Catch-up contributions were introduced in 2001 as part of the Economic Growth and Tax Relief Reconciliation Act (EGTRRA). They allow people aged 50 or older to make additional contributions to their retirement savings accounts, such as 401(k)s, IRAs, and other employer-sponsored plans. These contributions are intended to help individuals who may not have saved enough for retirement to increase their savings and maximize their investment opportunities. The Pension Protection Act of 2006 made catch-up contributions permanent, and the IRS reviews and adjusts contribution limits annually to account for inflation. More recently, the SECURE Act 2.0 of 2022 introduced changes to the rules surrounding catch-up contributions, including the requirement for higher-income earners to make catch-up contributions to designated Roth accounts after 2025.

| Characteristics | Values |

|---|---|

| Law that created catch-up contributions | Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) |

| Year of introduction | 2001 |

| Type of contribution | Retirement savings contribution |

| Eligible individuals | People aged 50 or older |

| Contribution limit for IRA in 2024 and 2025 | $8,000 ($7,000 plus an additional $1,000 catch-up contribution) |

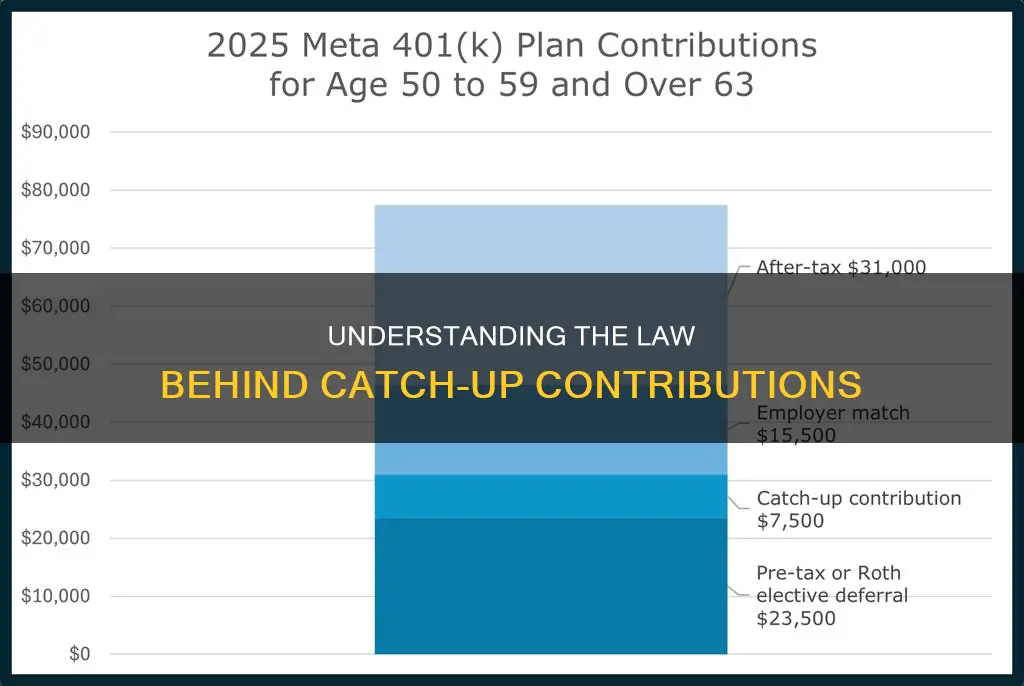

| Contribution limit for 401(k) in 2024 and 2025 | $31,000 ($23,500 plus an additional $7,500 catch-up contribution) |

| Contribution limit for 401(k) in 2025 for ages 60-63 | $34,750 ($23,500 plus an additional $11,250 catch-up contribution) |

| Contribution limit for SIMPLE IRA/SIMPLE 401(k) in 2023 | $4,500 ($1,500 plus an additional $3,000 catch-up contribution) |

| Contribution deadline | Federal tax filing date of the following year (usually April deadline) |

Explore related products

What You'll Learn

- The Economic Growth and Tax Relief Reconciliation Act of 2001 created catch-up contributions

- The Pension Protection Act of 2006 made catch-up contributions permanent

- The SECURE Act 2.0 of 2022 changed catch-up contribution rules

- Catch-up contributions are for retirement savings accounts

- Catch-up contributions are for people aged 50 or older

![]()

The Economic Growth and Tax Relief Reconciliation Act of 2001 created catch-up contributions

The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) created catch-up contributions. This provision allows workers aged 50 and above to save more for retirement by contributing additional funds to their 401(k) and IRA accounts beyond the standard limits. These catch-up contributions are elective deferrals, where employees can deposit money from their pay into their retirement accounts, exceeding legal, plan-imposed, or ADP limits. The IRS sets annual catch-up contribution amounts and limits, which vary depending on the retirement plan. For example, in 2024 and 2025, the IRA contribution limit for individuals aged 50 and older is $8,000, including a $1,000 catch-up contribution.

