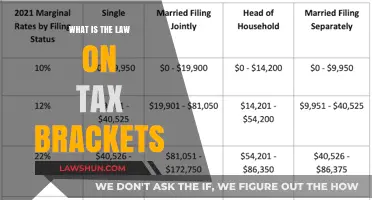

Churches are unique entities under US law, and their tax status is distinct from that of other religious organisations. Churches are automatically granted tax-exempt status without needing to apply for a Letter of Determination from the IRS. This exemption is based on the Constitution and specific IRS codes. While churches are not required to file annual tax returns or pay federal income tax, they may still be liable for tax on unrelated business income. They must also comply with various reporting obligations, including annual information returns to employees and self-employed workers, and adhere to public policy standards such as non-discrimination policies.

Characteristics and Values of Church Tax Information

| Characteristics | Values |

|---|---|

| Tax-Exempt Status | Churches are automatically granted tax-exempt status under IRC 508(c)(1)(a) without needing to apply for a Letter of Determination. |

| Employer Identification Number (EIN) | Churches with an EIN and recognized as such are tax-exempt. |

| Annual Information Returns | Churches are generally exempt from filing annual information returns (Form 990) but must provide information returns to employees and self-employed workers (W-2 and 1099 forms). |

| Unrelated Business Income Tax | Churches may be liable for tax on unrelated business income, i.e., income from a regularly carried-on trade or business not related to their exempt purposes. |

| Annual Certification of Racial Nondiscrimination | Churches must comply with public policy standards and annually certify racial nondiscrimination (Form 5578). |

| Political Campaign Activity | Section 501(c)(3) tax-exempt organizations, including churches, are restricted from intervening in political campaigns. |

| Audits and Tax Inquiries | Special rules limit the IRS's authority to audit churches, and there are specific guidelines for tax inquiries and examinations. |

Explore related products

What You'll Learn

![]()

Churches are automatically granted tax-exempt status

Churches are unique entities under US law and are automatically granted tax-exempt status without the need to apply for a Letter of Determination from the IRS. This exemption is based on the Constitution and specific IRS codes, ensuring churches are recognised as federally tax-exempt entities.

While churches are not required to file an application with the IRS for tax exemption, they may still have various reporting obligations under federal law. For example, churches must issue annual "information returns" to employees and self-employed workers (W-2 and 1090-MISC forms). They are also required to issue a 1099-INT form to those who were paid $600 or more in interest income during the year. Additionally, churches must file the annual certification of racial nondiscrimination (Form 5578), which is one of the most commonly disregarded federal reporting obligations.

Although churches are exempt from filing Form 990, which is the annual information return for tax-exempt organisations, they may be liable for tax on their unrelated business income. This means income from a regularly carried-on trade or business that is not substantially related to their exempt purpose.

To maintain their automatic tax-exempt status, churches must be formally organised, operate exclusively for exempt purposes, and adhere to public policy standards, including prohibitions on racial discrimination and advocating for the overthrow of the government. While not mandatory, some churches may opt to obtain a Letter of Determination to enhance their credibility with donors and stakeholders.

Bailment Basics: Contract Law Explained

You may want to see also

Explore related products

![]()

Churches are exempt from filing Form 990

Churches are categorised as tax-exempt organisations under IRC Section 501(c)(3) by the IRS. While tax-exempt organisations are generally required to file an annual information return (Form 990), churches are exempt from this requirement. This exemption also applies to some church-affiliated organisations.

Churches are not required to file Form 990 annually to report their financial information, activities, and other details. However, they may choose to file Form 990 voluntarily to strengthen transparency and integrity among the public and contributors. Making the return available for public inspection increases trust in the church's financial activities. Additionally, a Form 990 filed by a church can serve as documented evidence of its exempt activities and program service accomplishments.

While churches are exempt from filing Form 990, they are still subject to taxes on any business income that is not substantially related to their exempt purposes. For example, churches with unrelated business gross taxable income of $1,000 or more in a tax year are required to file Form 990-T, Exempt Organisations Business Income Tax Return. Furthermore, churches must still comply with other filing requirements, such as Forms W-2, 1099, 940, and 941.

To obtain tax-exempt status, churches must first apply for an EIN by filing Form SS-4. Once they receive the EIN, they can file Form 1023 with the IRS. The IRS will then provide a determination letter recognising the church as a tax-exempt organisation. It is important to note that churches must meet certain requirements and guidelines established by the IRS to maintain their tax-exempt status.

Why Tax Returns are Vital for Presidential Candidates

You may want to see also

Explore related products

$7.75 $17.75

![]()

Churches must issue annual information returns to employees

Churches are unique entities under US law, and their tax obligations differ from those of other organisations. While churches are automatically granted tax-exempt status, they may still have certain reporting obligations under federal law.

