Japan's taxation system is primarily based on a national income tax, with rates varying according to one's area of residence. The country also levies consumption and excise taxes at the national level, an enterprise tax and a vehicle tax at the prefectural level, and a property tax at the municipal level. While taxes are administered by the National Tax Agency, the country's tax laws are influenced by various factors, including international tax rules, tax treaties, and the political landscape. The Liberal Democratic Party (LDP), for instance, has played a significant role in shaping Japan's tax policies, with notable contributions from politicians like Masayoshi Ōhira, Noboru Takeshita, and Ryutaro Hashimoto.

Explore related products

What You'll Learn

![]()

Tax laws are administered by the National Tax Agency

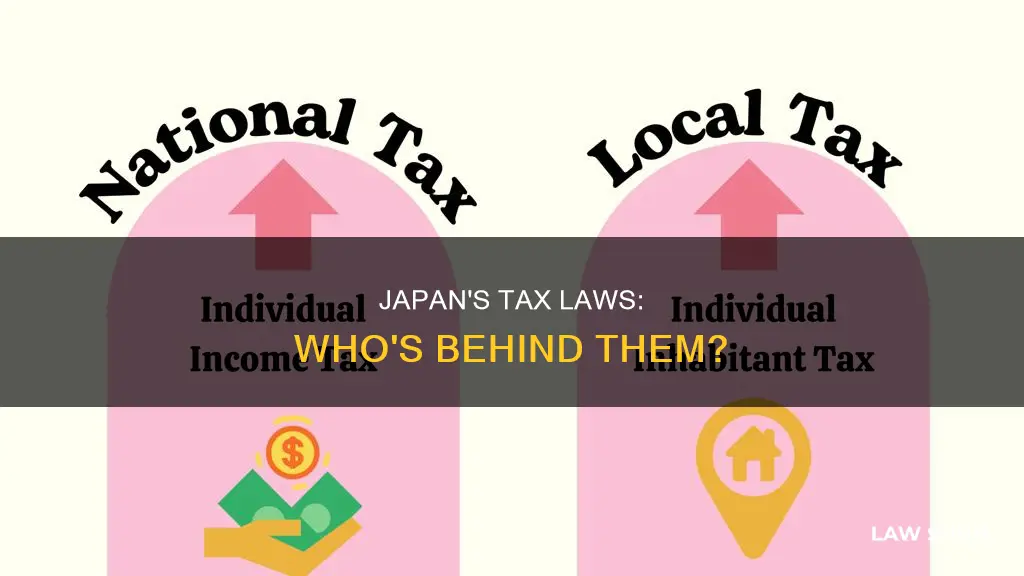

Taxation in Japan is based primarily on national income tax, consumption taxes, and excise taxes at the national level. There are also enterprise taxes and vehicle taxes at the prefectural level, as well as property taxes at the municipal level. These tax laws are administered by the National Tax Agency.

The National Tax Agency oversees the collection of taxes from individuals and corporations. This includes income tax, which is levied on the income of residents and non-residents, as well as enterprise taxes for those engaged in business activities. The Agency also administers consumption taxes, such as the national consumption tax and the local consumption tax. These consumption taxes are applied to the purchase of goods and services, with varying rates depending on the type of product, such as a reduced rate for food and drinks.

In addition to the above, the National Tax Agency also manages excise taxes, which include taxes on liquor, tobacco, and gasoline. These excise taxes are included in the prices that consumers pay for these items. Furthermore, the Agency deals with vehicle-related taxes, such as the prefectural automobile tax, municipal light vehicle tax, and the national motor vehicle tonnage tax.

The National Tax Agency also plays a role in the taxation of spouses. In Japan, there is a phenomenon known as the "Wall of 1.03 million yen and 1.30 million yen," where spouses can take a marital deduction if their income is below these thresholds. However, if the main earner's income exceeds 10 million yen, the couple is not eligible for this deduction.

Another area of focus for the National Tax Agency is inheritance tax. In Japan, inheritance tax is levied on individual heirs rather than on the estate of the deceased. This tax must be filed within 10 months of the death, and it is calculated based on the fair market value of the inherited assets, minus any exemptions or funeral expenses.

Overall, the National Tax Agency plays a crucial role in administering and enforcing Japan's tax laws, ensuring that taxes are collected fairly and efficiently from individuals and businesses across the country.

Creating Public Health Laws: Which Branch of Government?

You may want to see also

Explore related products

![]()

The Liberal Democratic Party introduced a consumption tax in 1989

Taxation in Japan is based primarily on a national income tax, which varies depending on one's area of residence. There are also consumption taxes and excise taxes at the national level, an enterprise tax and vehicle tax at the prefectural level, and a property tax at the municipal level. Taxes are administered by the National Tax Agency.

The Liberal Democratic Party (LDP) government first attempted to introduce a consumption tax in 1979 under Masayoshi Ōhira, but this was met with opposition within the party and was abandoned after the party suffered losses in the 1979 election. Ten years later, in 1989, the LDP successfully negotiated with politicians, bureaucrats, businesses, and labor unions to introduce a 3% consumption tax. This was achieved under Noboru Takeshita.

The consumption tax was initially unpopular and was blamed for causing a recession in Japan, though others attributed this to the 1997 Asian financial crisis. In April 1997, the consumption tax was raised to 5% under Ryutaro Hashimoto, comprising a 4% national consumption tax and a 1% local consumption tax.

