billion in the last decade, and eliminating this fraud could save the government about $12 billion per year. |

| Ineffective tax credits | Certain tax credits, like the Markets Tax Credit, have benefited wealthy investors instead of creating new employment opportunities in low-income areas as intended. |

| Taxation of carried interest | Hedge fund and private equity owners' carried interest is taxed at capital gains rates, despite resembling wages. |

| High corporate tax rates | The United States has the highest corporate tax rates among developed countries, leading to multinational companies keeping their incomes in other countries. |

Explore related products

What You'll Learn

![]()

Tax law's wide-reaching impact

The One Big Beautiful Bill Act (OBBBA) is a piece of legislation that introduces significant updates to the tax code, impacting how Americans file their taxes in 2025 and beyond. It has wide-ranging implications for both businesses and individuals, with tax changes that are both big and small. The OBBBA includes extensions of the 2017 Tax Cuts and Jobs Act (TCJA) and introduces dozens of new tax provisions.

One notable impact of the OBBBA is the restoration of favourable tax treatment for several types of business expenses. For example, it reinstates 100% expensing of qualified assets in the year they were put into service, also known as bonus depreciation, for property acquired beginning in January. It also allows for immediate expensing of domestic research costs and provides the ability to accelerate the remaining unamortized amounts of previously capitalized research costs incurred between 2022 and 2024.

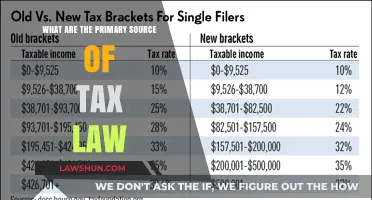

The OBBBA also makes permanent the section 199A qualified business income deduction, with no change to the current 20% deduction percentage. Additionally, it expands the limitation phase-in window from $50,000 for single filers ($100,000 for married filing jointly) to $75,000 for single filers ($150,000 for married filing jointly). These changes can have a significant impact on business cash flow and strategy.

Furthermore, the OBBBA introduces a new type of savings account for children under the age of 18, with a contribution limit of up to $5,000 per tax year (adjusted for inflation after 2027). Employers can also contribute up to $2,500 per year to an employee or dependent of an employee. These contributions are not tax-deductible until the child turns 18, and withdrawals cannot be made until then.

The OBBBA also includes changes to the State and Local Tax (SALT) Deduction, raising the cap to $40,000 for incomes under $500,000 ($250,000 for married filing separately). If an individual's Modified Adjusted Gross Income (MAGI) is over $500,000, the cap is gradually reduced by 30% until it reaches $10,000. These changes can impact whether it makes more sense for taxpayers to itemize deductions or claim the standard deduction.

Obama vs Trump: Immigration Laws Compared

You may want to see also

Explore related products

![]()

Death taxes

The federal estate tax ranges from 18% to 40% of the inheritance amount, and only a small percentage of Americans are subject to it. In 2023, an estate must have assets exceeding $12.92 million to be taxed federally, and this amount will increase to $13.61 million in 2024. The exemption amount is so high that most people do not need to worry about federal estate taxes. Additionally, there are ways to reduce the size of a taxable estate, such as by giving gifts to beneficiaries (up to $16,000 per person in 2022 and $17,000 in 2023) or transferring assets to a spouse, both of which are tax-free.

Twelve states impose a state estate tax separate from the federal government: Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington, and the District of Columbia. Some states also impose an inheritance tax, where the beneficiary is taxed, including Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. However, these states also have exemptions for surviving spouses.

The estate tax has been a source of controversy, with some arguing that it is unfair and unnecessary. However, it has persisted for centuries and brings in significant revenue. For those interested in tax law, understanding death taxes is essential, as they can have a significant impact on high-net-worth individuals and their beneficiaries. It is also important to note that tax law is a numbers-heavy field, and a solid understanding of statistics and accounting is crucial.

Lawsuit Income: Taxable or Not?

You may want to see also

Explore related products

![]()

Tax fraud

Tax law is an important subject that can be both challenging and rewarding to study. While it may not be the most glamorous area of law, it is essential to understanding the financial system and can provide a solid foundation for a variety of legal careers.

One of the key challenges within the field of tax law is the issue of tax fraud, which can take many forms. Tax fraud, or tax scamming, is a serious issue that can have significant financial and legal consequences for those involved. It involves individuals or organisations deliberately avoiding paying taxes that they owe to the government. This can be done through a range of deceptive practices, such as filing false or fraudulent tax returns, engaging in abusive tax schemes, or misusing taxpayer funds.

For example, in a recent case, the founder and former CEO of a charitable organisation, Keith Taylor, pled guilty to charity fraud and tax evasion. Taylor embezzled millions of dollars from his charity, which was meant to help low-income families, and spent the money on personal expenses. He also failed to file personal income tax returns or pay income taxes on the money he received from the charity, evading over a million dollars in federal taxes. As a result, he faces multiple charges of wire fraud and tax evasion, each carrying potential prison sentences.