One such obligation is the requirement to issue annual information returns to employees. Specifically, churches must provide these returns to all employees who were paid wages, as well as to any self-employed individuals who received at least $600 in annual compensation from the church. These information returns are known as W-2 and 1099-MISC forms, respectively. Additionally, if a church pays $600 or more in interest income to an individual in a given year, it must issue a 1099-INT form to that person.

It is important to note that churches are exempt from filing annual information returns with the IRS, unlike most other tax-exempt organisations. This exemption is outlined in Section 6033 of the Internal Revenue Code, which specifically mentions "churches, their integrated auxiliaries, and conventions and associations of churches" as being exempt from this requirement. This means that the government has very limited insight into the financial activities of churches, unless an audit is conducted, which is rare.

Despite this exemption, churches are still subject to other reporting requirements, such as the quarterly employer's tax return (Form 941) and the unrelated business income tax return (Form 990-T). Furthermore, churches must adhere to public policy standards, including prohibitions on racial discrimination and advocating for the overthrow of the government. While not mandatory, some churches may opt to obtain a Letter of Determination to enhance their credibility with donors and stakeholders.

Exploring Roman Law: Categories and Their Influence

You may want to see also

Explore related products

![]()

Churches must adhere to public policy standards

Churches are unique entities under US law, and understanding their tax status under the IRS code and the Constitution is crucial. Churches are automatically granted tax-exempt status without needing to apply for a Letter of Determination from the IRS. This exemption is a direct result of the Constitution and specific IRS codes, ensuring churches are recognised as federally tax-exempt entities.

However, to maintain this status, churches must adhere to public policy standards. These standards include prohibitions on racial discrimination and advocating for the overthrow of the government, as established by key court decisions like the 1983 Bob Jones University case. While not mandatory, some churches may opt to obtain a Letter of Determination to enhance their credibility and assure donors and stakeholders of their tax-exempt status.

Churches are generally exempt from filing annual information returns, such as Form 990, which is typically required for tax-exempt organisations. However, they still have various reporting obligations under federal law. These include annual information returns to employees and self-employed workers (W-2 and 1099 forms), the quarterly employer's tax return (Form 941), and the annual certification of racial nondiscrimination (Form 5578).

It is important to note that churches may be liable for tax on their unrelated business income, which refers to income from a regularly carried-on trade or business that is not related to their exempt purposes. To ensure compliance and make informed decisions, churches are encouraged to consult with tax experts or legal advisors.

The Evolution of UK Copyright Law

You may want to see also

Explore related products

![]()

Churches may need a Letter of Determination

Churches are unique entities under US law, and while they automatically qualify for tax-exempt status, they may opt to secure a Letter of Determination from the IRS for further validation. This letter is not a requirement, but it can aid in fundraising, grant applications, or supporting affiliated ministries. It provides additional credibility and assurance to donors and stakeholders about the church's tax-exempt status.

The Letter of Determination can be especially useful in the following scenarios:

- Tax-deductible donations: During an audit, if a taxpayer's donations to your church are challenged, the donor may need to prove that the church is a qualifying charity. Without a determination letter, the tax deduction may be disallowed.

- Property tax exemption: A church may find it challenging to obtain a property tax exemption for its land and facilities without a determination letter.

- Donor expectations: Most donors expect churches to have a determination letter as it signals that the church has been officially recognized as a charitable organization by the IRS, enhancing its trustworthiness.

To obtain a Letter of Determination, churches can consult with tax experts or legal advisors to ensure compliance and make informed decisions about their tax status. This decision can depend on the specific needs and activities of the church. It is worth noting that churches are generally excepted from filing annual information returns, but they may choose to do so if they wish.

Who Makes the Laws in the US?

You may want to see also

Frequently asked questions

Yes, churches are automatically granted tax-exempt status without the need to apply for a Letter of Determination. Churches are unique entities under U.S. law and are recognised as federally tax-exempt entities.

Churches are exempt from filing annual information returns, also known as Form 990. However, they must issue annual "information returns" to employees and self-employed workers (W-2 and 1099 forms). They are also required to submit the quarterly employer's tax return (Form 941), the unrelated business income tax return (Form 990-T), and the annual certification of racial nondiscrimination (Form 5578).

To maintain its tax-exempt status, a church must be formally organised (e.g. as a corporation or trust), operate exclusively for exempt purposes (religious, charitable, etc.), and adhere to public policy standards, including prohibitions on racial discrimination and advocating for the overthrow of the government.