Tax brackets are a range of incomes taxed at given rates, which differ according to filing status. In a progressive tax system, as income rises, it is taxed at a higher rate. The Internal Revenue Service (IRS) adjusts tax provisions annually to account for inflation, with the income limits for all tax brackets and filers adjusted for inflation for the 2025 tax year. There are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These brackets are permanent, along with standard deductions and a new bonus deduction for older adults.

| Characteristics | Values |

|---|---|

| Number of federal income tax brackets | 7 |

| Tax bracket percentages | 10%, 12%, 22%, 24%, 32%, 35%, 37% |

| Tax calculation | Taxable income is divided into layers, with each layer taxed at the corresponding rate |

| Tax rate application | The highest tax rate applies only to the portion of income within that layer |

| Tax rate progression | As income increases, the tax rate on the next layer of income is higher |

| Tax bracket determination | Based on filing status and taxable income |

| Filing status | Single, Married Filing Jointly, Married Filing Separately, Head of Household, Qualified Surviving Spouse |

| Tax credits | Child tax credit, education tax credit, adoption cost credit, solar panel cost credit |

| Tax deductions | Standard deductions, “bonus” deduction for older adults, itemized deductions |

| Alternative Minimum Tax (AMT) | Exemption of $88,100 for individuals, $137,300 for married couples filing jointly |

| Inflation adjustments | Made annually by the IRS to over 60 tax provisions to account for changes in the cost of living |

| Income limits | Adjusted for inflation in 2025, with income limits for all tax brackets and filers |

| Tax laws | "One Big Beautiful Bill Act" enacted in July 2025, establishing new tax laws and extending provisions of the 2017 Tax Cuts and Jobs Act (TCJA) |

| Tax planning | Knowledge of tax brackets can help with tax planning and taking advantage of credits and deductions |

| Tax returns | Due in April or October with an extension |

Explore related products

What You'll Learn

![]()

How much tax do you pay on your income?

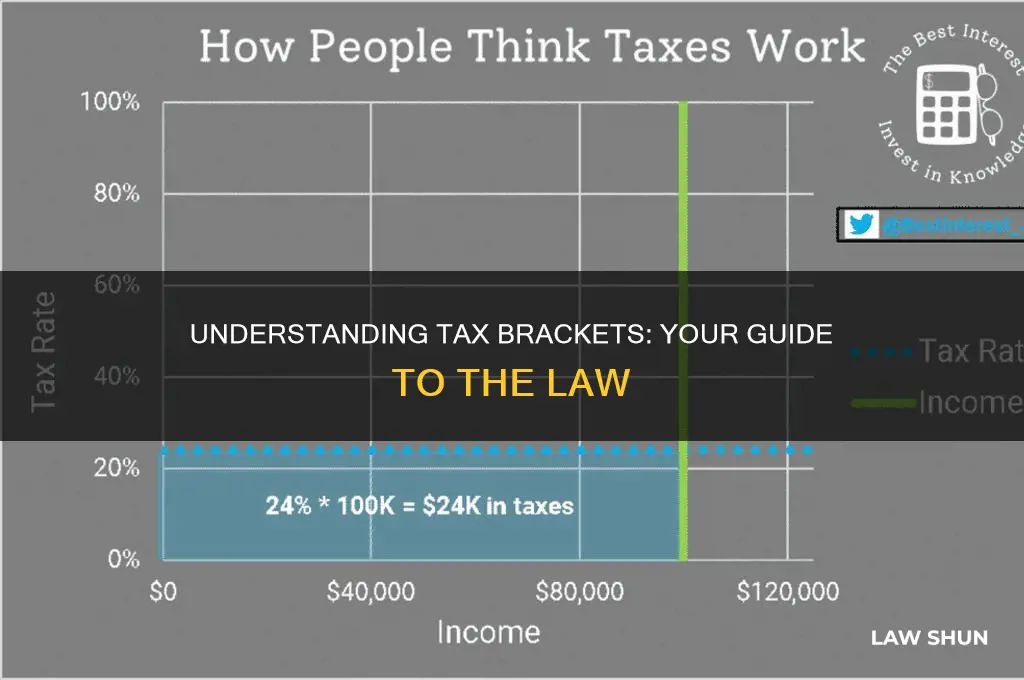

The amount of tax you pay on your income depends on your income level and filing status. In the United States, there are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These brackets are progressive, meaning that as your income increases, it is taxed at a higher rate. For example, if you had $50,000 of taxable income in 2024 as a single filer, you would pay 10% on the first $11,600, 12% on the income between $11,601 and $47,150, and 22% on the rest. Thus, your total tax bill would be roughly $6,053, or about 12% of your taxable income, even though your highest bracket is 22%.

