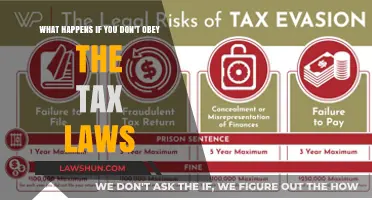

The three basic sources of tax law are legislative, administrative, and judicial. Legislative sources include the U.S. Constitution, U.S. statutes, and tax treaties. Administrative sources include Treasury Regulations and IRS documents such as revenue rulings, notices, and announcements. Judicial sources refer to case law or court decisions that interpret and apply the tax laws. These primary sources are essential for legal and tax research, providing the foundation for understanding and resolving tax-related matters.

| Characteristics | Values |

|---|---|

| Legislative sources | The U.S. Constitution, U.S. statutes and their legislative histories, and U.S. tax treaties |

| Administrative sources | Treasury Regulations, IRS documents, and other IRS publications |

| Judicial sources | Tax cases and court decisions |

Explore related products

What You'll Learn

- Legislative sources: the US Constitution, US statutes, tax treaties

- Administrative sources: Treasury Regulations, IRS documents

- Judicial sources: court decisions, case law

- Primary sources: Internal Revenue Code, tax cases, tax legislation

- Secondary sources: treatises, journals, tax management portfolios

![]()

Legislative sources: the US Constitution, US statutes, tax treaties

The US Constitution, US statutes, and tax treaties are the three primary legislative sources of tax law. These sources are the foundation of federal tax law in the United States, providing the legal framework for taxation.

The US Constitution establishes the legislative branch of the federal government, which includes the House of Representatives and the Senate, collectively known as Congress. Congress is responsible for enacting laws and levying taxes to fund essential government services. It has the power to borrow money if insufficient funds are raised through taxation. The Constitution also grants Congress the authority to ratify treaties, including tax treaties with foreign countries.

US statutes, also known as the Internal Revenue Code (IRC) or simply "the Code," are the primary source of federal tax law. These statutes are the supreme law of the land outside of the Constitution and tax treaties. They encompass all aspects of federal taxation, including income tax, estate tax, and gift tax. The IRC has undergone several major amendments over the years, with the current version being the Internal Revenue Code of 1986.

The legislative history behind the enactment of statutes is also an important source of tax law. This includes judicial committee reports and documented debates in the House of Representatives or the Senate. This legislative history provides valuable context for interpreting and applying tax laws.

Tax treaties are international agreements between the United States and foreign countries. These treaties outline the tax obligations of residents or citizens of the treaty countries, including reduced tax rates or exemptions from US income taxes on certain sources of income within the United States. Tax treaties are particularly relevant when taxpayers have ties to both the US and another treaty country. In cases where tax treaties and statutes conflict, the source enacted or adopted most recently typically takes precedence. However, Congress may specify that either source will apply in different situations.

In summary, the US Constitution, US statutes, and tax treaties form the legislative foundation of tax law in the United States. They are the primary sources that shape and define the country's tax system, providing the legal framework for taxation and guiding the interpretation and application of tax laws.

Understanding Conditional Acceptance in Contract Law

You may want to see also

Explore related products

![Wills, Trusts, and Estates, Eleventh Edition: [Connected eBook with Study Center] (Aspen Casebook) (Aspen Casebook Series)](https://m.media-amazon.com/images/I/71qQLEqup6L._AC_UY218_.jpg)

![Federal Income Taxation [Connected eBook] (Aspen Casebook)](https://m.media-amazon.com/images/I/61dCYeLQMxL._AC_UY218_.jpg)

![]()

Administrative sources: Treasury Regulations, IRS documents

Administrative sources are an important aspect of tax law, encompassing Treasury Regulations and IRS documents. Treasury Regulations, also known as Treasury Decisions (TDs), are published in the Federal Register and codified in Title 26 of the Code of Federal Regulations (CFR). Unlike other federal regulations, Treasury Regulations are cited differently, using a specific format such as "Treas. Reg. §1.61-1". They are updated annually on April 1. These regulations cover a range of topics, including retirement plans, income calculations, and employee classifications.

