The One Big Beautiful Bill legislation, signed into law on July 4, 2025, introduces significant updates to the tax code, impacting how Americans file their taxes in 2025 and beyond. The new tax laws extend provisions of the 2017 Tax Cuts and Jobs Act (TCJA), including an increased standard deduction, lower tax brackets, and a higher estate tax exemption. Additionally, the No Tax on Overtime rule allows eligible workers to claim deductions for overtime pay, while the No Tax on Tips law enables deductions for designated tip earnings. Other changes include adjustments to premium tax credit rules, impacting health insurance coverage through the Marketplace, and the permanent elimination of personal exemptions and miscellaneous itemized deductions. The IRS also offers free tax filing options through various programs for eligible taxpayers. These laws showcase the dynamic nature of taxation policies and their potential impact on individuals and businesses.

Explore related products

What You'll Learn

![]()

The One Big Beautiful Bill law

One notable change in the OBBB is the permanent extension of tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA). This includes increasing the cap on the state and local tax (SALT) deduction, which includes local income, sales, and property taxes. The cap has been raised from $10,000 to $40,000 for the 2025 tax year, with further increases planned for subsequent years.

The OBBB also makes changes to energy credits and deductions. It repeals energy-efficient credits for electric vehicles (EVs), hybrids, charging, and energy-efficient home improvements. Additionally, it cuts energy credits passed under the Inflation Reduction Act.

Another important aspect of the OBBB is the reform of taxes on tips and overtime for certain workers. The new "No Tax on Tips" law allows for a dollar-for-dollar deduction for a designated amount of tips earned by workers in industries where tipping is customary. The income eligible for this deduction is capped at $25,000, and it begins to phase out for higher-income workers.

Furthermore, the OBBB impacts charitable contributions. If a taxpayer claims an itemized deduction for a charitable contribution, they will be required to reduce their deduction by 0.5% of their contribution base, typically their adjusted gross income. On the other hand, taxpayers who claim the Standard Deduction will now also be able to claim a Charitable Deduction for cash contributions.

Overall, the One Big Beautiful Bill law brings about a significant number of changes to the tax code, with most of the provisions taking effect in the 2025 tax year or later. These changes are expected to have a notable impact on Americans' tax filings and financial planning.

Punitive Damages in Contract Law: When and Why?

You may want to see also

Explore related products

![]()

Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act (TCJA) was passed in 2017 and brought about significant changes to the federal tax code. It amended the Internal Revenue Code of 1986, simplifying the tax code for some, lowering corporate debt, and cutting taxes for most US taxpayers. The TCJA also reduced the American corporate tax rate from 35% to 21%, four percentage points lower than the OECD average at the time.

The TCJA overhauled the federal tax code by reforming individual and business taxes. It lowered most individual income tax rates, including the top marginal rate from 39.6% to 37%. The law maintained the seven-bracket rate structure, with rates of 10%, 12%, 22%, 24%, 32%, 35%, and 37%, but updated the income thresholds. The standard deduction was increased to $12,400 for single filers and $24,800 for married filers (as of 2020), compared to $6,500 and $9,550 respectively under prior law.

The TCJA also eliminated the personal exemption and various miscellaneous deductions, such as the state and local tax (SALT) deduction, mortgage interest deduction (MID), and charitable contribution deduction. It limited certain itemized deductions and made it less beneficial to itemize deductions. Additionally, the TCJA allowed for full and immediate expensing of short-lived capital investments for five years and increased the section 179 expensing cap from $500,000 to $1 million.

The TCJA was expected to lower taxes by an average of $1,600 in 2018 and 2025, according to the Tax Policy Center. However, the bottom 80% of taxpayers (income under $149,400) were projected to receive only 34%-35% of the benefit, with the top 20% of Americans by income receiving about 65% of the tax savings. The TCJA was also estimated to increase the federal debt and after-tax incomes disproportionately for the most affluent. While it led to an 11% increase in corporate investment, its effects on economic growth and median wages were smaller than expected.

Understanding the First Law of Thermodynamics: Q System and Surroundings

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UL320_.jpg)

![]()

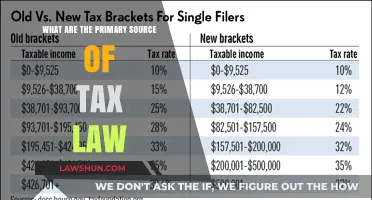

Adjustments to tax brackets

Permanent Tax Brackets

The OBBB has made the seven federal tax brackets permanent at the following rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These rates are applicable for the 2025 tax year and will remain in effect indefinitely. This provides stability and predictability for taxpayers in planning their finances.

Adjustments for Inflation

The IRS makes annual inflation adjustments to tax brackets to keep them in line with the changing cost of living. For the 2025 tax year, the income limits for all tax brackets have been adjusted for inflation. This means that the income thresholds for each bracket have been increased to account for inflation, resulting in higher incomes being taxed at the same rate. For example, the top end of the 10% tax bracket for a single filer increased from $11,600 in 2024 to $11,925 in 2025.

