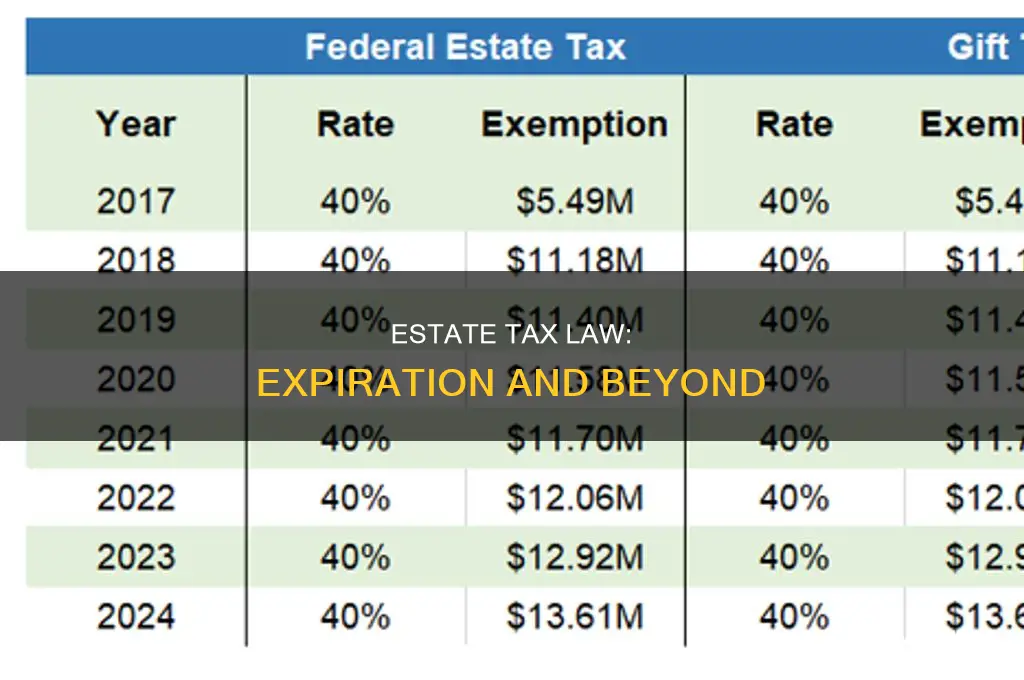

The estate tax law in the United States is a federal tax on the transfer of a deceased person's estate. The estate tax is part of the federal unified gift and estate tax, which also includes the gift tax that applies to transfers of property during a person's life. In 2025, the estate tax exemption increased to $13.99 million for individuals and $27.98 million for married couples. The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, made this increase permanent and raised the exemption for 2026 to $15 million for single filers and $30 million for married couples filing jointly. This legislation also indexed the higher basic exclusion amount for inflation in years after 2026, using 2025 as the new base year for adjustments. It is important to note that some states may have their own estate tax laws and exemption amounts, which can vary and may not always be as high as the federal exemption.

| Characteristics | Values |

|---|---|

| Current estate tax law expiration date | End of 2025 |

| Basic exclusion amount (BEA) in 2025 | $13,990,000 |

| BEA in 2026 | $15 million |

| BEA in 2018 | $11.18 million |

| BEA in 2019 | $11.4 million |

| BEA in 2020 | $11.58 million |

| Legislation that made BEA permanent | One Big Beautiful Bill Act (OBBBA) |

Explore related products

$12.49 $21.99

What You'll Learn

![]()

The One Big Beautiful Bill Act (OBBBA)

OBBBA 2025 makes permanent aspects of the 2017 Tax Cuts and Jobs Act (TCJA) that were set to expire at the end of 2025. The TCJA had temporarily raised the estate exemption amount to a higher base threshold. OBBBA makes that extension permanent and also increases the exemption amounts for 2026.

The only federal and gift tax change in OBBBA 2025 is a slight but permanent increase in the maximum lifetime exclusion amount (lifetime exemption) that any U.S. citizen or resident can use to shelter gifted assets or assets passing at death from the federal gift tax or federal estate tax. The lifetime exclusion amount represents the value of the property that an individual could give away or leave after death without having any gift tax or estate tax imposed on the transfer of that property.

For unmarried individuals with a net worth of $7-15 million and married couples with a combined net worth of $14-30 million, the likelihood of owing a net federal estate tax after death has decreased to zero or nearly zero, unless they have already made significant taxable gifts and used up most of their lifetime exclusion amounts. OBBBA's increase in the basic exclusion amount for 2026 and future years has also made irrelevant some regulations that the Treasury (IRS) finalized in 2019 to deal with the issue of how the federal estate tax should be calculated if an individual made large taxable gifts during 2018-2025.

Income Taxes: Understanding the Law

You may want to see also

Explore related products

![]()

Estate tax exemption amounts

The estate tax exemption amounts have undergone changes over the years. From 2006 to 2008, the applicable exclusion amount was $2,000,000, meaning there was no federal estate tax due if the taxable estate plus adjusted taxable gifts during a lifetime totalled $2,000,000 or less. In 2009, the applicable exclusion amount increased to $3,500,000, and the estate tax was repealed for estates of decedents dying in 2010. However, the legislation was not permanent, and the estate tax was scheduled to return in subsequent years.

The Tax Cuts and Jobs Act (TCJA) of 2017 brought significant changes to the estate tax exemption amounts. The act doubled the basic exclusion amount (BEA) for tax years 2018 through 2025. The BEA is adjusted annually for inflation, resulting in the following exemption amounts: $11.18 million for 2018, $11.4 million for 2019, and $11.58 million for 2020. These increased exemption limits provided individuals with greater flexibility in estate planning and gift-giving.

