The Tax Cuts and Jobs Act (TCJA) has had a significant impact on the federal budget and deficit. The act, which came into effect in 2018, included substantial tax cuts that added $1 to $2 trillion to the federal debt. The impact of the TCJA on the deficit has been a subject of debate, with some arguing that it will increase the deficit in the long run, while others believe it will boost economic activity and reduce the deficit. The Penn Wharton Budget Model estimates that the Trump administration's tax proposals, including the TCJA, could increase primary deficits by up to $5.1 trillion over a decade. The “Big Beautiful Bill” House GOP Tax Plan, which includes extensions of the TCJA, is also estimated to reduce federal revenues by $4 trillion between 2025 and 2034. These tax cuts primarily benefit high-income households, while lower-income households may experience declines in income and welfare. To address budget deficits, local governments, such as in Forsyth County, North Carolina, have proposed raising property taxes, which has sparked controversy among residents.

| Characteristics | Values |

|---|---|

| Tax Cuts and Jobs Act (TCJA) | Cut taxes substantially from 2018 through 2025 |

| TCJA Deficits | Adding $1 to $2 trillion to the federal debt |

| CBO's 2018 Update | Deficit increase of about $1.4 trillion |

| TCJA's Impact on Economic Activity | Boost by an average of about 0.7% over the budget window |

| Reduction in Deficit Impact | About $385 billion |

| Increase in Revenues | $451 billion |

| Increase in Spending | $66 billion |

| One Big Beautiful Bill Act (OBBBA) | Significant updates across the tax code, impacting how Americans file taxes |

| "No Tax on Overtime" Rule | Effective 2025-2028, allows certain workers to claim a dollar-for-dollar deduction for overtime pay |

| "No Tax on Tips" Law | Effective 2025-2028, allows a dollar-for-dollar deduction for a designated amount of tips |

| State and Local Tax (SALT) Deduction | Provides a federal deduction for income and property taxes paid locally and at the state level |

| Trump Administration Tax Proposals | Increase 10-year primary deficits by $5.1 trillion before economic growth effects and by $4.9 trillion after |

| House Budget Reconciliation Instructions | Allow a net deficit increase of $4.5 trillion over the 2025-2034 budget window |

| "Big Beautiful Bill" House GOP Tax Plan | Estimated to reduce federal tax revenue by $4 trillion from 2025 through 2034 |

| Deficit Impact of the Bill | Increase in the budget deficit by $1.7 trillion from 2025 through 2034 |

| Public Law 119-21 | Increase in the cumulative effect on the deficit to $4.1 trillion |

| Corporate Income Tax Rate Cuts | Part of the 2017 law, will remain indefinitely |

Explore related products

What You'll Learn

![]()

Spending cuts and tax increases

The Tax Cuts and Jobs Act (TCJA) has had a significant impact on the federal budget and national debt. The act, which came into effect in 2018, introduced substantial tax cuts and changes to the tax code, including the removal of personal and dependent exemptions and changes to the standard deduction. While the act was intended to be revenue-neutral, with any losses from tax cuts offset by new taxes or the removal of tax breaks, it has instead resulted in a substantial increase in the deficit. Official estimates predict that the TCJA will add $1 to $2 trillion to the federal debt, with this figure rising if temporary tax cuts are extended beyond their original expiry date of 2025. The Congressional Budget Office (CBO) initially estimated that the act would increase the deficit by $1.1 trillion over a decade, but this figure was revised upwards to $1.4 trillion in 2018.