While the EGTRRA initially scheduled catch-up contributions to expire in 2010, the Pension Protection Act of 2006 made these provisions permanent. This permanence ensures that workers can continue to benefit from the ability to increase their retirement savings through catch-up contributions. Additionally, the SECURE Act 2.0, which came into effect in 2022, further enhanced catch-up contributions by indexing future amounts to inflation. This adjustment ensures that individuals can continue to maximize their retirement savings despite inflationary pressures.

It is important to note that catch-up contributions are not limited to a single retirement account. Individuals with multiple accounts can make catch-up contributions to more than one plan, such as IRAs, employer-sponsored plans, SIMPLE IRAs, and health savings accounts (HSAs). This flexibility allows individuals to maximize their savings across various retirement vehicles.

The eligibility for catch-up contributions is primarily based on age, with individuals aged 50 and above being eligible to take advantage of these provisions. However, it's worth mentioning that employees with at least 15 years of service may also be eligible for additional catch-up contributions, regardless of age. This eligibility criterion allows long-serving employees to boost their retirement savings even further.

In conclusion, the Economic Growth and Tax Relief Reconciliation Act of 2001 played a pivotal role in establishing catch-up contributions, providing older workers with the opportunity to enhance their retirement savings. This provision has since been solidified and augmented by subsequent legislation, ensuring that individuals have the tools necessary to adequately prepare for their golden years.

OSH Act: The Origin of Workers' Compensation Law

You may want to see also

Explore related products

![]()

The Pension Protection Act of 2006 made catch-up contributions permanent

Catch-up contributions were introduced in 2001 as part of the Economic Growth and Tax Relief Reconciliation Act (EGTRRA). Under this Act, catch-up contributions were originally scheduled to expire at the end of 2010. However, the Pension Protection Act of 2006 made catch-up contributions permanent, allowing older workers to continue making additional contributions to their retirement savings beyond the standard limits.

Catch-up contributions are designed for individuals aged 50 and above to help them boost their retirement savings, especially if they haven't saved enough earlier in their careers. These contributions can be made to various retirement plans, including popular employer-sponsored 401(k) plans, traditional IRAs, Roth IRAs, SIMPLE IRAs, and Simplified Employee Pensions (SEPs).

The annual contribution limits for catch-up contributions vary across different retirement plans and are adjusted periodically to account for inflation. For example, in 2024 and 2025, the catch-up contribution limit for a 401(k) plan is $7,500, excluding SIMPLE 401(k)s, which is in addition to the standard contribution limit of $23,500. For IRAs, the catch-up contribution limit is $1,000 on top of the annual contribution limit of $7,000 for the same period.

It's important to note that the rules and limits for catch-up contributions may change over time. Recent legislation, such as the SECURE Act 2.0, has introduced adjustments to the contribution limits for certain age groups and income levels. Therefore, individuals considering catch-up contributions should stay informed about the latest regulations and consult with financial advisors to make informed decisions regarding their retirement savings.

Procedural Law: Who Makes the Rules?

You may want to see also

Explore related products

![]()

The SECURE Act 2.0 of 2022 changed catch-up contribution rules

The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) originally created catch-up contribution provisions. However, the SECURE Act 2.0 of 2022 changed the rules surrounding catch-up contributions.

Catch-up contributions allow individuals aged 50 or older to make additional elective deferral contributions to their employer-sponsored retirement savings plans above the standard IRS limits. These contributions are not mandatory and plans are not required to offer them, but if they do, they must generally make them available to all participants eligible for catch-up contributions.

The SECURE Act 2.0 of 2022 introduced a change for higher-income participants making catch-up contributions in a 401(k) or similar retirement plan. Beginning in 2026, those earning more than $145,000 in the prior year will need to designate their catch-up contributions as after-tax Roth contributions. This means that while contributions will be made after taxes, qualified withdrawals in retirement will be tax-free.