It is important to note that these percentages are not applied to your entire income. Instead, you pay a higher rate only on the portion of your income that falls within a higher tax bracket. Additionally, the tax brackets and rates may vary depending on the state, as some states have different brackets or no income tax at all. For instance, Colorado has a flat tax rate of 4.25% on taxable income.

The Internal Revenue Service (IRS) adjusts over 60 tax provisions annually to account for inflation and changes in the cost of living. These adjustments impact income tax brackets, deductions, and other inputs. For instance, the 2025 tax changes included in the "One Big Beautiful Bill Act" resulted in an average increase of about 2.8% in tax parameters.

To determine your tax liability, you must first establish your filing status, which can be single, married filing jointly, married filing separately, head of household, or qualified surviving spouse. Next, you apply the relevant tax rates to different portions of your taxable income based on the tax brackets. It is worth noting that various tax credits and deductions can help lower your tax bill.

Exploring Europe's Complex Web of Tax Laws

You may want to see also

Explore related products

![]()

How does the IRS adjust for inflation?

The IRS makes annual inflation adjustments to many tax provisions, which could help offset the impact of rising prices. These adjustments are made to reflect the higher cost of living and prevent bracket creep. Without these adjustments, people with incomes that merely keep pace with inflation could be pushed into higher tax brackets and end up paying more individual income tax.

The IRS adjusts certain tax credits and deductions to account for inflation. Some of the provisions that are adjusted include tax brackets, the size of the standard deduction, the Earned Income Tax Credit, and the exclusions for estate and gift taxes. For instance, the standard deduction for married couples filing jointly for tax year 2023 rose to $27,700, up $1,800 from the prior year.

Additionally, the income thresholds for each federal tax bracket are increased to reflect inflation. For example, the income tax brackets for tax year 2025 have been adjusted, with the top tax rate remaining at 37% for individual single taxpayers with incomes greater than $626,350 ($751,600 for married couples filing jointly).

The IRS also adjusts the maximum credit amounts, phase-out ranges, and investment income limits annually to account for inflation. For instance, the maximum Earned Income Tax Credit amount for qualifying taxpayers with three or more qualifying children increased from $7,430 in 2024 to $7,830 in 2025.

Furthermore, limits on contributions to retirement accounts, such as 401(k) plans, are also indexed for inflation. For example, the 401(k) contribution limit for 2024 was $23,000, and it increased to $23,500 for 2025.

Duress and Undue Influence: Invalidating Contracts

You may want to see also

Explore related products

![]()

How do tax credits work?

In the United States, there are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These brackets are permanent as of the 2025 tax year. The income tax rates and brackets run from 10% to 37%. As your income increases, the tax rate on the next layer of income is higher. However, when your income jumps to a higher tax bracket, you only pay the higher rate on the portion of your income that falls within that bracket. For example, if you had $50,000 of taxable income in 2024 as a single filer, you would pay 10% on the first $11,600, 12% on the income between $11,601 and $47,150, and 22% on the rest. Your effective tax rate in this scenario would be about 12%. It's important to note that states may have different tax systems, with some states like Colorado having a flat tax rate and others like Wyoming having no income tax.

Now, regarding tax credits, they are a tool to reduce your tax liability. A tax credit is a dollar-for-dollar reduction in your income tax, directly lowering your tax burden. For instance, if your total tax is $1,000 and you are eligible for a $1,000 tax credit, your net liability becomes zero. Some tax credits, such as the Earned Income Credit, are refundable, meaning you receive the full amount even if it exceeds your tax bill. In the previous example, if your total tax is $400 and you claim a $1,000 credit, you will receive a $600 refund. Tax credits are available at both the federal and state levels, but not all states offer them as not all states require residents to file income taxes.