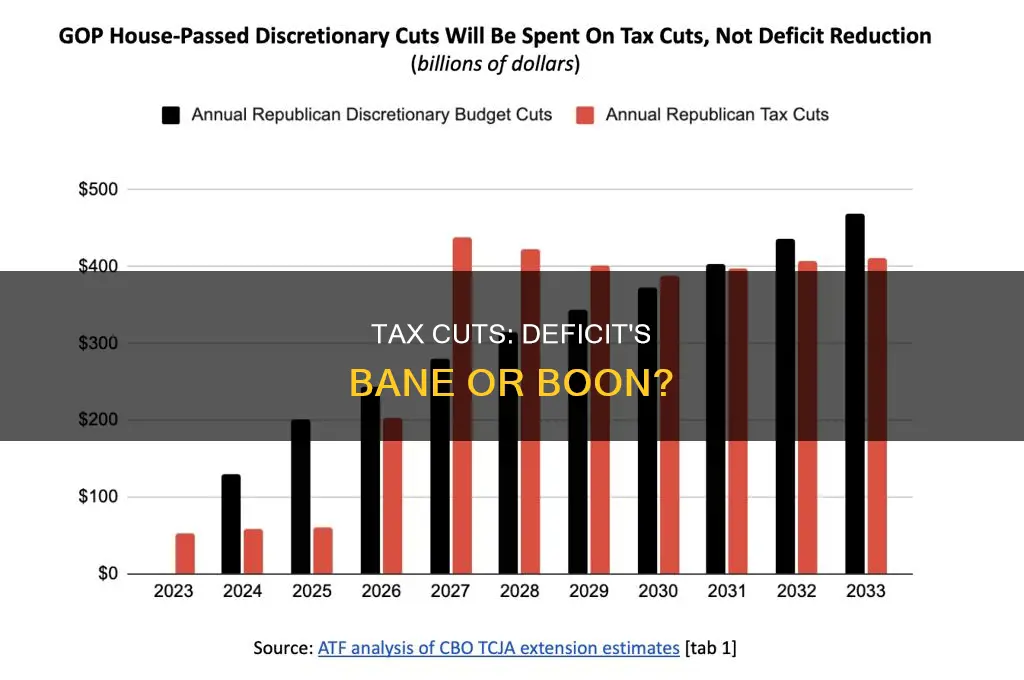

The impact of the TCJA on the federal budget and national debt has led to discussions of potential spending cuts and tax increases to reduce the deficit. The FY2025 House Budget reconciliation, for example, includes instructions for $1.7 trillion in net spending cuts and $4.5 trillion in net tax cuts, allowing for a $2.8 trillion increase in primary deficits over the 10-year budget window from FY2025 to FY2034. However, if House committees meet their targets for $2 trillion in mandatory spending reductions and $300 billion in spending increases, the total outlays would be reduced by $1.7 trillion over the budget window relative to current law.

The Trump administration's tax proposals have also been estimated to increase primary deficits by $5.1 trillion over the next decade, before accounting for economic growth effects, and by $4.9 trillion after growth effects. These proposals include significant spending increases in areas such as defense, border security, and law enforcement, as well as tax cuts for high-income households. To offset these increases, the administration has proposed spending cuts in areas such as Medicaid, nutrition assistance, and student loans.

While both spending cuts and tax increases can be used to reduce deficits, there is ongoing debate about which approach is more effective and less harmful to economic growth. Some argue that cutting spending is less detrimental than raising taxes, as it can signal the possibility of future tax cuts and associated benefits to economic growth. Additionally, deficit reduction policies based on spending cuts typically have a minimal effect on output, making them a more reliable method for reducing the debt-to-GDP ratio. However, it is important to note that the impact of austerity policies can vary between developed and developing economies, and short-term and long-term considerations may differ.

The Evolution of Employment Law: A Historical Perspective

You may want to see also

Explore related products

$36.95 $36.95

![]()

Deficit financing

The influence of government deficits on a national economy can be significant. While some economists have abandoned the balanced budget concept, others argue that deficit spending is always bad policy and that a government should always run a balanced budget.

Some theories, such as Chartalism, argue that a structural deficit is necessary for monetary expansion in an expanding economy. According to Chartalists, if the economy grows, the money supply should also increase through government deficit spending. They believe that private sector savings are equal to government sector deficits.

In contrast, deficit spending can also result from government inefficiency, reflecting issues like tax evasion or wasteful spending.

National government deficits may be intentional or unintentional and can result from policy decisions. For example, the Tax Cuts and Jobs Act (TCJA) in the United States is estimated to increase deficits by $1 to $2 trillion, adding to the federal debt.

Overall, deficit financing is a complex issue with potential benefits and drawbacks. While it can be used as a tool to stimulate the economy, it also contributes to increasing government debt and interest obligations.

Contract Law Basics: Understanding the Fundamentals

You may want to see also

Explore related products

![]()

Temporary tax cuts

The OBBB, signed into law in 2025, includes temporary changes such as the “No Tax on Overtime” rule, which allows certain workers to claim a dollar-for-dollar deduction for a designated amount of overtime pay. It also introduces the “No Tax on Tips” law, which allows a similar deduction for a designated amount of tips earned by workers. Additionally, the bill provides for tax years 2025 through 2028, expiring after President Trump's term ends.

The Tax Cuts and Jobs Act (TCJA) of 2017 is another example of temporary tax cuts. While the TCJA permanently lowered the corporate income tax rate, it also included several temporary policies. For instance, R&D expensing must now be spread out over multiple years instead of being fully deducted in the first year. Net interest deductions have been restricted since 2022, and "bonus" depreciation for businesses will completely expire at the end of 2026.

The impact of temporary tax cuts on deficits can be complex. The TCJA, for example, substantially cut taxes from 2018 through 2025, adding $1 to $2 trillion to the federal debt. However, the Joint Committee on Taxation and the Congressional Budget Office (CBO) estimated that the act would reduce deficits starting in 2027. If the temporary tax cuts in the TCJA are extended or made permanent, deficits will be higher. Similarly, the Trump administration's tax proposals in the FY2025 House Budget reconciliation are estimated to increase 10-year primary deficits by $5.1 trillion before accounting for economic growth effects and by $4.9 trillion after growth effects.