Since 2008, Japanese taxpayers have had the option to redirect a portion of their income tax to one of the regions instead of the central government. This has led to regions competing for these taxes by offering "gifts" of products and services, allowing taxpayers to obtain goods at lower prices. Inheritance tax in Japan is levied on individual heirs and must be filed within 10 months of the death of the deceased.

Mosaic Law: When Was It Created?

You may want to see also

Explore related products

![]()

Japan's tax system has a progressive tax rate

Taxation in Japan is primarily based on a national income tax that varies according to one's area of residence. Japan's income tax system has a progressive tax rate, meaning that a higher rate of tax is applied as income increases. The tax rate increases in stages, and the method of payment differs between those who work for a company and those who are self-employed. For those working for a company, income tax is deducted from salaries in advance and paid collectively by the company. For the self-employed, income and tax for the year must be calculated, and a tax return filed with the tax office.

The residence status of an individual is an important factor in determining tax liability in Japan. All individuals, regardless of nationality, are classified as either residents or non-residents. Residents are taxed on their worldwide income, regardless of the location of the source of income. Non-residents, on the other hand, are taxed only on their Japan-sourced income. The definition of a resident for tax purposes includes those with a permanent home in Japan, as well as those with a temporary home in the country for a year or more. Non-permanent residents refer to non-Japanese citizens who have resided in Japan for five years or less within a ten-year period.

In addition to income tax, Japan also has consumption taxes, excise taxes, enterprise taxes, vehicle taxes, and property taxes. Consumption taxes are levied on the purchase of goods and services, while excise taxes are specific taxes on certain products or activities. Enterprise taxes are paid by individuals engaged in certain businesses specified in local tax laws, and taxable income for this purpose is calculated similarly to income tax. Vehicle taxes are levied at the prefectural level, while property taxes are administered at the municipal level.

Inheritance tax in Japan is levied on individual heirs, rather than on the estate as a whole, and must be filed within 10 months of the death of the deceased. This tax is also progressive, with a rate of up to 55% based on the fair market value of the inherited assets, minus any applicable deductions and exemptions.

The Ohio Cruelty Law: Who Was Behind It?

You may want to see also

Explore related products

![]()

Taxpayers can redirect income tax to one of the regions

Taxation in Japan is based primarily on national income tax, which is calculated based on one's area of residence. Since 2008, Japanese taxpayers have had the option to pay 2,000 yen to redirect a portion of their income tax to one of the regions, instead of to the central government. This is not limited to their "home town". Regions compete to win these taxes by offering "gifts" of various products and services, and many taxpayers use this opportunity to buy products at a lower price. For example, a donation of 2,000 yen can produce a "gift" of 60 kg of rice, equivalent to an adult's annual consumption.

In Japan, individuals are classified as either residents or non-residents. Individual income tax is levied on the individual's income for the calendar year. A resident is defined as someone who has a domicile in Japan or has resided in the country for one year or more. Residents are taxed on their worldwide income. Non-permanent residents are those who have lived in Japan for less than five years and do not intend to stay permanently. They are taxed on their income from Japan and any foreign-source income that is paid or remitted to Japan. Non-residents are those who have lived in Japan for less than a year and do not have their primary base of living in the country. They are taxed only on income from sources in Japan.

The tax liability for residents is determined by multiplying the excess taxable income for each bracket by the corresponding percentage. Japan also has a self-assessment system, where individuals calculate their own income and tax for the year and file a tax return with the tax office, known as "kakutei shinkoku". Additionally, there is a withholding tax system, where taxes are subtracted from salaries and wages by employers. Most employees in Japan do not need to file a tax return due to this system.

Natural Law: Who Was the Founding Father?

You may want to see also

Explore related products

![]()

Japan's Corporate Income Tax Law is part of the Triangular Legal System

Japan's taxation system is primarily based on a national income tax that varies depending on one's area of residence. There are also consumption and excise taxes at the national level, an enterprise tax and vehicle tax at the prefectural level, and a property tax at the municipal level.

The Securities and Exchange Law requires each "issuer" of designated securities to file annual and semi-annual reports with the Prime Minister and copies with the Ministry of Finance.

The Corporate Income Tax Law outlines the taxation requirements for corporations in Japan. For example, a company with its head office in Japan is considered a domestic corporation, regardless of the place of central management or the nationality of its shareholders. Resident companies are taxed on their worldwide income, while non-resident companies are taxed only on Japanese-source income at standard corporate rates.

Japanese tax law also provides for special tax credits and deductions on certain research and development costs. For instance, if a corporation incurs research and development expenses related to qualified IP and earns income from transferring or licensing this IP to third parties, the income earned is taxed at a favourable rate through special deductions.

South Africa's Lawmakers: Who Crafts the Rules?

You may want to see also

Frequently asked questions

The Liberal Democratic Party (LDP) has historically been responsible for creating tax laws in Japan. For example, the LDP government of Masayoshi Ōhira attempted to introduce a consumption tax in 1979, and Noboru Takeshita successfully introduced a 3% consumption tax in 1989.

Japan levies a variety of taxes, including income tax, consumption tax, excise tax, enterprise tax, vehicle tax, and property tax.

Japan's income tax is based on an individual's area of residence and income level. All individuals, regardless of nationality, are classified as either residents or non-residents. Residents are taxed on their worldwide income, while non-residents are taxed only on income earned in Japan.

Yes, Japan offers several tax breaks and deductions. For example, the "Innovation Box" regime provides tax breaks on income earned from certain intellectual property developed in Japan. Additionally, there are special tax credits and deductions for research and development costs. Japan also has a spouse deduction, which allows couples to take a marital deduction if one spouse's income is below a certain threshold.