Treasury Regulations provide guidance and clarification on tax-related matters. For example, they may outline rules for plans that include cash or deferred arrangements, impacting long-term, part-time employees. Additionally, they can specify methodologies for calculating interest rates and making other calculations for defined benefit plans. Treasury Regulations also address requirements for initial and re-enrollment in certain programs, such as updating continuing professional education standards.

The Internal Revenue Service (IRS), a bureau of the US Treasury Department, also plays a crucial role in administrative sources of tax law. The IRS publishes various documents, such as revenue rulings, revenue procedures, private letter rulings, technical advice memorandums, notices, and announcements. These documents interpret and apply tax laws to specific situations, providing guidance to taxpayers and tax professionals.

Revenue rulings, for instance, offer the IRS's official interpretation of the Internal Revenue Code, related statutes, tax treaties, and regulations. They are published in the Internal Revenue Bulletin (IRB) and are authoritative for the same factual circumstances unless officially revoked. Private letter rulings, on the other hand, are written responses to taxpayers' inquiries, interpreting tax laws as they apply to the taxpayers' specific circumstances. These letters are assigned file numbers for reference.

In summary, administrative sources of tax law, including Treasury Regulations and IRS documents, provide essential guidance and clarification on the application of tax laws. They help taxpayers, tax professionals, and administrators navigate the complex landscape of taxation, ensuring compliance and providing direction in specific situations.

Brother-in-Law: Relative or Not for Passport Purposes?

You may want to see also

Explore related products

![]()

Judicial sources: court decisions, case law

Judicial sources are an integral part of tax law, encompassing court decisions and case law. This involves the interpretation and application of tax statutes, regulations, and the Internal Revenue Code (IRC) by various courts, including federal and state jurisdictions.

The U.S. Tax Court, a federal trial court established under Article I of the Constitution, plays a pivotal role in this context. It specialises in resolving disputes between taxpayers and the Internal Revenue Service (IRS). Decisions from this court set important precedents and provide guidance on interpreting and enforcing tax laws. The U.S. Tax Court issues three types of decisions: memorandum decisions, summary decisions, and regular decisions. Memorandum decisions relate to established legal issues and hinge on interpretations of fact. Summary decisions are issued in less complex cases with a lower financial threshold and do not set precedents. Regular decisions, on the other hand, involve novel or unusual points of law and are decided by all judges of the Tax Court, carrying significant weight in shaping tax law.

Other federal courts also contribute to judicial sources in tax law. These include the U.S. District Courts and the Court of Federal Claims, which handle tax cases alongside their other responsibilities. The Court of Federal Claims, for instance, has jurisdiction over tax refund cases where the taxpayer seeks a refund exceeding a certain amount. The U.S. Supreme Court, as the highest judicial authority in the country, also weighs in on tax matters, providing definitive interpretations of tax laws and resolving constitutional questions related to taxation.

State courts, while not directly interpreting federal tax laws, contribute to judicial sources by shaping tax policies within their respective states. They interpret and apply state tax laws, which often interact with federal tax regulations. Additionally, state court decisions can influence how federal tax laws are understood and implemented, especially when state tax policies are challenged on constitutional grounds.

The body of case law generated by these courts forms a critical component of tax law. It provides practical examples of how statutes and regulations are applied in specific situations, offering clarity and guidance to taxpayers, tax professionals, and government agencies alike. This case law is easily accessible through various databases and publications, such as the CCH Tax Court Reporter and RIA's Tax Court Reported and Memorandum Decisions, ensuring transparency and enabling informed decision-making in the complex realm of taxation.

HIPAA Laws: Constitutional Privacy Rights?