Creating Public Health Laws: Which Branch of Government?

You may want to see also

Explore related products

![]()

Tax cuts for the rich

The Tax Cuts and Jobs Act (TCJA) has resulted in substantial tax cuts from 2018 through 2025, with temporary tax cuts potentially extended beyond this period. These cuts are expected to add $1 to $2 trillion to the federal debt, according to official estimates. The Joint Committee on Taxation and the Congressional Budget Office (CBO) have published estimates of the budget impact, with the CBO projecting a $1.9 trillion increase in the conventional budget over the same period.

The TCJA has been criticised for disproportionately benefiting higher-income households and corporations, while providing minimal relief to working families and lower-income households. For example, under the House Republican reconciliation bill, families earning less than $50,000 would receive less than $300 in tax cuts, while those earning $1 million or more could receive around $90,000 in tax breaks. This pattern continues with policies like larger deductions for wealthy business owners and estate tax exemptions for wealthy heirs.

The extension of the TCJA beyond its original timeframe is expected to increase the fiscal gap, making it harder to stabilise the ratio of public debt to gross domestic product (GDP). This could result in economic pain for working families, especially if spending cuts are made to programmes like SNAP or Medicaid.

Some Americans support tax cuts for the rich due to fairness considerations and the prospect of upward mobility. However, the impact of these tax cuts on the federal debt and the potential harm to working families are important considerations in the ongoing debate surrounding tax policy.

Contract Law Court: Where to Seek Legal Recourse

You may want to see also

Explore related products

![]()

Tax cuts for corporations

The Tax Cuts and Jobs Act (TCJA) has had a significant impact on the federal budget and deficit. The act, which was enacted in 2017, included substantial tax cuts for corporations and individuals. The corporate income tax rate was permanently lowered from 35% to 21%, while several other policies were made temporary. The TCJA also included provisions such as the bigger Standard Deduction, the repeal of personal exemptions, and changes to itemized deductions. According to official estimates, the resulting deficits from the TCJA are expected to add $1 to $2 trillion to the federal debt.

The impact of the TCJA on the deficit has been a subject of analysis by organizations like the Joint Committee on Taxation and the Congressional Budget Office (CBO). The CBO initially estimated that the TCJA would increase the deficit by slightly less than $1.1 trillion over a decade. However, in a subsequent update, the CBO revised this estimate to about $1.4 trillion. The Joint Committee on Taxation (JCT) found that the TCJA would boost economic activity and reduce the deficit impact by about $385 billion.

The TCJA also included temporary provisions that are set to expire at the end of 2025, such as most cuts to individual income taxes and business expensing for new investments. If lawmakers decide to extend these expiring provisions, it will further increase the deficit. According to estimates, extending the expiring provisions would add about $480 billion to deficits through 2027 and a growing amount thereafter.

In 2025, the One Big Beautiful Bill Act (OBBBA) was signed into law, which included permanence for major individual and corporate provisions of the TCJA, along with additional temporary tax cuts for individuals and businesses. The OBBBA is estimated to reduce federal tax revenue by $5 trillion between 2025 and 2034 on a conventional basis. The act also introduced significant updates across the tax code, including the “No Tax on Overtime” rule, the “No Tax on Tips” law, and changes to the State and Local Tax (SALT) Deduction.

The Trump administration's tax proposals and spending plans have also been a subject of analysis. The FY2025 House Budget reconciliation includes proposals for $1.7 trillion in net spending cuts and $4.5 trillion in net tax cuts, allowing for a $2.8 trillion increase in primary deficits over the 10-year budget window from FY2025 to FY2034. However, incorporating economic growth effects, the primary deficits are estimated to increase by $4.9 trillion over this period. The Trump administration's tax proposals are expected to benefit high-income households the most, while lower-income households may gain less or even lose.

Taxes and Law: What's the Connection?

You may want to see also

Frequently asked questions

The Tax Cuts and Jobs Act (TCJA) was a law enacted in 2017 that cut taxes substantially from 2018 through 2025.

The TCJA is expected to increase the federal budget deficit by $1.1 trillion over a decade, according to the Congressional Budget Office (CBO). The Joint Committee on Taxation (JCT) estimates a smaller increase of $385 billion.

The TCJA includes substantial tax cuts for individuals and businesses, with most individual income tax cuts expiring at the end of 2025. The act also introduces temporary changes, such as limiting taxes on tips and overtime pay.

The JCT estimates that the TCJA will boost economic activity by an average of 0.7% over the budget window, reducing the deficit impact. However, the CBO's 2018 update projects a higher deficit increase of $1.4 trillion.

Continuing low tax rates for the wealthy and corporations are likely to hurt working families and slow economic growth over time. Deficit financing to maintain these low tax rates can drag on economic growth, and spending cuts in social insurance and income support can further negatively impact Americans' incomes and welfare.