Carried interest is a share of the profits of an investment paid to the investment manager, usually in private equity and hedge funds. The concept has become a political flashpoint in the US, with critics arguing that it is a loophole that allows fund managers to secure a reduced tax rate. The debate centres around whether carried interest should be taxed as capital gains or ordinary income. While the former is taxed at a lower rate (20%), the latter is subject to a higher tax rate of 37%. The preferential tax rate for carried interest has been a topic of discussion in US politics since at least 2007, with various bills and proposals introduced to change its tax treatment.

| Characteristics | Values |

|---|---|

| What is carried interest | A share of the profits of an investment paid to the investment manager |

| Origin | 16th century when European ships were crossing to Asia and the Americas |

| Carried interest rate | 20% |

| Carried interest fees charged by private equity firms | Only when the investment returns exceed a "performance hurdle" |

| Carried interest tax rate | Same as long-term capital gains |

| Ordinary income tax rate | 37% |

| Long-term capital gains tax rate | 20% |

| Ordinary marginal tax rate for single filers in 2021 | 22% if they earn over $40,525 |

| Ordinary marginal tax rate for married couples filing jointly in 2021 | 22% if they earn over $81,051 |

| Tax law change | 2017 Tax Cuts and Jobs Act |

| Minimum holding period for long-term capital gains | 3 years |

Explore related products

What You'll Learn

![]()

The carried interest loophole

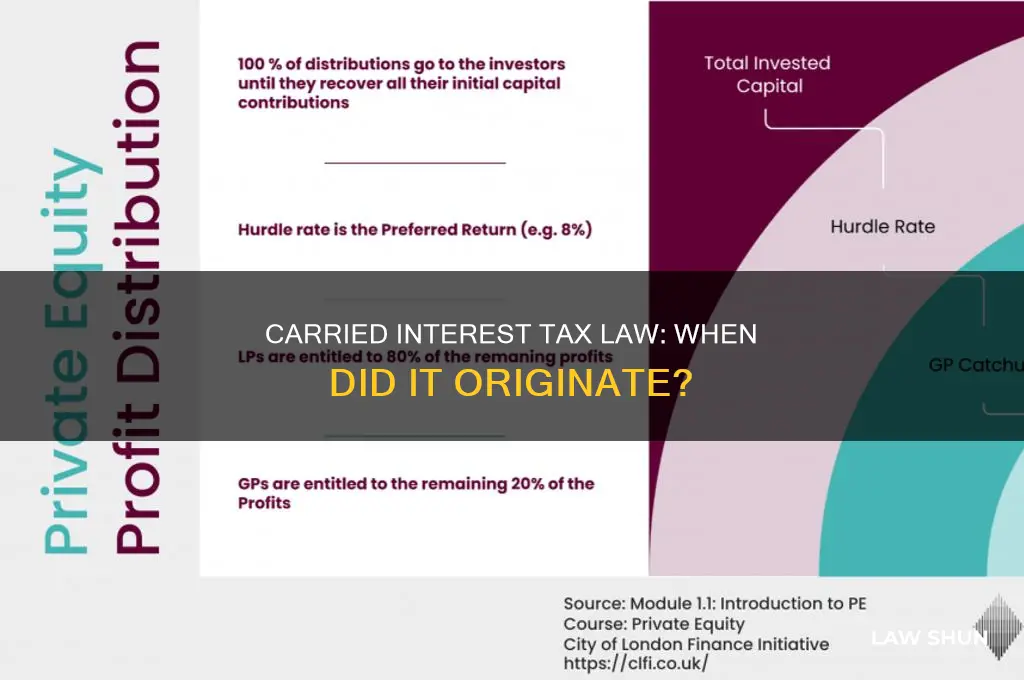

Carried interest is a type of compensation paid to general partners of investment funds. It is a performance fee, rewarding the manager for enhancing performance. The manager's carried interest allocation varies depending on the type of investment fund and the demand for the fund from investors. In private equity, the standard carried interest allocation has been 20% for funds making buyout and venture investments, but there can be some variability. For example, a general partner might receive an annual management fee of 2% of a fund's assets, as well as carried interest equal to 20% of a fund's profits.