You may want to see also

Explore related products

![]()

Primary sources: Internal Revenue Code, tax cases, tax legislation

Primary Sources: Internal Revenue Code, Tax Cases, and Tax Legislation

The Internal Revenue Code (IRC) is the cornerstone of federal tax law in the United States. It is a compilation of official federal tax laws passed by Congress and is organised into subtitles, chapters, subchapters, parts, and sections. The IRC covers all aspects of federal taxation, from income tax to estate and gift tax. The current version is the Internal Revenue Code of 1986, which has had three major amendments: the 1939 Code, the 1954 Code, and the 1986 Code. The sections of the IRC can be found in Title 26 of the United States Code (26 USC), which is updated annually on April 1st. An electronic version of the current United States Code is publicly available, and one can browse "Title 26—Internal Revenue Code" to see the table of contents for the IRC.

Tax cases are decisions made by courts that interpret and apply the IRC. These cases can come from various levels of courts, including the U.S. Tax Court, Federal District Courts, Court of Federal Claims, Circuit Courts of Appeals, and the U.S. Supreme Court. The U.S. Tax Court issues three types of decisions: memorandum decisions, summary decisions, and regular decisions. Memorandum decisions relate to established legal issues and hinge on interpretations of fact. Summary decisions are issued in "small" cases with less than $10,000 in tax liability and are not considered precedent or officially published. Regular decisions involve new or unusual points of law and are decided by all judges of the Tax Court.

Tax legislation refers to the process of passing new tax laws or amending existing ones. This process begins with a bill introduced in either the House of Representatives or the Senate, undergoing several stages of review and amendment before being passed by both houses and signed into law by the President.

Understanding and effectively using these primary sources of tax law is crucial for tax research. They provide the official and authoritative texts that constitute the law itself, and effective research involves not just finding these sources but also interpreting and applying them to specific tax issues.

The Iron Law of Wages: A Historical Perspective

You may want to see also

Explore related products

$32.45

![]()

Secondary sources: treatises, journals, tax management portfolios

Secondary sources of tax law are a great place to start your research as they can guide you to relevant primary authorities. They may cite specific statutes, regulations, or cases that are relevant to your issue, and they may provide commentary or analysis that helps you understand these authorities. When you find a citation to a primary source in a secondary source, you can usually find the full text of the primary source in any of the major tax databases.

Treatises

Treatises are secondary sources that often cover specific areas of tax law or particular provisions of the Tax Code. They can be found in law libraries or on legal research platforms. To use them effectively, start by identifying the treatise that covers the topic you're interested in. Then, use the treatise's table of contents or index to find the relevant sections. Finally, read those sections carefully for a detailed understanding of the topic. Some examples of treatises include:

- Bittker & Eustice: Federal Income Taxation of Corporations & Shareholders

- McKee, Nelson & Whitmire: Federal Taxation of Partnerships & Partners

- U.S. Master Tax Guide

- U.S. Tax Reporter

Journals

Journals are academic publications that feature articles on a wide range of tax topics. They can provide in-depth analysis of complex tax issues and commentary on recent developments in tax law. Journals can be found on legal research platforms, in law libraries, or online. To use them effectively, identify the journal that covers the topic you're interested in, then use the index or search function to find relevant articles. Finally, read those articles carefully to understand the topic.

Tax Management Portfolios

Also known as TMP, Tax Management Portfolios are written by tax practitioners and provide in-depth analysis and practical application of tax topics with reference to the relevant authority governing each topic. They are published by Bloomberg BNA and are available on Bloomberg Law via the Bloomberg Tax Practice Center. TMPs cover a range of topics, including U.S. Income, Estates, Gifts & Trusts, State Tax, Accounting, and International Tax. One helpful feature of TMPs is their indexes, which can be used to locate relevant volumes.

Peter Falk's Brother-in-Law: Unveiling the Mystery

You may want to see also

Frequently asked questions

The three basic sources of tax law are legislative, administrative, and judicial. These sources can be further broken down into:

Legislative sources of tax law include the U.S. Constitution, U.S. statutes and their legislative histories, and U.S. tax treaties. The Constitution's Sixteenth Amendment authorizes Congress to lay and collect taxes on income, and Congress enacts federal tax law in the Internal Revenue Code (IRC).

Administrative sources of tax law include Treasury Regulations, which are the Treasury Department and IRS's statements of law, and IRS documents such as revenue rulings, revenue procedures, notices, and announcements.