There are various types of tax credits catering to different situations. For instance, the federal government offers a credit for purchasing solar panels to encourage environmentally conscious behaviour. Additionally, there is the federal adoption tax credit to assist families in the adoption process. The Child Tax Credit is another example of a nonrefundable credit that lowers the taxpayer's tax liability. To qualify, the child must be a US citizen under 17 with a Social Security number and be claimed as a dependent on the taxpayer's return. Taxpayers with qualified dependents may be eligible for specific credits and deductions.

To determine eligibility for tax credits, individuals can conduct online research, visit the IRS website, or consult tax experts or software. It is beneficial to stay informed about the latest tax laws and credits to make effective financial decisions. The IRS estimates that four out of five workers are eligible for the Earned Income Tax Credit (EITC), yet many who qualify do not claim it, missing out on potential financial benefits. Therefore, it is essential to carefully review current tax credits and claim all applicable credits and deductions when filing tax returns.

Governing Law vs. Applicable Law: What's the Difference?

You may want to see also

Explore related products

![]()

How does your filing status affect your tax bracket?

Tax brackets divide portions of your income into different windows based on filing status. This means that your filing status can have a significant impact on your tax bracket and, ultimately, your tax liability.

There are five filing statuses: single, married filing jointly, married filing separately, head of household, and qualifying widow(er) or surviving spouse. Your filing status is tied to your marital status, but it can also depend on factors such as the number of children and occupation. For example, a single filer with no children or dependents would fall under the single category, while a single individual supporting dependents may be considered the head of the household.

The tax rates for each bracket differ depending on the filing status. Single taxpayers generally pay tax at higher rates than married taxpayers who file joint returns. This is because the income levels that determine the tax brackets for married people filing jointly are less than double the income levels for single people, a phenomenon known as "the marriage penalty." As a result, married couples may find themselves in higher tax brackets faster than single people. On the other hand, filing as the head of a household can provide tax advantages, with a higher standard deduction and more favourable tax brackets than filing single.

Additionally, deductions can impact your filing status and tax bracket. Deductions can reduce your taxable income and potentially move you to a lower bracket, resulting in a lower tax rate. Tax credits can also help reduce your tax bill, but they do not affect your tax bracket.

It's important to select the correct filing status as it can significantly affect your tax liability. Taxpayers who are eligible to claim more than one filing status usually choose the one with the lowest tax rates. However, it's crucial to file your status honestly, as providing false information can be considered fraudulent and may result in penalties.

The First Child Protection Law: A Historical Overview

You may want to see also

Explore related products

![]()

How do you calculate your marginal tax rate?

Marginal tax rates are assigned to tax brackets, or taxable income ranges. Your marginal tax rate is the highest rate that will be applied to your income. It refers to the tax rate applied to the last dollar of your taxable income.

To calculate your marginal tax rate, you can use the federal income tax brackets, which are based on your filing status and taxable income for the tax year. The tax rate that applies to the tax bracket for your total taxable income is your marginal tax rate. The tax brackets are adjusted annually to account for inflation.

For example, if you are a single filer with $50,000 of taxable income in 2024, you pay 10% on the first $11,600 and 12% on the chunk of income between $11,601 and $47,150. Then, you pay 22% on the rest because some of your $50,000 of taxable income falls into the 22% tax bracket. Your total bill was roughly $6,053, or about 12% of your taxable income, even though 22% is your marginal tax rate.

Your marginal tax rate does not give you a clear picture of the overall rate at which you are taxed. To calculate your effective tax rate, or the average amount you pay on each dollar, divide the amount you pay in taxes by your gross annual income.

Constitutional Carry Law: Oklahoma's Gun Rights

You may want to see also

Frequently asked questions

Tax brackets are layers of income taxed at different rates. The higher your income, the higher the tax bracket and rate.

There are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Your tax bracket is determined by your filing status (single, married filing jointly, etc.) and your taxable income.

No, you only pay the highest rate for the portion of your income that falls into that tax bracket. The rest of your income is taxed at lower rates.

The Internal Revenue Service (IRS) adjusts tax brackets annually to account for inflation. These adjustments ensure that income tax brackets, deductions, and other inputs remain in line with the changing cost of living.