However, it is important to note that the TCJA's increased exemption amounts are temporary. In 2026, the BEA is scheduled to revert to its pre-2018 level of $5 million, adjusted for inflation. This means that the estate tax exemption amount will be lower in 2026 unless Congress extends the higher exemption limits. The impending change has prompted individuals to reevaluate their estate plans and consider strategies to maximise the increased exemption before the law sunsets.

The latest updates from the Internal Revenue Service (IRS) indicate that for 2024, the federal estate tax exemption amount is $13.61 million per individual. This allows individuals to transfer up to this amount of assets during their lifetime or at death without incurring federal gift or estate taxes. Additionally, the IRS has announced that for 2025, the estate and gift tax exemption will increase further to $13.99 million per individual. These changes highlight the dynamic nature of estate tax exemption amounts and the importance of staying informed about the latest adjustments.

Contract Law Basics: Understanding Standard Contracts

You may want to see also

Explore related products

![]()

Federal estate tax

In the United States, the estate tax is a federal tax on the transfer of a deceased person's estate. The federal estate tax does not apply unless an estate reaches a certain exemption amount. The federal estate tax is part of the unified federal gift and estate tax system. The other part of the system, the gift tax, applies to transfers of property during a person's life.

The exemption amount for people who pass away in 2025 is $13.99 million (up from $13.6 million in 2024). For married couples, the exemption is $27.98 million (up from $27.22 million in 2024). Estates valued over the exemption amount are taxed at a rate of 40%. For example, estates exceeding $14,990,000 for individuals or $28,980,000 for married couples are taxed at 40%.

The Tax Cuts and Jobs Act (TCJA) of 2017 temporarily raised the estate exemption amount. The One Big Beautiful Bill (OBBB), enacted on July 4, 2025, made that extension permanent. The OBBB also increased the exemption amounts for 2026: single filers will receive an estate exemption of $15 million, and married couples filing jointly will receive an exemption of $30 million. These exemption amounts will be indexed for inflation in years after 2026.

The estate tax is periodically the subject of political debate. Some opponents have called it the "death tax," while some supporters have called it the "Paris Hilton tax."

UK Constitutional Law: Who's Teaching?

You may want to see also

Explore related products

![]()

Gift tax

In the United States, the federal government levies a gift tax on transfers of money, property, and other assets during a person's life. This is separate from estate taxes, which are levied on assets transferred to heirs upon a person's death.

The gift tax and estate tax provisions apply a unified rate schedule to a person's cumulative taxable gifts and taxable estate to arrive at a net tentative tax. The applicable exclusion amount, known as the Basic Exclusion Amount (BEA), is adjusted annually for inflation. For 2018, the BEA was $11.18 million, increasing to $11.4 million in 2019, and $11.58 million in 2020.

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly increased the gift and estate tax exemption. However, this higher exemption is temporary and only applies to tax years up to 2025. After 2025, the exemption is scheduled to revert to the pre-2018 level of $5 million, adjusted for inflation. This means that individuals who take advantage of the increased gift tax exclusion amount between 2018 and 2025 will not face adverse consequences after the exclusion amount drops in 2026.

It is important to note that there are strategies to reduce gift and estate taxes, such as gifting assets during one's lifetime to reduce the taxable estate. Additionally, certain gifts, such as cash and assets with little appreciation, are generally more tax-efficient than highly appreciated assets.

While the current gift tax laws provide a framework for taxation, it is essential to stay informed about potential changes. Congress has the power to modify these laws, and annual reviews of gift and estate strategies are recommended to align with any legislative updates.

Religious Influence on Colonial Laws Explored

You may want to see also

Explore related products

![]()

Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act (TCJA) is a United States federal law that amended the Internal Revenue Code of 1986. It was enacted in December 2017 and is officially known as the Trump Tax Cuts. The TCJA overhauled the federal tax code by reforming individual and business taxes. It significantly lowered marginal tax rates and the cost of capital, reducing federal revenue by an estimated $1.47 trillion over 10 years before accounting for economic growth.

The TCJA lowered most individual income tax rates, including the top marginal rate from 39.6% to 37%. It increased the standard deduction to $12,400 for single filers and $24,800 for married filers (tax year 2020), compared to $6,500 (single) and $9,550 (married) under prior law. The act also eliminated the personal exemption and limited certain itemized deductions, such as the state and local tax (SALT) deduction, mortgage interest deduction (MID), and charitable contribution deduction.

The TCJA reduced the corporate income tax (CIT) rate from 35% to 21%, ten percentage points higher than the OECD average. It allowed full and immediate expensing of short-lived capital investments for five years and increased the section 179 expensing cap from $500,000 to $1 million. The act eliminated or reduced various business taxes and expenditures, including the deductibility of net interest and net operating loss carrybacks and carryforwards.

The TCJA also included changes to deductions, depreciation, expensing, tax credits, and other items affecting businesses. It introduced Opportunity Zones to spur economic development and job creation in distressed communities. According to the Tax Policy Center, the TCJA lowered individual income taxes for about 65% of US households, raised them for about 6%, and left them unchanged for the rest.

Promulgating Constitutional Law: A Guide

You may want to see also

Frequently asked questions

The current estate tax law is the One Big Beautiful Bill Act (OBBBA), which was enacted on July 4, 2025.

The OBBBA made permanent the increase in the maximum lifetime exclusion amount (lifetime exemption) that any U.S. citizen or resident can use to shelter gifted assets or assets passing at death from the federal gift tax or federal estate tax.

For 2025, the lifetime exclusion amount is $13,990,000 for individuals and $27,980,000 for married couples.

For 2026 and beyond, the lifetime exclusion amount will be $15 million for individuals and $30 million for married couples.