Additionally, the SECURE Act 2.0 of 2022 increased catch-up contribution limits for certain retirement plan participants. In 2025, the catch-up contribution limit increased to $7,500 for individuals aged 50 or older, on top of the annual contribution limit of $23,500. For individuals aged 60 to 63, the catch-up contribution limit increased further to $11,250.

The SECURE Act 2.0 of 2022 also made changes to the age at which retirees must take required minimum distributions (RMDs) from IRA and 401(k) accounts. The age increased to 73 in 2023 and will increase further to 75 beginning in 2033.

The Evolution of EU Law: Who Are the Key Players?

You may want to see also

Explore related products

![]()

Catch-up contributions are for retirement savings accounts

Catch-up contributions are a type of retirement savings contribution that allows people aged 50 or older to make additional contributions to their retirement accounts, including 401(k)s, IRAs, and other employer-sponsored plans. These contributions are designed to help individuals who may not have saved enough for retirement when they were younger or those who want to maximise their savings.

The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) created the catch-up contribution provision. Originally, these contributions were scheduled to expire at the end of 2010. However, the Pension Protection Act of 2006 made catch-up contributions permanent. The IRS sets the catch-up contribution amounts annually, and the limits vary based on the type of retirement account and the individual's age. For example, the catch-up contribution limit for a 401(k) plan in 2024 and 2025 is $7,500, while the limit for an IRA is $1,000. These limits are in addition to the standard annual contribution limits for each type of account.

It's important to note that catch-up contributions are not mandatory, and individuals should consider their finances, goals, and tax situation before deciding to make them. Additionally, not all retirement plans may offer catch-up contributions, so it's essential to review the specific provisions and rules of your retirement plan.

The SECURE Act 2.0, passed in 2022, made further changes to catch-up contributions. Beginning in 2026, individuals earning more than $145,000 in the previous year will need to make catch-up contributions to a Roth 401(k) account with after-tax dollars. This change will impact how high-income earners make their catch-up contributions.

By taking advantage of catch-up contributions, eligible individuals can boost their retirement savings and potentially benefit from tax advantages. These contributions provide flexibility and help individuals achieve their financial goals for retirement.

The Law of Gravity: A Historical Perspective

You may want to see also

Explore related products

![]()

Catch-up contributions are for people aged 50 or older

Catch-up contributions were introduced in 2001 as part of the Economic Growth and Tax Relief Reconciliation Act (EGTRRA). They allow people who are aged 50 or older to save more for their retirement. This is particularly beneficial for those who have not saved enough for retirement and want to maximise their savings.

The primary eligibility requirement for catch-up contributions is the individual's age. Plan participants aged 50 or over at the end of the calendar year are often eligible to make annual catch-up contributions. It is important to note that participants cannot contribute more than their compensation over elective deferral contributions that are not catch-up contributions.

Catch-up contributions can be made to various retirement plans, including employer-sponsored 401(k) plans, traditional IRAs, Roth IRAs, SIMPLE IRAs, and Simplified Employee Pension (SEP) plans. These contributions are considered elective deferrals, where employees make deposits into their retirement accounts that exceed legal or plan-imposed limits.

The IRS sets catch-up contribution amounts and limits annually, taking into account factors such as inflation. For example, for 2024 and 2025, the IRA contribution limit for investors aged 50 and older is $8,000, including a $1,000 catch-up contribution. Additionally, the SECURE Act 2.0, which came into effect in 2022, allows individuals aged 60-63 to make higher catch-up contributions of up to $11,250 for 2025.

It is worth noting that catch-up contribution rules are subject to change. Beginning in 2026, individuals earning more than $145,000 in the previous year will need to make catch-up contributions to a Roth 401(k) account, paying taxes on those contributions but benefiting from tax-free withdrawals in retirement.

The Law of Conservation of Mass: Its Historical Origin

You may want to see also

Frequently asked questions

Catch-up contributions were created by the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA). The Pension Protection Act of 2006 made these contributions permanent.

Individuals aged 50 or over at the end of the calendar year can make annual catch-up contributions. Some sources also mention that individuals aged 60 to 63 can make higher catch-up contributions.

The contribution limits vary by year and the type of retirement account. For 2024 and 2025, the IRA contribution limit is $8,000, including a $1,000 catch-up contribution. For 2025, the catch-up contribution limit for most 401(k) plans is $7,500, excluding SIMPLE 401(k)s.