The controversy surrounding the carried interest loophole arises from how it is taxed. While a management fee is taxed as ordinary income at a top marginal rate of 37%, carried interest is often treated as long-term capital gains, with a top rate of 20%. This preferential tax treatment allows fund managers to pay lower taxes than they would if their earnings were taxed as ordinary income. The distinction between ordinary income and capital gains dates back to the oil and gas industry of the early 20th century.

Critics of the carried interest loophole argue that it exacerbates income and wealth inequality, as it allows some of the richest Americans to pay lower taxes than middle-class taxpayers. Closing the loophole is estimated to raise between $1.4 billion and $18 billion annually in additional tax revenue. However, proponents of the current tax treatment argue that fund managers provide valuable investment strategies, expertise, and oversight, justifying the reduced tax rate.

Attempts have been made to close the carried interest loophole, including through the 2017 Tax Cuts and Jobs Act, which extended the minimum holding period for an investment to qualify for the long-term capital gains rate from one year to three years. However, this change was deemed ineffective as most private equity investments are held for longer periods, and clever accounting techniques can dodge the requirement.

Contract Law: Why It's Essential for Society

You may want to see also

Explore related products

$29.99 $24.99

![]()

How carried interest is taxed

The concept of carried interest originated in the 16th century when European ships sailed to Asia and the Americas. The ship captain would take a 20% share of the profit from the carried goods to pay for transport and cover the risks of sailing.

Today, carried interest is a share of the profits of an investment paid to the investment manager, usually in alternative investments such as private equity and hedge funds. It is a performance fee that rewards the manager for enhancing performance.

In the United States, carried interest is taxed at the same rate as long-term capital gains, which is a lower rate than ordinary income. This preferential tax rate is a controversial political issue, with critics arguing that it is a loophole that allows private equity managers to pay lower taxes than regular employees. The top tax rate for capital gains is 20%, compared to 37% for ordinary income. This distinction allows fund managers to significantly reduce their tax bill.

The 2017 Tax Cuts and Jobs Act attempted to address this loophole by requiring investments to be held for a minimum of three years to qualify for the tax break. However, this provision was easily circumvented as most private equity investments are held for longer periods.

There is ongoing debate about whether carried interest should be taxed as ordinary income to create a fairer and more efficient tax system.

Understanding Contract Law: What is a Puff?

You may want to see also

Explore related products

![]()

Origins of carried interest

The origins of carried interest can be traced back to the 16th century when European ships sailed to Asia and the Americas. The captain of the ship would take a 20% share of the profit from the carried goods to pay for the transport and the risk of sailing over oceans. The name is unrelated to interest rates or interest payments on loans or bank accounts.

Today, the term "carried interest" refers to the compensation collected by investment executives in private equity funds. It is a performance fee that rewards the manager for enhancing performance. The manager's carried interest allocation varies depending on the type of investment fund and investor demand. In private equity, the standard carried interest allocation has historically been 20% for funds making buyout and venture investments, but there is some variability.

Carried interest is often only paid if the fund achieves a minimum return known as the ""hurdle rate". It typically serves as the primary source of compensation for the general partner, amounting to 20% of a fund's returns. Private equity firms usually charge carried interest fees only if the investment returns exceed a "performance hurdle" of 6 to 8%.

The controversy surrounding carried interest stems from how it is taxed. It is taxed as capital gains, resulting in a lower tax rate than if it were taxed as ordinary income. This allows partners receiving carried interest to pay less in taxes while potentially earning a higher salary than regular employees. Critics argue that this creates inequality in taxation and that carried interest should be taxed as wage and salary income, which has a top rate of 37%.

Tax Law: Impact on Jobs Returning to the USA

You may want to see also

Explore related products

![]()

Critics of carried interest

Critics of the carried interest system object to the ability of fund managers to treat most of their return as capital gains, including amounts above and beyond the amount directly related to the capital contributed by the manager. Critics characterise this as managers taking advantage of tax loopholes to receive what is effectively a salary without paying the 37% marginal ordinary income tax rate. This preferential tax treatment of carried interest reduces federal revenues, putting pressure on the federal budget. According to McKinsey & Company, private equity funds managed $8.2 trillion in 2023, and the Congressional Budget Office estimated that treating carried interest as ordinary income would raise $12 billion over ten years.