Alternative Minimum Tax (AMT) Adjustments

The OBBB has adjusted the Alternative Minimum Tax (AMT), which was originally created to prevent high-income earners from using tax loopholes to reduce their tax liability. The AMT exemption has increased to $88,100 for individuals and $137,300 for married couples filing jointly. However, the phaseout threshold for the AMT exemption has been reduced to 25 cents per dollar earned once income reaches certain levels, such as $500,000 for single filers.

Child Tax Credit

The OBBB has increased the Child Tax Credit to $2,200 per qualifying child for the 2025 tax year. This credit is not adjusted for inflation and provides a substantial benefit to families with children.

Standard Deductions

Standard deductions have increased for the 2025 tax year. For single taxpayers, the standard deduction rose to $15,000, while for married couples filing jointly, it increased to $30,000. Additionally, a new ""bonus" deduction for older adults has been introduced, allowing those age 65 and older to claim a higher deduction, subject to income thresholds.

High-Income Filers Threshold

A key income threshold to watch for high-income filers is $197,300 for single filers and $394,600 for married couples filing jointly. These thresholds mark the transition from the 24% tax rate bracket to the higher 32% rate bracket.

These adjustments to tax brackets are intended to simplify the tax system, provide relief to taxpayers, and ensure that the tax code keeps pace with inflation. However, it's important for individuals to consult with tax professionals to understand how these changes may impact their specific financial situations.

Commandments: A Unique Law Code

You may want to see also

Explore related products

![]()

Changes to premium tax credit rules

The premium tax credit, also known as PTC, is a refundable credit that helps eligible individuals and families cover the cost of health insurance purchased through the Health Insurance Marketplace. Here are the key details regarding changes to the premium tax credit rules:

Eligibility

To be eligible for the premium tax credit, certain requirements must be met. Firstly, household income must fall within a specified range. For tax years 2021 through 2025, Congress temporarily expanded eligibility by eliminating the requirement that a taxpayer's household income must not exceed 400% of the federal poverty line. As a result, taxpayers with household incomes above this threshold may still be allowed to claim the premium tax credit if they meet other eligibility criteria. Additionally, those who received unemployment compensation during 2021 are considered to have household incomes within the eligible range.

Enrollment and Coverage

The premium tax credit is available immediately upon enrollment in an insurance plan through the Health Insurance Marketplace. Individuals and families with incomes at or above the federal poverty level can benefit from this credit. It's important to note that if you enroll in an employer-sponsored plan, including retiree coverage, you are generally not eligible for the premium tax credit for Marketplace coverage. However, you may be eligible for the credit if you decline employer coverage or if your employer offers an ICHRA that is deemed unaffordable.

Advance Payments and Reporting Changes

Individuals can choose to receive advance payments of the premium tax credit, which can lower their monthly insurance premiums. However, it is crucial to report any changes in household income, family size, or other life circumstances promptly to the Marketplace. These changes can impact the amount of the premium tax credit and, consequently, affect your tax refund or the amount of tax owed.

Claiming the Credit

To claim the premium tax credit, individuals must file a federal income tax return and attach Form 8962, Premium Tax Credit (PTC), to their return. This form is used to reconcile the amount of advance payments received with the actual credit amount based on household income and family size.

Special Considerations

There are special considerations for married couples and individuals facing certain circumstances. Married couples who receive advance payments must generally file a joint return to qualify for the premium tax credit. However, exceptions are made for survivors of domestic violence and individuals abandoned by their spouses. Additionally, those who qualify to file as Head of Household may also be eligible for the credit.

These changes to the premium tax credit rules aim to provide financial assistance to eligible individuals and families, ensuring they can afford health insurance coverage through the Health Insurance Marketplace.

The First Law University in Kerala: A Historical Overview

You may want to see also

Explore related products

![]()

Tax Expenditure Budget

The tax expenditure budget outlines the estimated revenue losses from federal income tax laws, including special exclusions, exemptions, deductions, credits, deferrals, and preferential tax rates. It is published annually by the Office of Management and Budget (OMB) and the congressional Joint Committee on Taxation (JCT). These lists, also known as Tax Expenditure Budgets, detail the revenue losses attributed to exceptions in the income tax law, which are considered alternatives to standard provisions.

Tax expenditures reduce the income tax liability for individuals and businesses that engage in activities specifically encouraged by Congress. For example, the deduction for charitable contributions reduces tax liability for those who itemize charitable donations on their tax returns. Similarly, tax expenditures can reduce tax liability for individuals Congress wishes to assist, such as retired or disabled people receiving Social Security benefits, who are exempt from federal income tax on a portion of their benefits.

The budget generally treats tax expenditures as revenue losses rather than spending. The OMB's tables display tax expenditures as the portion of refundable tax credits that offset positive income tax liabilities. In contrast, the JCT's tables include both the revenue loss and outlay effects of refundable credits, with the combined revenue loss for all provisions not equalling the sum of individual provision losses due to interactions between provisions.

Tax expenditure estimates are for fully phased-in tax changes and account solely for changes in income taxes. They do not include the effects of changes in economic behaviour or other taxes such as payroll or estate taxes. The ideal administrative agency for a tax subsidy may vary, and certain tax expenditures may be better administered by agencies with specific expertise.

Natural Law vs Divine Command: What's the Difference?

You may want to see also