To combat tax fraud, the Internal Revenue Service (IRS) provides educational materials to help the public recognise and avoid abusive tax schemes. They also offer various forms for reporting tax scams or fraud, such as Form 14157 for reporting fraudulent tax returns filed by tax preparers, and Form 14039 for reporting identity theft. It is important for taxpayers to be vigilant and cautious when choosing a tax preparer to avoid becoming victims of tax fraud themselves.

In conclusion, tax law is a crucial area of study that can provide valuable insights into the financial system and the legal consequences of tax fraud. While it may not be the most exciting subject, it is essential for any aspiring lawyer to have a basic understanding of tax law and the potential pitfalls of tax scams and fraud.

Who Controls the Contract Prison Laws?

You may want to see also

Explore related products

![]()

Tax credits

There are three primary types of tax credits: non-refundable, refundable, and partially refundable. Non-refundable tax credits can reduce the tax owed to zero but do not offer refunds beyond that point. Refundable tax credits, on the other hand, are paid out in full, providing a refund for any remaining credit amount after the tax due is reduced to zero. Partially refundable tax credits, as the name suggests, fall somewhere in between, offering a partial refund of the remaining credit amount.

Various tax credits are available to individuals and businesses, often serving specific purposes. For instance, the Child Tax Credit helps taxpayers with the costs of caring for children, while the American Opportunity Tax Credit assists with qualified education expenses for higher education. Additionally, there is the Earned Income Tax Credit, which is a refundable credit designed for moderate- and low-income taxpayers. Tax credits can also promote certain behaviours, such as the tax credit for installing solar panels for home use, which encourages environmentally friendly actions.

When considering tax law, it is crucial to understand the difference between tax credits and tax deductions and how they can benefit taxpayers. Tax credits offer a direct reduction in tax liability, making them a valuable tool for taxpayers to minimize their tax burden and maximize their refunds. By strategically utilizing tax credits, individuals and businesses can make informed decisions to optimize their financial situations.

Creating City Law: A Step-by-Step Guide

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Tax on carried interest

Tax law is a complex and dynamic field that plays a crucial role in shaping economic policies and social justice. One of the contentious topics in tax law is the taxation of carried interest. Carried interest refers to the percentage of a private fund's investment profits that are kept by the fund manager as compensation for their services. This compensation is often referred to as a "performance fee" and is a key incentive for fund managers in private equity funds, venture capital funds, and hedge funds.

The taxation of carried interest is a highly debated topic. Currently, for federal tax purposes, profits from carried interest are considered a return on investment rather than ordinary income. As a result, they are taxed as capital gains rather than wage or salary income. The top tax rate for capital gains in the US is 20%3.8% net investment income tax, resulting in a total of 23.8%. In contrast, the top tax rate for ordinary income is significantly higher at 37%. This preferential tax treatment for carried interest has become a political flashpoint, with some arguing that it creates an unfair advantage for high-income investment managers.

Critics of the current system argue that taxing carried interest as capital gains allows fund managers to pay lower taxes than most other Americans. They advocate for taxing carried interest as ordinary income, which would result in a higher tax rate and potentially increase tax revenue for the government. Additionally, they highlight the similarity between general partners in investment funds and investment bankers, who pay taxes on their wages, salaries, and bonuses at ordinary rates.

However, supporters of the current tax treatment of carried interest contend that a lower tax rate on capital gains encourages entrepreneurship and promotes financial risk-taking. They believe that increasing the tax rate on carried interest would discourage investors from allocating capital into private markets, potentially hindering economic growth. This debate over the taxation of carried interest highlights the complexities of tax policy, where considerations of economic efficiency, fairness, and incentivization must be carefully weighed against each other.

The Tax Cuts and Jobs Act (TCJA) made a slight adjustment to the tax preference for carried interest. It extended the holding period requirement for investment funds to qualify for long-term capital gains tax treatment from one year to three years. This change ensures that gains from assets held for three years or less are taxed as short-term capital gains at a higher rate. However, as most private equity funds hold their assets for more than three years, the impact of this change on them is minimal.

The Evolution of Laws: Why They Exist

You may want to see also

Frequently asked questions

Tax law is important because there is almost nothing that you will do that won't have economic consequences for which tax law isn't relevant. Whether you are getting married, having a baby, or buying a home, there are tax considerations that you should know about.

If you are starting a business, depositing the proceeds of a theft in a bank, or even finding a diamond in the street and keeping it, there are tax considerations that you should know about.

Many important laws in other fields that are thought of as just a part of common law had their origins in tax law. For example, the Magna Carta, which created the beginnings of Anglo-American democracy, was a tax cap agreement.

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)