The controversy surrounding carried interest has been ongoing since the mid-2000s and has increased as the growth in assets under management by private equity and hedge funds has driven up manager compensation. As of September 2016, the carried interest tax regime's total tax benefit for private equity partners is estimated to be from $2 billion to $16 billion per year. This has resulted in income and wealth inequality, with private equity managers paying lower tax rates than middle-class taxpayers.

Critics argue that carried interest is compensation for a service and should, therefore, be taxed at ordinary income rates. They contend that removing the tax break would increase the tax system's transparency and fairness by treating carried interest as ordinary income. Additionally, taxes on carried interest are not due until a realisation event occurs, typically the sale of an investment, which allows for further tax deferral.

The carried interest loophole has been criticised as a "home run for private equity investors" and has been a controversial political issue, with some arguing that it allows private equity managers to secure a reduced tax rate. In 2017, the Tax Cuts and Jobs Act extended the number of years an asset must be held before it is considered a long-term capital gain from one to three years. However, this change was easy to circumvent as most private equity investments are held for 5 to 7 years, and clever accounting techniques can dodge the 3-year requirement.

Contract Law: Understanding the Basics of Agreements

You may want to see also

Explore related products

$32.45

![]()

Attempts to close the loophole

The carried interest loophole has been a controversial issue in the United States, with critics arguing that it allows private equity managers to pay lower tax rates than middle-class taxpayers. This loophole has been referred to as "Wall Street's favorite tax break" and has been a target of attempts to close it. Here are some details on these attempts:

Political Campaigns and Promises:

As a presidential candidate, Donald Trump promised to close the carried interest loophole, criticizing investment fund managers for not paying their fair share of taxes. However, when it came to changing the tax law, his administration and the Republican Congress sided with private equity lobbyists and preserved the loophole in the 2017 Tax Cuts and Jobs Act. This act extended the holding period for investments to qualify for the tax break to three years, but this provision was easily circumvented by the industry.

Legislative Efforts:

There have been legislative efforts to close the carried interest loophole at the state level. Liberal political activists, lawmakers, and "patriotic millionaires" have advocated for ending the loophole in New York and other states. Similar legislative efforts were planned in California, Connecticut, Illinois, Massachusetts, New Jersey, and Pennsylvania. These attempts aimed to treat carried interest as ordinary income, arguing that it is a fee for services and should be taxed accordingly.

Democratic Party Platform:

Closing the carried interest loophole was part of the Democratic Party platform in 2020. It was included in the recommendations by the Unity Task Force of the Biden and Sanders presidential campaigns. However, the specifics of their proposed reforms are not publicly available.

Public Support:

A significant majority of voters across parties support legislation that would close the carried interest loophole. Treating carried interest income as ordinary compensation income could raise between $1.4 billion and $18 billion annually in additional tax revenue.

Proposed Reforms:

Some commonly proposed reforms by the Congressional Research Service include applying ordinary income tax rates to only a portion of carried interest or treating carried interest entirely as ordinary income. This would increase the tax burden on private equity executives and reduce the inequality caused by the current loophole.

Understanding Set-Offs: A Powerful Contractual Tool

You may want to see also

Frequently asked questions

The carried interest rate is the share of profits from an investment paid to the investment manager.

The carried interest rate is taxed as capital gains, which is a lower tax rate than ordinary income.

The carried interest rate is controversial because it allows investment managers to pay a lower tax rate than they would if their income were taxed as ordinary income. Critics argue that this creates inequality in taxation, with high-earning investment managers paying less in taxes than regular employees.

The concept of carried interest can be traced back to the 16th century when ship captains would take a share of the profits from carried goods to pay for transport and cover the risk of sailing.

The 2017 Tax Cuts and Jobs Act slightly curtailed the tax preference for carried interest by increasing the minimum holding period for investments to qualify for long-term capital gains treatment from one to three years. However, critics argue that this change was easy to circumvent and did not effectively close the carried interest loophole.